This article first appeared in the July-August 2017 edition of Funds Europe.

It’s feared that Brexit could destroy tens of thousands of jobs in the City of London, mainly in investment banking. Here, Mark Latham looks at the impact on the UK’s £7 trillion asset management industry.

A few weeks after the 2016 Brexit vote to end the UK’s 43-year membership of the European Union, it looked like the British government would have little alternative but to set aside the unexpected result.

It faced a situation where the Japanese car maker Nissan had threatened it would shift production from Sunderland in north-east England to factories in continental Europe as a direct result of the vote.

The Conservative government hastily convened talks with Nissan executives and came to a secret agreement, the details of which have never been published, to keep production in the UK.

Had the deal not been made, many believe that the sight of some 7,000 blue-collar workers being laid off within weeks of the Brexit vote would have shifted public opinion to such an extent that a second referendum would have become unavoidable.

A year on from the referendum, and just weeks after formal negotiations on the UK’s departure finally got underway, business leaders believe hundreds of thousands of UK jobs could be lost as a result of Brexit.

Manufacturing (particularly the automobile industry) and agriculture are expected to be big losers, but the sector that is likely to be hardest hit is the country’s enormously successful financial services industry.

The City of London, shorthand for the UK’s entire financial sector, has for years been the country’s largest exporter, running a £19.1 billion (€21.6 billion) surplus in financial services with the EU in 2015.

The question now confronting the UK is whether the country is prepared to risk damaging its most successful export industry under the mantra of ‘taking back control’ of regulation, law-making and immigration.

On that question, a report published this month by trade body the TheCityUK – which is lobbying for a bespoke deal for the UK’s financial sector – found that, while a flexible immigration policy could help to ease some lost ground from Brexit, it won’t bring as many benefits as staying in the EU.

The report also warned that London could lose its status as Europe’s top financial centre and that continental Europe could become the preferred destination for banks, insurers and asset managers as they relocate business there to retain access to the EU single market.

While firms may start shifting a small number of jobs to Europe, this could accelerate when property leases expire, firms carry out business reviews or when the cost of capital becomes uneconomical.

While firms may start shifting a small number of jobs to Europe, this could accelerate when property leases expire, firms carry out business reviews or when the cost of capital becomes uneconomical.

Meanwhile, a research paper from consultancy firm Oliver Wyman estimated that the hardest form of Brexit could put 35,000 job losses in the financial sector at risk along with £20 billion of annual income and £5 billion of tax revenues.

In such a scenario, a further 40,000 jobs and £18 billion of revenue, and £5 billion of tax revenue, could also be indirectly lost from the ‘ecosystem’ of lawyers, consultants and accountants who service the financial services industry.

At the other end of the spectrum, it is estimated that a softer Brexit that put the UK outside the European Economic Area (EEA), but delivered access to the EU’s single market as well as passporting and equivalence for financial services, would put up to 4,000 jobs at risk and lead to a £2 billion decline in income.

Other studies estimate similarly high levels of job losses: one by PwC estimates 70,000 jobs and a loss of between £14 billion and £20 billion in revenues, while a more recent study from EY estimates that 83,000 jobs are at risk.

The majority of the potential jobs losses are likely to be from investment banking operations. Crucially, the estimates do not include a further 100,000 jobs that would be at risk if London loses its dominance of the €1 trillion-a-day euro clearing market as a result of Brexit.

Small but significant

The number of potential job losses in the asset management industry is smaller but still significant.

According to the Investment Association (IA), the UK is Europe’s largest asset management centre (larger than that of Germany, France and Italy combined) with firms managing £5.7 trillion from the UK, of which some £1.2 trillion is for EU investors and a further £1 trillion for clients in the rest of the world.

Of the UK’s £200 billion of revenues from financial services, around a quarter is international and wholesale business related to EU countries other than the UK. Of that total, asset management accounts for around £24 billion, of which £6 billion is business related to the EU (ex-UK) that would be directly impacted by Brexit.

A research paper from the London School of Economics published this year warns that UK-based asset managers may need to set up subsidiaries across Europe to continue to manage investment funds domiciled there in an efficient way.

Both the Oliver Wyman and PwC studies claim that between a third to a half of the UK’s £6 billion EU-related asset management revenues, worth between £2 billion and £3 billion a year, could look for a new home post-Brexit.

So far a steady trickle of asset management firms have said they plan to retain the ability to do business with the rest of the EU post-Brexit (see panel) by moving jobs abroad.

Jorge Morley-Smith, director of international affairs and Brexit at the IA, said that while the issue of passporting is not an “existential threat” to the UK’s funds industry, there are areas that are “vulnerable”.

When Brexit negotiations eventually turn to trade issues and the extent to which the UK will continue to have access to the single market, Morley-Smith says there will be “a number of potential banana skins en route that we need to avoid”.

The “number-one priority”, he says, is the issue of delegation of portfolio management and the degree to which management of Ucits funds can be delegated to non-EU countries.

“Post-Brexit, the UK would be a third country that would rely on third-country provisions,” he says. “Some of the mood music from Europe suggests that regulation related to third countries could be tightened: that is the threat.

“My assumption is that the UK asset management industry will continue to flourish but politics could get in the way so that things could yet go very wrong.”

Gina Miller, the co-founder of London-based wealth manager SCM Direct, believes that fund firms in the UK “have not yet got a grasp of the seriousness of the threat to the industry over the issue of passporting”.

Miller, who shot to fame last year as the figurehead of a legal challenge that forced the UK government to consult parliament over the triggering of Brexit, says that the industry needs to lobby the government more vociferously than it has so far.

“I am surprised that the industry has not been more vocal about pushing for access to the EU single market. There needs to be a single industry voice to speak out about the dangers confronting the industry,” she told Funds Europe.

“There is now a real threat to the profitability of the industry, the recruitment and retention of staff and the ability of firms to sell products across borders.

“I think that because of the febrile atmosphere around politics in the UK now and worries about who will be in power in the future, voices in the industry that should be speaking out are not.”

The reluctance of firms to speak out about threats to the industry was echoed by another UK fund manager who, speaking on condition of anonymity, said that firms are afraid they will be shut out of future consultation if they are deemed to be not sufficiently positive about Brexit by the government.

Of the various post-Brexit options open to the UK, Miller believes that staying within the EEA would be the least disruptive model for the funds industry.

“If that is not politically possible, then a long period of transitional arrangements would be needed to reduce disruption to the industry,” she says. “The two years of transition that is being talked about is really not going to be long enough.”

Miller also warns that equivalence is a “very poor alternative to passporting” and would require UK firms to apply to the European Securities and Markets Authority (Esma) to be regarded as operating from a third country with an equivalent regulatory regime.

That process in itself would be time-consuming and Esma does not have the resources to process hundreds of registration applications quickly.

Miller pours cold water on the idea that leaving the EU would lead to a bonfire of red tape.

“There were people who thought that leaving the EU would lead to less regulation, but for the funds industry this would have to stay in place if the UK wants to continue to do business abroad,” she says.

She believes that the remaining 27 EU member states may not necessarily be the main jobs beneficiaries of Brexit. Some US financial firms could, given the uncertainty likely over the next few years, decide to focus their expansion plans on Asia or the Middle East instead of Europe.

Next year, Miller warns, the UK’s funds industry will be hit by the double whammy of new MiFID II regulatory rules and the extra costs of preparing for Brexit: “MiFID II will already be a revolution for the industry. When you add to that the cost of Brexit, profits are going to be hit.”

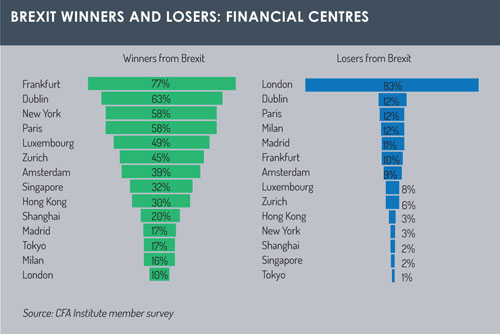

Miller’s fears for the industry are mirrored in the findings of a recent survey by the CFA Institute, which found investment managers in the UK, Europe and around the world are “overwhelmingly negative about Brexit”, according to Rhodri Preece, its head of capital markets policy.

The survey found that 70% of respondents in the UK believe that Brexit will cause the competitiveness of the UK asset management market to deteriorate.

It also found that over half (57%) of CFA member respondents around the world expect firms with a strong UK presence to reduce their operations in the UK as a result of Brexit.

Preece said that the extent of disruption to the industry will largely depend on whether politics allow current trading arrangements with the rest of the EU to continue.

“If we remain a member of the EEA, all of these issues that could impact the industry go away, but that would require the UK to accept continued freedom of movement of EU citizens, contributions into the EU budget and acceptance of the jurisdiction of the European Court of Justice,” he says.

“If the UK leaves both the EU and the EEA, then it will by default and in the absence of any alternative arrangements become a third country under EU law. If that were to happen, we would not be able to passport the full range of services that we are at present under Ucits.”

Even if the EU is prepared to regard the UK’s regulatory and supervisory regime as ‘equivalent’, which would allow cross-border trading to continue, this status could be withdrawn with just a month’s notice, Preece warns.

“There would be a significant degree of uncertainty and that does not form a good basis for a long-term trading arrangement,” he said.

Townsend Lansing, head of exchange-traded commodities at ETF Securities, fears that the distribution of cross-border funds could be seriously impacted if UK-based firms are unable to retain their current passporting licences post-Brexit.

“If Esma decides that firms need to have a heavy footprint within the EU, there might be a question over whether a company has enough boots on the ground in the EU,” he says.

“It could be the case that setting up a letterbox entity in the EU with just one employee will no longer be deemed acceptable. Firms may need to relocate sales, compliance and legal staff into offices in the EU in order to continue trading in the EU.”

Another scenario that could unfold, Lansing believes, concerns international fund firms with a UK presence who might decide to “up sticks and move” post-Brexit.

Another scenario that could unfold, Lansing believes, concerns international fund firms with a UK presence who might decide to “up sticks and move” post-Brexit.

“A Swiss firm that sells into Europe from London might decide to move to Frankfurt instead,” he says. Lansing is, though, reasonably upbeat about his own firm’s prospects. “If, over the next 12 months, it looks like there is going to be no post-Brexit deal, we are an agile company and can move quickly and open offices in the EU and have business continuity.

“This is not an existential crisis for us but there are likely to be increased costs and administrative hassle.”

Recruitment, however, has already become a headache for the firm. Lansing says that, since 2016’s Brexit vote, it has already become more difficult for City firms to recruit staff with European languages.

“Fewer Europeans are now looking to come to London,” he adds. “London has for years been one of the greatest examples of the EU working and the City became the EU’s financial gateway to the rest of the world. It is hard to see how that is going to continue.”

Aaron Stocks, a partner and head of listed funds at City law firm Travers Smith, also frets that the EU could take a more protectionist stance about equivalency regulation as Brexit negotiations progress and decide to “build a wall around the sale of investment products”.

“The worst-case scenario for the funds industry would be a hard Brexit combined with a government unwilling or unable to make tweaks to make it work,” he says.

“It is hard to underestimate the long-term impact on the funds industry if we get a hard Brexit and a government that imposes a migrant cap that restricts the number of bright young things that can come to the UK as that would lead to less innovation in the funds industry.”

The UK’s Conservative Party has long promoted itself as the most business-friendly of the country’s political parties, with many of its core policies geared towards wealth creation and expanding the private sector.

As the country heads towards Brexit, the party is in the uncomfortable position of having to implement policies that could, in the case of the financial sector as well as other industries, lead to sizeable job losses and wealth loss.

With polls of public opinion turning against Brexit, many are now wondering whether killing the goose that laid the golden egg is a price worth paying for an exit from the EU.

©2017 funds europe