As Australia deals with a Covid-driven economic slowdown, we ask funds professionals about the decisions that lie ahead.

The year 2020 has had a profound impact on the investment funds industry, forcing it to react to a health crisis and a global economic contraction that looks set to be the most severe for three-quarters of a century.

Australia’s economy contracted 7% in the three months to June, following a 0.3% decline during Q1, according to data from the Australian Bureau of Statistics and Trading Economics, forcing it into recession for the first time in 30 years. The Covid-19 pandemic has had a pernicious impact on the economy at large, and a debilitating effect on household savings and expenditure as Australian citizens in some regions adjusted to an extended period of lockdown.

This economic contraction has presented headaches for wealth managers as they reflect on where to target new distribution. Having fallen by 1.2% during Q1 2020 as the pandemic took hold, Australia’s household consumption plummeted 12.1% during the three months to June.

As part of its emergency support measures, the government announced extraordinary provisions to allow Australians to draw from their superannuation savings (AUD10,000 from April 20, 2020, with a further AUD10,000 if required after July 1, KPMG). The government planned initially to end this scheme on September 24, but it has subsequently extended it until December 31.

By the end of September, more than AUD33 billion (approximately US$24 billion) had been withdrawn from superannuation funds under this facility1. This will have an impact on assets under management, and therefore on scale efficiencies, within Australia’s superannuation sector. It will also force Australians to review their retirement planning as withdrawals from their superannuation pot erode the income that will be available to them in later life. In these circumstances, it is important that they have access to effective and affordable investment advice as we look beyond the health crisis.

Beyond Australia’s shores, the global economy and geopolitical environment present further uncertainties. Global real GDP has contracted 4.4% year-on-year to the end of October, according to IMF data2.

Beyond Australia’s shores, the global economy and geopolitical environment present further uncertainties. Global real GDP has contracted 4.4% year-on-year to the end of October, according to IMF data2.

The OECD reports that all G20 countries, with the exception of China, have suffered recession in 2020. Although a fragile recovery is expected next year, output in many countries at the end of 2021 will be below levels seen at the end of 2019, and well below that projected prior to the pandemic3.

Challenged with selling into this shrinking global economy, Australia’s exports fell by 4.4% and 6.7% respectively during the first two quarters of 2020 – although the trade balance has been boosted by an even sharper contraction in imports (6.7% in Q1, 12.9% in Q2) according to data from Trading Economics4.

The Australian government has reacted with an aggressive fiscal response to these difficulties, increasing government expenditure during the three months to June by a level (2.9%) not seen since Q4 1995. From the onset of the pandemic through to November, the Australian government has extended more than AUD250 billion in economic support to assist the vulnerable and to strengthen recovery5.

This disruption has triggered technology adaptation and changes in working practices that will have lasting effects for Australia’s investment funds industry. At short notice, the asset management world has adapted to remote working and rolled operational contingency arrangements into action that might have taken a decade or longer to deliver in normal times.

This will accelerate the digital transformation of the asset management industry – and the innovation that it offers to support fund sales, investment advice and client support through digital channels.

Post-Covid risks

To gauge the impact of the Covid crisis on Australia’s asset management industry, and to identify key trends for Australian investors, Funds Global Asia surveyed Australia-domiciled respondents from across the asset management industry. The results of these questions are summarised in figures A-G.

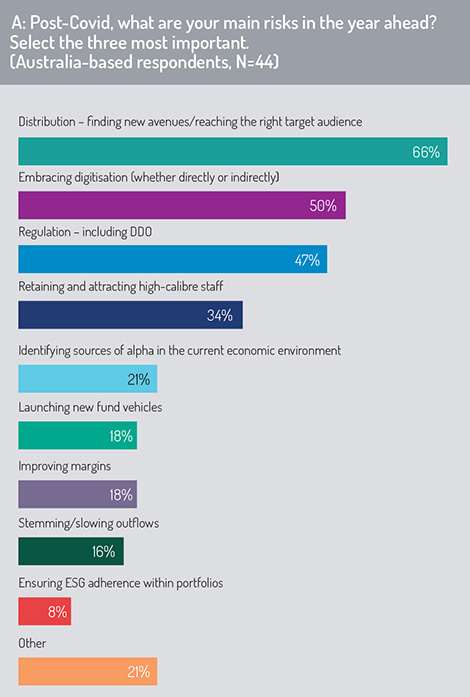

In this survey, we asked participants to reflect on the main risks that confront the asset management industry during the period of readjustment after the global pandemic (fig A).

Respondents to the Australia survey prioritised challenges with fund distribution – particularly in reaching the right target audience with their investment products and in opening new distribution channels – as they rebuild in the wake of the Covid-19 pandemic (66%).

These concerns have an explicitly regulatory component, given the Design and Distribution Obligations (DDO) and Product Intervention Powers (PIP) legislation that was enacted in the Australian market in April 2019. The DDO require issuers and distributors to have an effective product governance framework in place and to publish a ‘target market determination’, indicating which categories of investor will be targeted for sale of a specified investment product. The Australian Securities and Investment Commission (ASIC) has authority, using its intervention powers under PIP, to intervene when there is a risk of outcomes likely to be detrimental to the retail customer6.

Beyond this, respondents highlight the need for asset management firms and distribution partners to embrace digitisation to support efficient fund selection, trade execution and post-trade processing. This will be essential to meet the investment expectations of younger generations, many of whom expect to invest and to monitor their portfolio performance through fully digital channels.

Beyond this, respondents highlight the need for asset management firms and distribution partners to embrace digitisation to support efficient fund selection, trade execution and post-trade processing. This will be essential to meet the investment expectations of younger generations, many of whom expect to invest and to monitor their portfolio performance through fully digital channels.

Also, the survey highlights the challenge of attracting and retaining high-quality staff as the asset management industry in Australia adjusts to life after the pandemic (34%).

On a positive note, the survey finds little evidence that commitment to ESG principles will be reduced significantly by the pandemic. Only 8% of Australia-based respondents say that Covid-19 presents a risk to ensuring ESG adherence within investor portfolios.

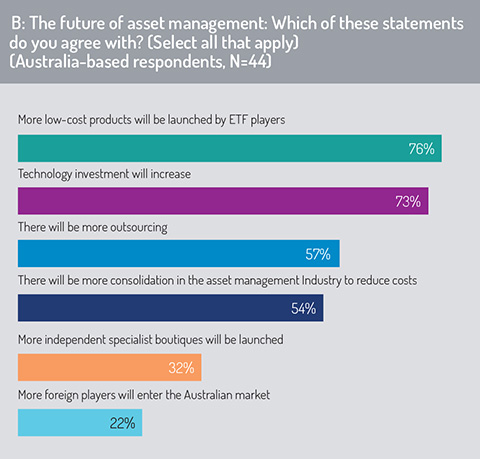

Looking more broadly at the future for Australia’s asset management industry, respondents predict that active managers will continue to experience strong competition from ETFs and low-cost ‘passive investments’ (fig B).

It comes as little surprise, as the industry reconfigures itself in the wake of the pandemic, that three longstanding drivers of innovation and cost management will feature prominently. The industry will look to technology to support new product development, efficiency gains and cost savings (73%).

More companies will outsource functions that they deem to be non-core, enabling them to replace fixed with variable costs and to focus on their core product or service expertise (57%). Thirdly, there will be further consolidation in the asset management industry to drive scale advantages and to reduce costs (54%).

Significantly, respondents do not expect to see a sharp rise in foreign asset managers entering the Australian market and seeking to capture market share (22%). The survey finds that Australian investors, both institutional and retail, will continue to focus a major share of their investment allocations towards fund management companies owned and headquartered in Australia.

1 – https://www.straitstimes.com/asia/australianz/australians-withdraw-billions-from-their-retirement-savings-to-cope-with-Covid-19

2 – International Monetary Funds, Real GDP Growth, Nov 2020, IMF Datamapper, https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/WEOWORLD

3 – OECD Economic Outlook, Interim Report Sept 2020, Building Confidence amid an Uncertain Recovery, https://www.oecd.org/economic-outlook

4 – https://tradingeconomics.com/australia/gdp-growth

5 – https://home.kpmg/xx/en/home/insights/2020/04/australia-government-and-institution-measures-in-response-to-covid.html

6 – Deloitte, DDO – ASIC Regulatory Draft Guide, https://www2.deloitte.com/au/en/blog/assurance-advisory-blog/2020/ddo-asic-draft-regulatory-guide.html

© 2020 funds europe