Alternative fund services are a salient feature of the 2013 responses to our third-party fund survey, finds Nicholas Pratt.

Alter Domus and Silica, two third-party fund administrators (TPAs) who appear in our annual survey and directory this year for the first time, underline an important trend in the market: the growth of services for alternative fund managers.

If it is just a coincidence that they appear in the survey in the same year as the Alternative Investment Fund Managers Directive comes into force, then it is a happy one.

The portfolio management, capital introductions and property services for fund managers provided by Apex Fund Services seem more akin to the typical prime broker services offered to hedge funds.

Other offerings focused on alternatives include Maitland, launching administration services for private equity and multi-manager funds, and Northern Trust, launching a hedge fund service. This includes a shadow administration model (see Funds Europe, January 2013) as well as enhanced collateral management capabilities and expanded support for sophisticated management and performance fee calculations.

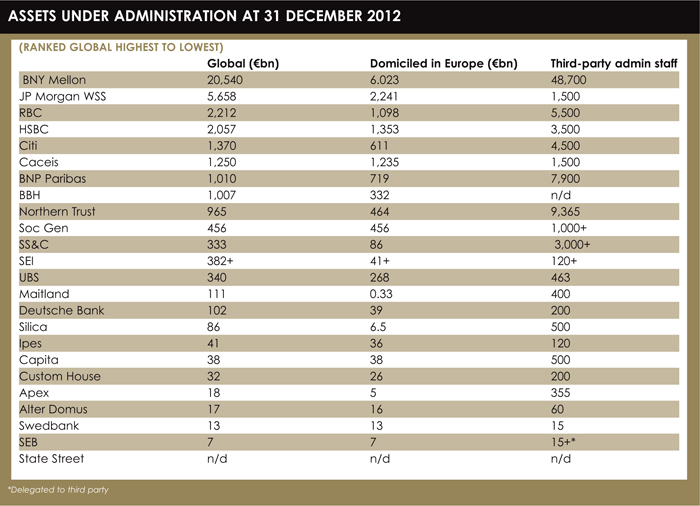

Our survey and directory for 2013 – which has grown to feature 22 providers – shows that new products and services being developed by TPAs seem to be reliant on continued growth in the asset management industry, whether the launch of new funds (especially alternative funds), or the distribution of existing funds into new territories.

Our survey and directory for 2013 – which has grown to feature 22 providers – shows that new products and services being developed by TPAs seem to be reliant on continued growth in the asset management industry, whether the launch of new funds (especially alternative funds), or the distribution of existing funds into new territories.

Several TPAs, such as BBH, talk of the need to provide distribution support services as well as ancillary services such as broader foreign exchange offerings and cross-border distribution support.

But amid this business activity, the survey also reveals a reduced emphasis on international expansion compared with 2012. What expansion there is will focus on filling gaps in coverage, at least in Europe. For example, Citi has focused on the Netherlands and Sweden. Meanwhile, others, such as Custom House and Ipes, are targeting Switzerland, the largest non-EU market in Europe.

But the majority of the focus is on areas outside Europe, notably Latin America, Asia (Japan, Singapore and China) and the US. There is also the Middle East, but this was mostly a market that TPAs looked to expand into 2012, if not before.

IMPACT

Collateral management is also a focus, as evidenced by BNP Paribas Securities Services, which in 2013 is upgrading its global custody offering to include support for tri-party collateral management asset optimisation services for collateral management and securities lending. Other TPAs, such as BNY Mellon, are looking to ascend the value chain by offering front-office services such as trade execution. They are also developing central security depositary (CSD) services, perhaps mindful of the opportunities that the T2S project to boost the European post-trade infrastructure, and measures to introduce central clearing for derivatives, presents them.

However, as Hani Kablawi, head of Europe, Middle East and Africa asset servicing at BNY Mellon, says the fact that regulators are still drafting and consulting on proposed reforms around market infrastructure does make it more challenging to develop appropriate services.

“There is uncertainty as to how this will reshape the post-trade landscape, but we continue to monitor events to assess probable impacts, and are investing significant resources into planning for future reform.”

The 2012 survey revealed the increasing pressure on TPAs, whose clients wanted more services at a lower cost. One year on, this pressure still appears to dominate the landscape.

Peter Hughes, global managing director at Apex, says: “New fund managers have a greater expectation of their service providers to shoulder regulatory burdens, assist with transparency, complete a wider range of tasks and, at the same time, offer cost savings and operational efficiencies.”

Peter Hughes, global managing director at Apex, says: “New fund managers have a greater expectation of their service providers to shoulder regulatory burdens, assist with transparency, complete a wider range of tasks and, at the same time, offer cost savings and operational efficiencies.”

A number of TPAs talk of a changing business model as a consequence of the cost pressure created by the regulatory burden where there is greater emphasis on operational outsourcing.

Catherine Brady, head of Emea fund services at Citi, says clients want “operational alpha” as they look to achieve a “sustainable business model through best-fit partnerships that bring high technology and data driven solutions”.

She also says that “a small number of players in the market are aiming to consolidate, resulting in price decay and P&L pressure for everyone”.

The challenges for independent administrators, as opposed to the bank-owned global custodians, are more severe though, notes Mark Hedderman, chief executive at Custom House. “Clients are expecting more from the administrator and the original product that was fund administration is now completely different. Therefore, you have to redesign your operating model and its capabilities.

“Increased regulatory burdens on managers and funds is leading a return to a more consolidated service model option and the challenge to display true added value is even greater.”

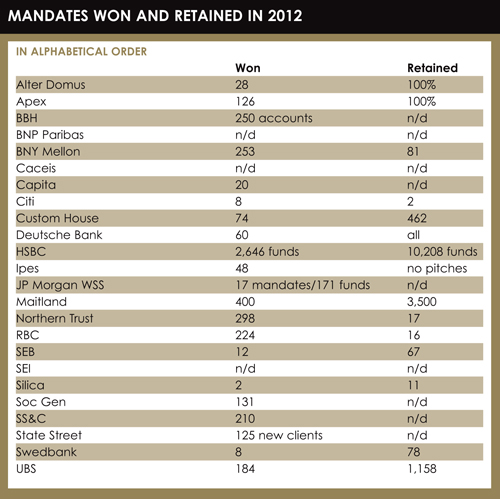

Custom House was the only TPA to report a negative inflow in the survey, which it ascribed to the loss of a top-ten client.

Certainly, it seems that fund managers have realised the position of power they hold in such a competitive environment, resulting in more of them going to tender rather than re-appointing the incumbent, says Justin Partington, commercial director at Ipes. However, he says that there is a bifurcation on pricing – “it is either the main criteria or not important at all” – and that technology is an increasing focus on pitch situations.

Competition is also likely to lead to consolidation, says Andre le Roux, head of business development at Maitland. “We see continued consolidation and thus competition for acquisition targets. As an acquirer, the expectation of price is often unrealistic. From an operational perspective, the ability to roll out value-added services and move up the value chain is the industry’s biggest challenge.”

There does seems to be more focus on technology from TPAs. Michale Prentice, chief executive officer at Silica, mentions the use of straight-through processing to enable advanced data presentation and enhanced customer experience and is investing heavily in automated rules engines and workflow.

BALANCE

Meanwhile, Mark Porter, global head of fund services at UBS, says that clients’ most common demands, as a result of the continued requirement for transparency and real time information, are for customised reporting, technology connectivity, and advanced risk management techniques. This is creating a healthy pressure on pricing in all parts of the value chain in order to enable investors to produce sustainable returns.

“All industry participants must, therefore, continue to evolve their efficiency and automation programs to achieve this.”

It is a case of looking for new sources of revenue wherever they may be. “As the profit margins are tightening on pure custody products, we see increased revenue potential on new products, such as Sicav-solutions to asset managers who want to focus on sales and investments,” says Aet Rätsepp, head of fund services, Swedbank.

The fund administration business has fundamentally changed over the years, particularly in Europe, to a model of bundled services to address the growing number of services required by managers, says Mike Hughes, managing director, global head, alternative fund services at Deutsche Bank.

“Basic back-office services have been commoditised and expectations are ever higher that fund administrators and service providers will offer increasingly sophisticated and customised reporting and analytic tools. Flexibility in platform architecture is what makes meeting these demands an efficient and positive experience for our clients.”

According to Pascal Berichel, global head of fund operations at Societe Generale Securities Services, improving operational efficiency is a key concern. The challenge for TPAs is to somehow find a balance between developing new expertise, managing expenses lowering costs through standardisation, but also retaining the ability to meet client-specific requirements.

For fund managers reviewing their TPA arrangements, it is also a question of balance: seeking a competitive price and using the tender process to drive this competition but also ensuring that the chosen provider has invested enough in its offering to meet specific requirements.

©2013 funds europe