In a volatile market, investors are increasingly looking for a new approach to equity investing. Smart beta solutions can answer their needs says Alessandro Russo, head of factor investing at Amundi.

While the performance of stock markets has been strong since the financial crisis, a more sophisticated approach is now required. The volatility of financial markets in the last 12 months highlights the current challenges. Risks of lower economic growth are curbing the medium-term return potential of equities while bouts of volatility threaten to erode the value of the portfolio.

Investors are increasingly looking for a new approach to equity investing to make the most of available risk premia and to minimise the impact of market volatility on a portfolio. Smart beta solutions can answer these needs, as they provide improved diversification compared with market capitalisation-weighted indices by addressing many of their limitations. These products aim to help investors reduce volatility and access potentially better returns as well as mitigate losses in bear markets.

CHARACTERISTICS OF FACTOR INVESTING

An investor can access a more diversified exposure to stocks and shares using index construction techniques which take a more risk balanced approach. This could include building an index by equalising the risk contribution of individual stocks, minimising volatility or maximising a diversification measure.

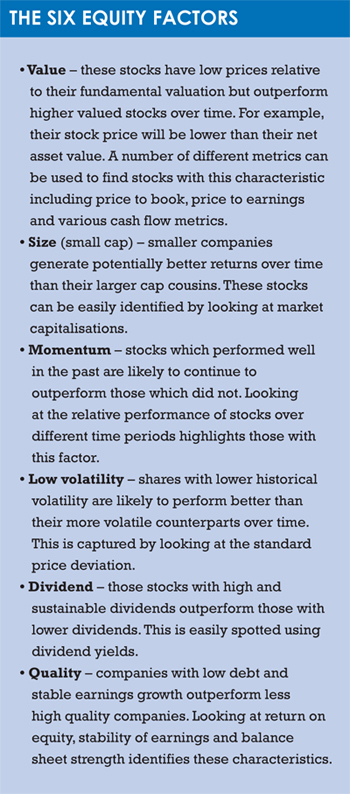

An even better risk-return profile can be achieved by tilting a portfolio towards stocks with certain characteristics. Academic research1 has shown stocks with specific characteristics can have consistent risk premia, known as investment factors. These include size, value, momentum, low volatility, quality and dividends.

IMPROVING THE RETURN PROFILE OF A PORTFOLIO

Constructing a portfolio which tilts towards these investment factors can improve performance compared to market-cap weighted indices because it allows investors to capture additional returns. As well as capturing the equity risk premium, they will also capture the additional risk premia associated with these investment factors.

Not only investment factors are expected to generate better potential returns than the overall market, some factors can also reduce the volatility of the equity portfolio, particularly the quality and low volatility factors. By including these in the portfolio tilt, investors can somewhat mitigate the risk profile of their portfolio.

Investors can increase portfolio diversification by adding more than one factor into the portfolio. As demonstrated by academic research¹, factors will show different performances at different points of the economic cycle. An exposure to a broad set of factors can improve the ability of the portfolio to generate alpha, irrespective of the economic cycle. This would reduce the likelihood of underperformance.

The exposure to different factors can also be managed dynamically, according to the economic cycle (see Fig 1). For example, during the first two quarters of the year, several indicators were suggesting world economic growth could decelerate. In such an environment, defensive factors like low volatility and high dividend could be useful asset allocation choices. From the end of 2015 to the end of June 2016, those investment factors have been the best performers², illustrating the benefit of allocating to these factors when there is a risk of a slowdown in economic growth.

The exposure to different factors can also be managed dynamically, according to the economic cycle (see Fig 1). For example, during the first two quarters of the year, several indicators were suggesting world economic growth could decelerate. In such an environment, defensive factors like low volatility and high dividend could be useful asset allocation choices. From the end of 2015 to the end of June 2016, those investment factors have been the best performers², illustrating the benefit of allocating to these factors when there is a risk of a slowdown in economic growth.

More recently, with improvement of the macroeconomic output, and with softening concerns about Brexit, more dynamic factors such as value and mid-cap are closing the gap³.

If, however, the outlook should worsen and a recession seemed probable, then low volatility and quality factors should be considered. When a recovery seems imminent, a shift to small cap and value stocks would produce better returns. And if economic growth starts to accelerate, high momentum stocks are more likely to outperform4.

By using the economic cycle to manage the factor portfolio dynamically, investors can generate better returns, compared to a portfolio with a static investment factor allocation

RISK CUSTOMISATION

The customisation of an investment factor portfolio can be taken further than managing a multi-investment factor portfolio dynamically – weighting can be defined by risk budgets. An investor can take the straightforward approach of allocating equally to each investment factor. Or they can decide to allocate weighting in compliance with a particular set of desired contributions to portfolio risk, which could be an absolute target or one relative to a market-cap weighted index.

Another risk approach is to apply the benefits of alternative index construction tools to an investment factor portfolio. Stocks are selected according to a particular or to several investment factors and the portfolio is constructed using weighting metrics such as risk parity, minimum volatility or maximum decorrelation. This would produce a more risk-balanced investment factor portfolio. These portfolios combine both ‘smart beta’ approaches: they use more risk balanced portfolio construction tools as well as accessing known sources of risk premia.

DO-IT-YOURSELF

Investors can now choose from a range of ‘smart beta’ products that allow them to access individual or combinations of investment factors. However, exchange-traded funds are one of the most useful product ranges available as they give cheap, highly liquid and transparent access to these factors.

The simplicity and range of products allow investors to use these vehicles as building blocks to construct a portfolio to meet their specific investment criteria.

Moreover, there is constant ETF product innovation which gives investors access to a broad and evolving investment toolkit.

Footnotes:

1 – Amundi Quantitative Research: ‘Equity Factor Investing according to the macroeconomic environment’, November 2015

2 – Amundi Quantitative Research: Performance monitor between 31/12/2015 and 30/6/2016

3 – Amundi Quantitative Research: Performance monitor between 30/06/2015 and 31/10/2016

4 – Source: Amundi Smart Beta Academy

Investment in a Fund carries a substantial degree of risk. The price and value of investments can go down as well as up. Investors may not get back the original amount invested and may lose all of their investment. Past performance is not indicative of future results, nor does it guarantee future returns. The performance data presented does not take into account the commission and costs incurred on the issue and redemption of units.

For professional investors only. This document is not intended for citizens or residents of the United States of America or to any «U.S. Person» , as this term is defined in SEC Regulation S under the U.S. Securities Act of 1933 and in the Prospectus of the funds mentioned in this document. This material does not constitute investment advice. Financial promotion Issued by Amundi Asset Management, SA with 596 262 615€ of registered capital, an investment manager regulated by the AMF under n° GP 04000036. Registered office address: 90, Boulevard Pasteur 75015 Paris Cedex 15 – France – 437 574 452 RCS Paris.