In our final survey of fund professionals’ attitudes towards emerging markets in conjunction with Amundi, investors seem certain about which regions and assets offer the best opportunities – and the best way to access them.

It’s been a year of some upheaval in emerging markets, with new countries ascending to the sphere, such as Pakistan in June, and others – including the flagship Brics (Brazil, Russia, India, China and South Africa) grouping –– being battered by economic and political tumult.

While the results indicate investors haven’t given up hope on emerging markets, some portions of the map are viewed more positively than others. Latin America has been drawing lower interest from investors, it seems – a mere 7% ranked it as the emerging region in which they were most interested, far behind other developing prospects.

Nevertheless, Pierre Gielen, Emerging Markets Investment Specialist at Amundi, wasn’t surprised by the result, given the economic and political challenges that lie ahead for Latin America’s major economies.

“In Brazil, much needed fiscal consolidation is likely to dampen consumer sentiment, while Mexico is in the process of assessing the consequences of the protectionism stance in Washington,” he says.

China has also lost its lustre with investors. Sentiment turned against the country following its bout of stock market turbulence in August last year (dubbed ‘Black Monday’), and is evidently yet to recover; the country is only cited by 11% of investors as the most interesting emerging market.

Conversely, India still elicits significant interest. The results echo Amundi’s own stance.

“Even though we could have a short-term hit to GDP growth following Prime Minister Narendra Modi’s reforms, we stick to the view that India is going to get out stronger and we are out for buying some selected stocks,” Pierre says.

Moreover, Asia (ex-China) as a whole is still of great interest to investors. As Pierre explains, the region has a strong, installed manufacturing basis, positive current accounts and large foreign currency reserves. Even if Donald Trump pursues policies inimical to globalisation, the region’s central banks will have relatively larger leeway to manage the adjustment in the event of more USD strengthening.

Investors seem most interested in emerging markets as a global play, consistent with Amundi’s view that global emerging portfolios bring investors built-in diversification and better risk-adjusted performance. In a universe of 23 countries, investing broadly means accessing different positioning in the growth or monetary cycle simultaneously.

FIXING INCOME

While investors were almost evenly split on the debt sectors of most interest to them, local currency debt reigned supreme, with 36% favouring it. Abbas Ameli-Renani, global emerging markets strategist at Amundi, suggests this reflects investors’ perceptions of valuation.

“Emerging market local debt has had a negative total return of 20% since January 2013, compared to a total return of 12% for dollar-denominated debt. As such, valuations appear much more compelling on the local debt side,” he says.

“However, we are of the view that hard currency debt continues to offer investors the best risk-adjusted return prospects in the medium term. This is particularly the case after the election victory of Donald Trump and the likely positive impact that his presidency will have on the US dollar. In such an environment, investors’ gains from yield can be wiped out from losses on the currency side. With hard currency debt in comparison, the key driver of returns is likely to be emerging market fundamentals, which we see undergoing significant improvement.”

“However, we are of the view that hard currency debt continues to offer investors the best risk-adjusted return prospects in the medium term. This is particularly the case after the election victory of Donald Trump and the likely positive impact that his presidency will have on the US dollar. In such an environment, investors’ gains from yield can be wiped out from losses on the currency side. With hard currency debt in comparison, the key driver of returns is likely to be emerging market fundamentals, which we see undergoing significant improvement.”

Given the election of Trump, and the potential uptick it could produce in the dollar, it is perhaps surprising there is not more interest in investment grade corporate debt, as much of the market is comprised of offerings from businesses with significant exposure to the US.

STAYING ACTIVE

Over 2016, there has been a deluge of data questioning the value of active managers. On an almost monthly basis, new studies indicate the vast majority of fund managers in almost every sector consistently fail to beat their index. October’s instalment was delivered by S&P’s active-vs-passive scorecard, Spiva; it showed 99% of active US equity funds, 98% of global equity funds, 97% of emerging market equity funds and 90% of European equity funds hadn’t beaten their benchmarks since June 30, 2006.

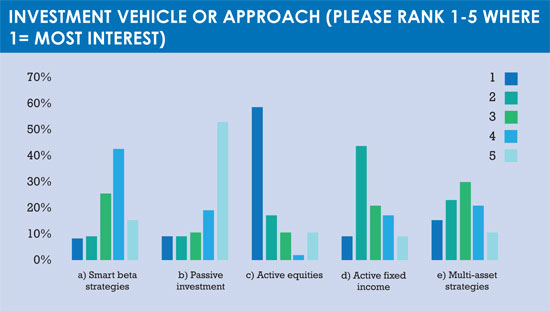

However, investors continue to overwhelmingly favour active equity strategies as a means of investing in emerging markets, with 59% most interested in such strategies, and 53% being least interested in passives. Amundi agree emerging markets are still a place where active funds make sense and can add value. Their own outperformance in the field is a testament to this.

“We have been able to outperform through our proven approach of combining a focus on domestic demand led economies and picking stocks with a solid growth outlook, high cash flow-generative and best-in-class corporate governance, all criteria that we believe support stock prices across the cycle,” Pierre says.

Another reason investing via passive is ineffective when it comes to emerging markets, Pierre says, is that tracking an emerging markets index leads to investment in large, unprofitable swathes of industries, sucking investors into a value trap.

Equities are also far and away the most interesting asset class for investors, with only 9% being most interested in fixed income, and 15% in multi-asset strategies.

Disclaimer: In the European Union, this document is only for the attention of “Professional” investor as defined in Directive 2004/39/EC dated 21 April 2004 on markets in financial instruments (“MIFID”), to investment services providers and any other professional of the financial industry, and as the case may be in each local regulations and, as far as the offering in Switzerland is concerned, a “Qualified Investor” within the meaning of the provisions of the Swiss Collective Investment Schemes Act of 23 June 2006 (CISA), the Swiss Collective Investment Schemes Ordinance of 22 November 2006 (CISO) and the FINMA’s Circular 08/8 on Public Advertising under the Collective Investment Schemes legislation of 20 November 2008. In no event may this material be distributed in the European Union to non “Professional” investors as defined in the MIFID or in each local regulation, or in Switzerland to investors who do not comply with the definition of “qualified investors” as defined in the applicable legislation and regulation. This document neither constitutes an offer to buy nor a solicitation to sell a product, and shall not be considered as an unlawful solicitation or an investment advice. Amundi accepts no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi can in no way be held responsible for any decision or investment made on the basis of information contained in this material. The information contained in this document is disclosed to you on a confidential basis and shall not be copied, reproduced, modified, translated or distributed without the prior written approval of Amundi, to any third person or entity in any country or jurisdiction which would subject Amundi or any of “the Funds”, to any registration requirements within these jurisdictions or where it might be considered as unlawful. Accordingly, this material is for distribution solely in jurisdictions where permitted and to persons who may receive it without breaching applicable legal or regulatory requirements. The information contained in this document is deemed accurate as at the date of publication. Data, opinions and estimates may be changed without notice. You have the right to receive information about the personal information we hold on you. You can obtain a copy of the information we hold on you by sending an email to [email protected]. If you are concerned that any of the information we hold on you is incorrect, please contact us at [email protected] Document issued by Amundi AM, a société anonyme with a share capital of € 746 262 615 – Portfolio manager regulated by the AMF under number GP04000036 – Head office: 90 boulevard Pasteur – 75015 Paris – France – 437 574 452 RCS Paris www.amundi.com