Sionic’s managing partner and co-head of the asset management practice, Paul Sutton, and Ashley Sheen, director in its asset management practice, weigh up the opportunities for asset managers and service providers arising from the adoption of a common technology platform for their end-to-end investment value chain.

Front-office decision-making and reporting tools require an increasing breadth and depth of accurate data which must be delivered closer to real time. This must be achieved in an environment where fee pressures are forcing asset managers to look at their costs and service providers are seeking opportunities to protect or improve the sustainability of their earnings.

Change is underway, but global operating models are complex owing to the number of asset classes, products, range of clients, jurisdictions and technologies these must bridge.

Fragmentation of business processes, and a lack of interoperability between systems and strategic suppliers, increases operational risk and reduces end-to-end resilience. Inefficiencies in the value chain drive headcount to manage STP breaks and errors. However, there is potential for a “win-win” for asset managers and service providers that can reduce this manual overhead by optimising data management across the end-to-end investment value chain.

How is the industry evolving?

More firms are deploying a common technology platform for the entire investment value chain. A core objective is to integrate portfolio management, servicing and reporting for traditional asset classes, as well as bringing in data from alternative investment verticals which may have their own platforms, to create a holistic overview. A common model also supports multi-asset, liability-driven investment (LDI) and ESG solutions.

The market activity to meet the endgame is dependent on the strategic gaps to be addressed by individual players – albeit with common themes. BlackRock chose to address the horizontal challenge and extend its coverage in the alternative space – it did so by acquiring eFront in 2019 where the rationale, in its own words, was “to make alternatives less alternative and enable a whole portfolio approach”. State Street, meanwhile, chose to focus on addressing the vertical challenge by acquiring Charles River’s front-office systems in 2018. The goal was to create a global front-to-back platform to support workflows across the investment lifecycle, providing data aggregation, analytics and compliance tools, along with the ability to exchange data with other industry participants.

Similar forces are at play across the market with the global providers seeking ways to deliver business services directly into their clients’ common front-to-back applications. This has been seen where several asset servicing providers (including BNY Mellon, BNP Paribas Securities Services and Northern Trust) have entered into strategic alliances with the likes of BlackRock, Bloomberg AIM and SimCorp to deliver integrated investment management capabilities to mutual clients. This enables the service provider to join middle-office outsourced services directly to clients’ front-end tooling and investment book of record.

Leading front, middle and back-office applications differ substantially in terms of how they function within a front-to-back model.

Leading front, middle and back-office applications differ substantially in terms of how they function within a front-to-back model.

A critical question is whether the need for a functionally rich data set to support the front office can be met by a common data model in order to deliver both efficiencies through simplification, and value from reliable, suitably timed and clearly tagged data sets along the value chain. Asset managers are differentiating their capabilities from an investment and client-servicing perspective through their choices in respect of data sourcing, data enrichment and means to generate a harmonised core data set that will drive value creation across the investment lifecycle.

But moving towards this single end-to-end model, supported on a small set of common platforms, will demand difficult compromises from service partners regarding the segregation of data responsibilities. A greater responsibility for investment data brings with it the challenge of sourcing a richer set of attributes. The challenge of providing this information intraday takes service providers away from the comfort of an overnight batch validation process, bringing with it fresh operating model considerations.

This approach, therefore, can be a double-edged sword. For asset managers, the benefits are a simplified model that can deliberately bring focus into the operational architecture, reducing the size of the application footprint and the requirement for interfaces between different platforms and components. As a consequence, it may shorten turnaround times for data queries and drive a marked improvement in data quality. It may also reduce operational risk and people costs. For service providers, a deeper integration with the asset manager technology reduces integration friction, and a broader data-servicing opportunity is presented to those with the right ambition, tools and operating model.

The flip side is that front-to back applications poorly selected and implemented can be a straitjacket, forcing suboptimal components onto user communities without offering the user-friendliness and functionally rich experience of a best-of-breed approach.

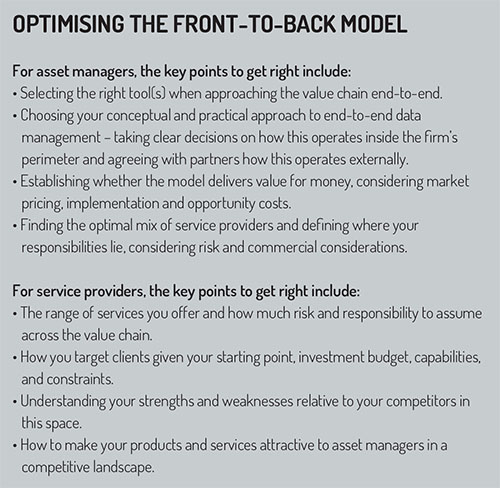

It is therefore vital to select the right tool for the firm, recognising its current and future requirements and its need to align with the technology and service infrastructure of outsource partners.

Single data model

So, what are the challenges in moving to an optimised front-to-back investment operating model? Firms rarely start with a clean slate and these choices are shaped by the systems, operational processes and outsource partners they already have in place. In some cases, the cost and level of disruption involved, and difficulty of getting all stakeholders over the line, may outweigh the potential benefits. The target is to operate a single data model that supports the data requirements of all modules. This central common, complete and consistent investment data architecture can then be supplemented and customised to support other business functions as required.

While a best-of-breed approach (common in legacy data models) may allow data optimisation within modules or business silos, inconsistencies in data format across modules have presented a challenge for data reconciliation – a reconciliation burden that adds friction and cost to these legacy data models.

Regardless of the asset manager’s intent, a constraining factor will be the ability (and appetite) of existing strategic outsource service providers to adapt their technology and operating models. This includes their capacity to meet data and functional challenges as the industry innovates in areas such as distributed ledger technology, robotics and artificial intelligence. Service providers can be a help or hindrance in meeting this objective. Furthermore, their starting point and ambitions in this regard are differentiated, therefore choosing the right providers to match your strategic aims is critical.

A fundamental question in a shared platform environment is how to manage the division of responsibilities across service partners – and where to draw the line for business processes, technology control, data quality and assurance.

© 2020 funds europe