The AIFMD heralds a massive change in the way alternative investment funds are marketed and administrated. With the effect on fund servicing centres likely to be huge, jurisdictions have already started to evolve.

Nicholas Pratt asks if developing niche specialisms will help them to survive and thrive.

Is Europe’s changing landscape for the regulation of alternative investments likely to drive demand for a one-stop-shop fund domicile and favour larger fund centres such as Ireland and Luxembourg?

Yes, according to a 2014 study from consultant Oliver Wyman called Domiciles of Alternative Investment Funds. The Alternative Investment Fund Managers Directive (AIFMD) is a growth driver for these jurisdictions, it concluded.

AN AID TO GROWTH

The ‘one-stop-shop’ notion is at odds with how things are now. Luxembourg is the strongest player in terms of Ucits funds marketed across international borders. However, it sees funds regulated by the AIFMD as a major pillar of growth.

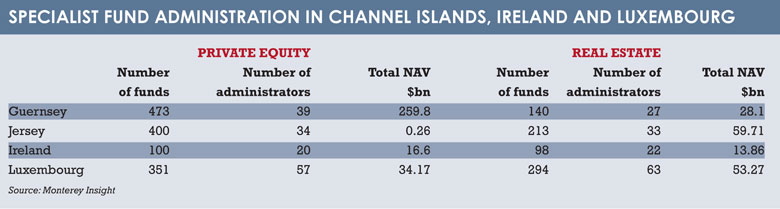

At the same time, Ireland is a hedge funds leader and the Channel Islands’ reputation lies in private equity and real estate.

So how might domiciles respond to the one-stop-shop challenge, if it even makes sense to? In particular, how will smaller players such as the Channel Islands – not to mention Malta, which has shown the biggest percentage of growth in alternative assets under administration in the past few years – position themselves?

LUXEMBOURG

According to Claude Niedner – chairman of the alternative investment funds technical committee at the Association of the Luxembourg Fund Industry – if Luxembourg is to maintain its status as an attractive destination for specialist fund administration, the focus has to be on regulating managers, rather than products.

This principle was behind the development of the Société en Commandite Spéciale, or SCSp, a special limited partnership similar to the Anglo-Saxon limited liability partnership. or LLP, he says. “It has been a significant development and a boost to real estate and private equity funds. The benefit is that you have a flexible vehicle that is quicker to market and qualifies for the EU passport.”

In terms of new and emerging alternative asset classes, Niedner – a partner at law firm Arendt & Medernach – says Luxembourg’s strategy is to develop categories for new fund types or asset classes of any significance, rather than target one niche area. “It is likely that administrators within Luxembourg will adopt a similar strategy – to offer bespoke services for some of the new asset classes but also maintain an element of diversity in their asset class coverage,” he adds.

IRELAND

With more than 12,500 funds administered, Ireland is administrator to a broad range of fund types and asset classes, says Pat Lardner, chief executive of the Irish Funds Industry Association (IFIA). That said, growth in alternative assets means alternative funds account for 23% of funds domiciled there. Within that group, hedge funds are a clear strength for Ireland: it administrates for 40% of this type of fund worldwide.

He says the broad strategy is to attract funds in general rather than specific types. As well as legislative steps to help grow its book of alternative business (both domiciled and non-domiciled funds, for which Ireland provides administration), Ireland has launched the Irish Collective Asset Management Vehicle (Icav), too. The Central Bank of Ireland has also created a framework for loan origination to capitalise on interest in non-bank funding within the EU. And, says Lardner, the Finance Act passed in 2013 introduced real estate investment trusts.

“One of the dangers is that you might concentrate on an area that turns out to be a fad. A better approach is to continue to have a broad spectrum of supporting services to cover both liquid and illiquid funds, traditional and alternative investment strategies,” he says.

MALTA

Malta’s funds industry is just 20 years old and for the first half of its life, funds were predominantly vanilla. That changed in 2000 when the Malta Financial Services Authority introduced Sicav and LLP structures for alternative funds. The major growth in the past five to seven years has been in these alternative funds, says Kenneth Farrugia, chairman of Finance Malta.

The total net asset value of Malta-domiciled funds at June 2014 was €9.7 billion. In the past two years there has been a broad growth of specialist funds, from global macro to arbitrage strategies, and infrastructure and real estate funds. Diversified funds make up more than 40% of assets under administration. Malta also enables managers to set up funds that may not have significant seeding, between €30 million and €50 million.

However Farrugia, who is also chief business development officer at Bank of Valletta, rejects the notion that Malta is principally a low-cost alternative to the likes of Luxembourg and Dublin. He is careful to point out that managers look at more than just cost when setting up funds or looking for administrators.

Farrugia is aware of just how mobile the industry can be and is therefore wary of trying to develop new niches in case existing business is adversely affected. “For fund administration within Malta, it is important that we remain relevant to the funds we are servicing and do not become too impatient in an effort to attract new funds,” he says.

“If you grow too quickly, you can alienate your existing client base and they will move to a new jurisdiction.”

CHANNEL ISLANDS

Jersey is best known for real estate funds, given its links to the UK and EU property markets. Guernsey is better known for private equity administration. In the past 30 years, both have built a portfolio of specialist support services – and the relationship between them is competitive.

“People often look at the Channel Islands as one jurisdiction, but there are different approaches,” says Peter Rioda, head of the strategy committee at the Jersey Funds Association (JFA). “I would say that Jersey has a more streamlined approach to regulation and is better placed for smaller, private funds.”

Joseph Truelove, vice-chairman of the Guernsey Investment Funds Association’s executive committee, says: “Our strategy is to keep doing what we’ve always done well, which is being open and adaptable to innovation with respect to new asset classes, legal structures and changes to regulations while opening new markets.”

However, offshore jurisdictions will have to rethink their strategy should private placement be ruled out under the AIFMD in 2018. In such an instance, alternative investment funds from outside Europe may not be able to market to European investors. But Rioda points out that fund passporting requirements are still to be made clear by the European Securities and Markets Authority. “Ideally, we will still be able to cater for alternative funds that are not marketed to European investors – that is, non-AIFMD products,” he says.

THE ADMINISTRATORS

Clearly, Ireland and Luxembourg are pushing for the one-stop-shop offering, as evidenced by new vehicles. But so too is Malta, it appears, with its support for a wide range of investment strategies. The Channel Islands may emerge as an offshore specialist.

So, how do the administrators feel fund managers should approach domiciles with their particular strategies?

Choosing the right domicile for the underlying asset class is an essential step in a successful specialist fund launch, says Sebastien Danloy, head of continental Europe and offshore managing director at RBC Investor and Treasury Services, which has a large presence in both Luxembourg and Dublin.

The fact that both domiciles continue to develop initiatives to support alternative asset classes is particularly important, he says. For example, real estate investment trusts and investment limited partnerships were introduced in Ireland in 2013. Meanwhile, the already-mentioned Icav will come into use in 2015.

Luxembourg has also become a strong domicile for real estate funds, Danloy says, while its strong heritage in Ucits has created an attractive environment for alternative hedge fund strategies packaged in the wrapper.

Alan Dundon, chief marketing officer at fund administrator Alter Domus, which started as a Luxembourg player but is now in 16 jurisdictions, says: “As an administrator, the first thing we ask when setting up in a new domicile is whether we will get clients when we open on day one.

“So rather than set up and hope for clients to follow, we would first have a major client that wants us to set up there.”

Other typical factors include the level of expertise, the extent of competition from both local and international administrators and the flexibility of the fund vehicles. For administering alternative funds, says Dundon, the ability to cater for both the fund and underlying special purpose vehicles, or SPVs, is a key attraction for private equity and real estate funds, as is the case in Luxembourg.

Alter Domus has also opened an office in Malta. As Dundon describes it, the jurisdiction is an up-and-coming centre for specialist fund administration that offers many of the same benefits as Luxembourg but on a smaller scale and in a lower-cost environment. Malta has also issued new rules for debt funds, an asset class that is experiencing growth.

“The administration of a debt fund requires different profiles and systems, so we have set up a new segment for this asset class. The private debt guys have a real in-depth knowledge of this asset class – they often come from a PE [private equity] or RE [real estate] background, so it is not just the fees but the all-round package. And while Malta has issued new rules around debt funds, the lion’s share of administration is still in Luxembourg, and that is where we would primarily look to service debt funds.

FUND REVIEW

Elian is a provider of corporate and fund administration services, historically concentrated in offshore jurisdictions such as Jersey, Guernsey and the Cayman Islands. In 2013, it opened a Luxembourg office in response to the various regulatory developments and to act as a hedge against the AIFMD’s implications for traditional offshore centres, says group director, Paul Lawrence.

“It is perhaps too early to tell what the full effect of the AIFMD will be, but what we have not seen is any significant redomiciling of existing funds from offshore to onshore,” he adds. “We are, though, seeing more review around where managers will establish their next fund.”

Lawrence says fund domiciles are all about the substance behind their national brand. It is too simplistic to put a fund in a jurisdiction just because it is in the EU and the AIFMD remit, he says. Legal and accounting skills and expertise, the availability of qualified directors and the ability to attract and retain staff on the ground are all important factors.

Because of these requirements, Lawrence believes it will be very difficult for the likes of Malta, Cyprus or other smaller EU fund domiciles to challenge the onshore strongholds of fund administration, namely Ireland, London and Luxembourg.

“Bringing in more jurisdictions does create more competition, but it cannot be a race to the bottom in terms of quality,” he says. “Regulation has to achieve its objective of better investor protection.”

©2015 funds europe