When the snow melts next spring, Russia’s capital markets could look completely different. With reforms in full swing and Moscow’s standing in the world elevated after the chemical weapons tragedy in Syria.

Dividends make investors in Russian equities feel more secure about an emerging market they find hard to trust. The dividend payouts are the trade-off for taking risk on companies that have poor corporate governance.

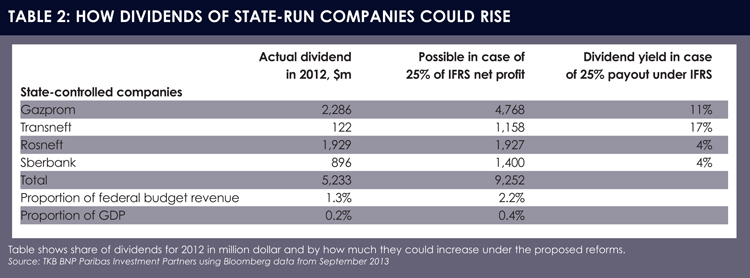

Under a new dividend policy, state-controlled companies will have to pay out 25% of profits made this year, a calculation based on International Financial Reporting Standards, when dividend payments are due in spring next year.

Those dividends could rise to 35% of profits by 2016.

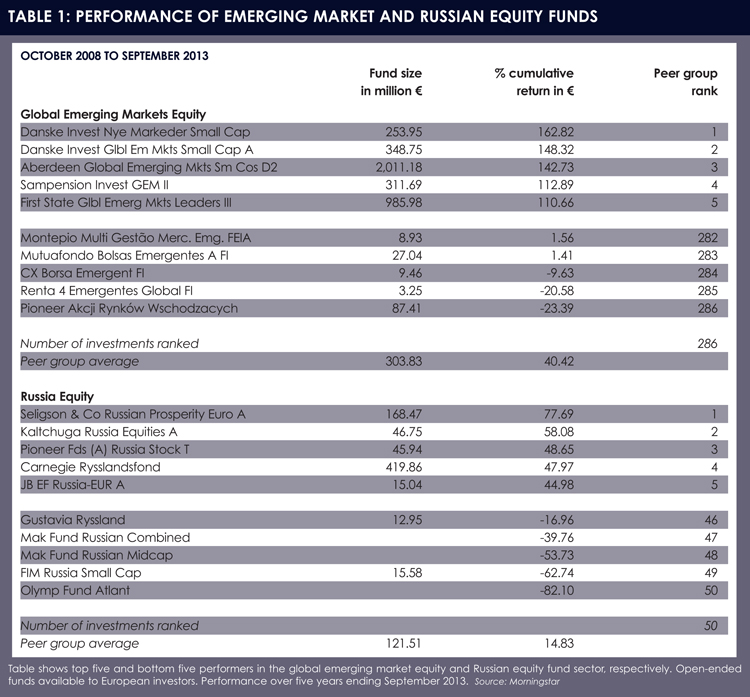

Even though Russia-focused funds have underperformed global emerging markets for years (see table 1), Bank of America Merrill Lynch says 92% of the global emerging market fund managers it surveyed were overweight the country in September, twice as many as in August.

Igors Lahtadirs, senior equity analyst at Citadele Asset Management, says the increasingly attractive dividend yield is one of the most important features of the Russian equity market.

“In Russia, investors like it when companies return money to shareholders due to still questionable corporate governance practice and not very high transparency levels, especially with respect to the state-owned enterprises.”

But dividends are only part of the picture. The past two years have seen a raft of wide-reaching capital market reforms.

Russia has merged two key stock exchanges, the MICEX and the RTS; created a central securities depositary; moved to a Target2 -Securities settlement cycle; and made it possible to clear Russian government bonds with Luxembourg-based Euroclear Bank.

This final measure is planned for next year (see box) and should also improve liquidity – a major factor in holding back emerging market investment.

Vladimir Tsuprov, chief investment officer at TKB BNP Paribas Investment Partners, says the current discounts of local stock prices to depositary receipts could disappear once local stocks also become available in Euroclear system.

GAME-CHANGER

The dividend policy – which means state-controlled companies will have to pay out 25% of profits this year, based on International Financial Reporting Standards – could be a game-changer for Russia.

Even though Russia has privatised assets over the years, state-ownership of large caps in the oil and gas, electricity, and partly the financial sector, is significant.

Gazprom, the largest natural gas producer in the world, Transneft, which is responsible for the national oil pipelines, Sberbank Rossii, the largest bank in Russia and Eastern Europe, and oil producer Rosneft are all state-controlled and would be affected (see table 2).

There is increased political pressure on state-controlled companies to share their net income streams with the federal budget through higher dividend payout ratios, says Lahtadirs.

“Should that trend continue, we will see not only enhanced cash returns to minority shareholders, but also improvement in corporate governance practices, as the state companies will

be forced to cut excessively large, inefficient and sometimes hard-to-justify capital expenditure programmes.”

Aivaras Abromavicius, partner at East Capital, notes that some companies are also debating when these dividend policies are applicable to them, whether there is room for exceptions and, if so, what the conditions are.

“Certain Russian companies are so large, their revenues are larger than those of some European countries,” he says. “They are, therefore, very influential and often get into a debate with government about various policies that affect them.”

No doubt, some will try to resist these dividend policies, insisting they need cash for other purposes. Abromavicius argues there is plenty of money left in companies, including the possibility to borrow.

Attitudes towards dividends have already changed in the private sector where companies are increasingly paying out dividends, which Abromavicius says was practically unheard of five to six years ago.

Payout ratios have improved because investors have become more demanding with regards to sharing cash flows with minority investors but also due to lower borrowing costs.

Pioneer Investments has been pursuing the dividend theme since last year and recently further increased its position in Gazprom by 50 basis points in its Emerging Europe and Mediterranean Equity fund.

Although this does not appear to be much, Marcin Fiejka, senor emerging markets equity portfolio manager at Pioneer, says Gazprom is already a large part of the portfolio. It is the fourth largest holding in the Russian Equity fund and the second largest in its Emerging Europe and Mediterranean Equity fund.

Other recent purchases of his team are Transneft, which he says has risen on the back of dividend expectations and the prospects of privatisation, and Surgutneftegas, an oil company, which he says it sitting on a lot of cash and will come under pressure to either pay it out in the form of dividends or invest.

Not everyone is convinced, though. Joseph Dayan, head of markets at BCS Financial Group, says holding Gazprom is not really justifiable, even though it has underperformed for so many years.

“Gazprom is not a for-profit run entity, it is more like the arm of the government,” Dayan says, adding that a lot of politics are involved.

“We do not like Gazprom as a long-term investment,” he says. “It will continue to be stripped of cash flow in order to finance expenditures for political reasons.”

Dayan says a lot of investors are buying Gazprom, hoping it will pay 35% dividends, which is overly optimistic.

RUSSIA’S CHANGING CASE

Marcin Fiejka, senior emerging markets equity portfolio manager at Pioneer Investments, says it used to be easy for the Russian government to ignore criticism because it had enough revenues from oil and gas.

This attitude started to change after the financial crisis, when demand for Russia’s resources plummeted.

“Now the Russian government is realising that its economic model is not sustainable in the long run and looking for different structures,” he says. “We have waited long for these changes.”

Even without the promise of higher dividends, Tsuprov says the investment case for Russia has changed.

Weaker performance of other emerging markets is making Russian equities look more attractive.

Towards the end of August and the beginning of September, emerging markets were sold off. Countries with weak external balances – Brazil, Indonesia, India, Turkey and South Africa – were particularly affected.

“There are still imbalances, but on the external side Russia is strong,” says Dayan. Russia holds more than $500 billion (€365.8 billion) of foreign exchange reserves and $150 billion in reserves from oil and gas sales, which are kept for difficult times.

Russia currently runs an estimated budget deficit of 0.5% of GDP, which is unusual. On the monetary side, interest rates are high at 8.25% and inflation hovers around 6%. Its central bank could actually cut rates, as opposed to other emerging markets, where interest rates are already low.

“Fed movements have had an adverse effect on emerging markets so investors want to be in a market that can defend itself,” Dayan adds.

Russia’s fortunes have long relied on the movements of oil and gas prices, which together account for up to 55% of the country’s budget. Dayan says there are other emerging markets as dependent on single factors, though.

PRUDENT FISCAL POLICY

Unlike in other countries, Russian fiscal and monetary policy has largely been well advised.

“Investors who have a bearish view on oil and gas should not invest in Russia,” Dayan says, noting that Russia should be able to defend itself even if the oil price drops to $70 per barrel from $110.9 per barrel in October.

“Investors who have a bearish view on oil and gas should not invest in Russia,” Dayan says, noting that Russia should be able to defend itself even if the oil price drops to $70 per barrel from $110.9 per barrel in October.

Then there are investors that deliberately play the global recovery through Russia, the idea being that if economic activity picks up, especially in China, commodity prices will rise and Russia will benefit.

Lahtadirs says the local market benefited from the recent spike in the oil price on the back of rising geopolitical tensions.

While Russia’s economy and equity market continue to be highly dependent on the oil price, he says the market’s reaction to oil price movements has become more muted recently.

Citadele Asset Management has accumulated shares of Rosneft because of supportive oil prices and high operating leverage of the companies, as well as expectations of improvements in corporate governance, which Lahtadirs says have partially materialised.

Over the last years, the oil price has overall stayed on a “rather comfortable level”, which he says has allowed oil producers to sustain decent cash flows and ensure macroeconomic and, to a certain degree, political stability in the country.

Lahtadirs says this has also created spill-over effects to internal consumption.

BCS Financial Group recommends buying Moscow-listed stocks of Russia’s largest retailer Magnit, which Dayan says owes its success to a dedicated owner. Magnit has a dual listing in Moscow and London, but Dayan says the London listing is up to 25% more expensive.

Magnit has been a darling of emerging market fund managers, but Fiejka says the stock is trading at valuations that do not discount risks. Still, he says his team likes companies where interests of the management are aligned with those of shareholders.

Magnit has been a darling of emerging market fund managers, but Fiejka says the stock is trading at valuations that do not discount risks. Still, he says his team likes companies where interests of the management are aligned with those of shareholders.

Citadele Asset Management has slightly rotated within the consumer staples sector of the portfolio and reduced the position in the supermarket chain O’Key Group, reacting to the deterioration of its business outlook. At the same time, it added to food retailer Dixy, on the expectations that operating performance will improve.

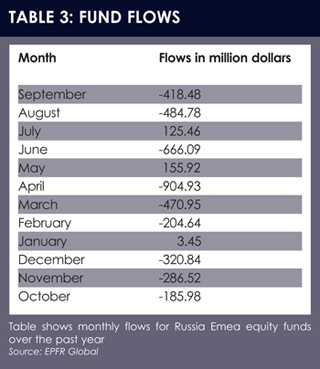

But many investors still appear difficult to win over. As an indication, EPFR Global data show outflows of $418.5 million from its Russian Emea Equity category in September, though this was down from outflows of $484.8 million in the previous month (see table 3).

Investors and fund managers make no secret of the fact that political risk, corruption and corporate governance are still the largest concerns.

“Corruption and corporate governance are issues [in Russia],” Dayan admits. “It is the same in other emerging markets, whether China or elsewhere.”

Acknowledging that there are inefficiencies in the government’s policies that negatively impact companies, Tsuprov says it is much more complicated than to simply label Russian equities as risky.

©2013 funds europe