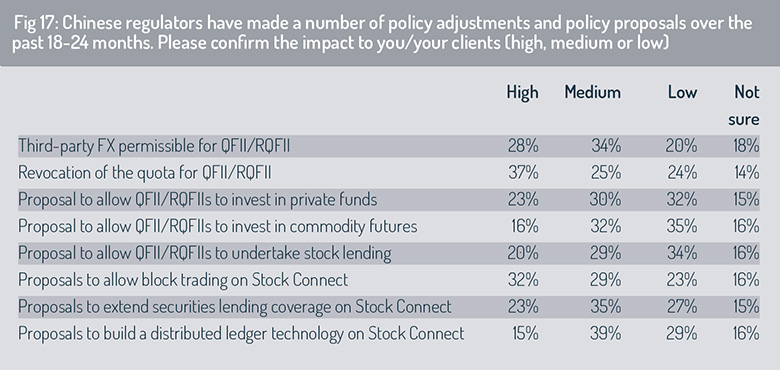

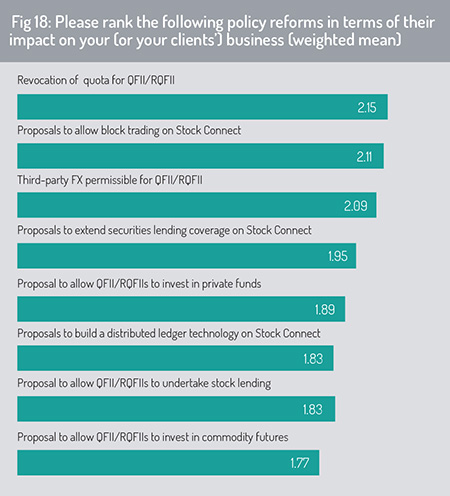

With Chinese regulators advancing a wide array of policy proposals designed to enhance market access and improve market efficiency, the survey asked respondents to prioritise which of these reforms will have the greatest impact on their business. Survey participants were asked to score each policy proposal as a high, medium or low priority (fig 17). These were then ranked in order on the basis of a weighted-mean score (fig 18). From this agenda, respondents attached highest priority to the revocation of quota restrictions for QFII/RQFII (known as QFI after November 1, 2020) and then to the extension of block trading facilities on Stock Connect.

As we have noted, investors continue to pay significant attention to the improvement of FX hedging tools, including proposals to allow third-party FX hedging in the QFII/RQFII programmes.

Although securities lending and borrowing is allowed under Stock Connect, this has, to date, been limited to brokers (‘exchange participants’). Extension of this programme to institutional investors, asset managers and custodians (lending on behalf of asset owner clients), enhancing loan supply by providing access to the deeper pool of securities that these hold in inventory, would potentially increase lending activity and the potential benefit (through enhanced liquidity, settlement fails coverage) this can offer to the market.

Alongside this package of reforms, PBoC, the CSRC and SAFE jointly issued a consultation paper on September 2, 2020 relating to potential changes to China’s fixed income markets. The Consultation Paper proposes a mechanism whereby qualified investors can trade cash bonds (as well as other bonds, subject to final regulations to be published by the regulators) in both the exchange bond market and the interbank bond market, through the connected infrastructure existing for these two markets, without any additional approvals.

The Consultation Paper also includes proposals to: (i) process the filing at asset manager level and eliminate the need to file for approval for each product; (ii) introduce a multi-tier custody structure with a nominee concept to align with international practice.

The Consultation Paper also includes proposals to: (i) process the filing at asset manager level and eliminate the need to file for approval for each product; (ii) introduce a multi-tier custody structure with a nominee concept to align with international practice.

With the introduction of multi-tier custody structure, CIBM Direct investors can choose to appoint a local custodian to enter the market or they can employ a global custodian (and therefore enter the market via a local custodian with accounts opened in the global custodian’s name). This reform also provides fungibility of fixed income assets across foreign investors’ QFII, RQFII (QFI after November 1, 2020) and CIBM Direct accounts.

Effective from September 1, 2020, CFETS also extended the opportunity for bond investors in CIBM Direct to trade across multiple counterparties via a request-for-quote (RFQ) mechanism based on quotes provided by market makers in the CFETS system. The CIBM Direct Trading Service is provided by CFETS in collaboration with Bloomberg and TradeWeb.

Conclusion

This 2020 China Investor survey indicates that China is central to the strategic priorities of international investors. Although investors are monitoring the implications of continuing US-China trade tensions and the new national security law in Hong Kong, respondents indicate that these risks do not substantially weaken the secular case for cross-border investment into China.

Index inclusion and the easing of regulatory barriers have driven a surge of investment through Stock Connect and Bond Connect. Notwithstanding the impact of the global pandemic on cross-border investment, Bond Connect and Stock Connect Northbound average daily turnover reached record half-yearly highs of RMB19.9 billion (US$3.0 billion) and RMB74.3 billion (US$11.1 billion) respectively in 1H 2020. The Bond Connect average daily turnover was triple that of 1H 2019.

Moreover, driven by market liberalisation and solid yield opportunities, China’s equities and bond markets have become the second-largest worldwide. Foreign holdings of China onshore financial assets increased to RMB7.18 trillion (approximately US$1.07 trillion) at the end of Q2 2020, according to PBoC data1.

Taking a closer look at the bond market, global investors have been adding to their holdings of Chinese government bonds (CGBs) since the early months of the pandemic, purchasing more than RMB850 billion during April alone, a rise of about 170% year-on-year (Xu Liangdui, ‘To promote cross-border use of RMB bonds in the post-Covid-19 market’, China Central Depositary & Clearing Co, CCDC, unpublished). This is likely to receive a further boost following the recent announcement from FTSE Russell that it will include Chinese government bonds in its World Global Bond Index from October 2021 (subject to final affirmation in March 2021). Standard Chartered Global Research estimates potential passive inflows of US$140 billion to US$170 billion on full inclusion and expects this to lead to a rise in foreign ownership of CGBs from 8.5% currently to 20% by end-2022.

Taking a closer look at the bond market, global investors have been adding to their holdings of Chinese government bonds (CGBs) since the early months of the pandemic, purchasing more than RMB850 billion during April alone, a rise of about 170% year-on-year (Xu Liangdui, ‘To promote cross-border use of RMB bonds in the post-Covid-19 market’, China Central Depositary & Clearing Co, CCDC, unpublished). This is likely to receive a further boost following the recent announcement from FTSE Russell that it will include Chinese government bonds in its World Global Bond Index from October 2021 (subject to final affirmation in March 2021). Standard Chartered Global Research estimates potential passive inflows of US$140 billion to US$170 billion on full inclusion and expects this to lead to a rise in foreign ownership of CGBs from 8.5% currently to 20% by end-2022.

Against a backdrop of depressed government bond yields in Western markets, CCDC proposes that with “ever-improving liquidity, operational efficiency and market infrastructure, conditions are ripe for promoting use of RMB bonds as a new safe asset”.

While the Connects have attracted strong growth in transaction volume, the inability of any single channel to meet the entirety of foreign investors’ access requirements – including asset class coverage, FX hedging, speed of registration and account opening, and low transaction costs – dictates that many will continue to employ a multi-channel approach.

Stock Connect and Bond Connect will remain at the forefront, providing ease of access and lower aggregate transaction cost than available previously through QFI. But there can be advantages for investors in trading directly through QFI (or CIBM Direct for bond investments) to access a wider universe of securities and a wide range of risk management tools.

In turn, the survey also reveals significant investor interest in private markets, although there remains a high level of caveat emptor attached to investment in less liquid securities, given challenges around the transparency of financial reporting and difficulties in obtaining rating opinions on smaller issuers.

In turn, as the world’s fifth-largest collective investment fund market, China offers a fertile sales ground for foreign asset managers wishing to exploit distribution opportunities in the domestic market. The survey forecasts strong growth in actively managed funds during the next 24 months, driven in part by retail investors wishing to reallocate from money market funds into higher-yielding fund products. For large asset managers committed to building a local presence in China for the longer term, a WFOE may provide an attractive option. For those with active joint ventures already in place with Chinese partners, there is a relatively even balance between those who will (or already have) taken a majority shareholding in their JV and those who do not expect to change their existing JV arrangements.

Testament to the advances made through this reform programme, investors’ longstanding concerns around speed of account opening and funding availability have slipped down their priority list in this year’s survey – albeit recognising that investors’ risk radars are currently dominated by the global pandemic, the US-China relationship and domestic political developments in Greater China.

Testament to the advances made through this reform programme, investors’ longstanding concerns around speed of account opening and funding availability have slipped down their priority list in this year’s survey – albeit recognising that investors’ risk radars are currently dominated by the global pandemic, the US-China relationship and domestic political developments in Greater China.

The need for a comprehensive solution to address FX risk across access channels remains important. It is encouraging that policymakers are taking initial steps to extend the FX hedging tools available and provide more FX flexibilities to foreign investors.

More broadly, China remains substantially under-represented in the investor portfolios of many global investors relative to its economic size (as the world’s second-largest economy in GDP terms), global strategic importance and contribution to key growth sectors such as technology.

This indicates strong potential for growth of cross-border investment into China as reform of access channels, operational infrastructure and financial reporting standards creates a market environment in which FIIs are confident to operate.

With a relatively promising economic outlook (the PBoC Governor recently indicated that the Chinese economy is likely to achieve positive growth for the full year of 2020), attractive bond yields relative to other large global economies and increasing investment opportunities arising from further regulatory liberalisation and global index inclusion, investment flows into China are expected to continue to accelerate over the coming 12 months.

China is rapidly establishing itself as a market that no investor can afford to ignore.

1– PBoC, Domestic Financial Assets Held by Overseas Entities, 2020, https://www.pbc.gov.cn/diaochatongjisi/resource/cms/2020/07/2020073116484988976.htm

© 2020 funds europe