Liquid alternatives are in vogue at the moment but at the same time their performance has been questioned. David Stevenson investigates the burgeoning asset class that allows retail investors access to hedge fund strategies, previously out of their reach.

Liquid alternatives can give retail investors a sense of living the high life. The concept allows them to invest in strategies previously inaccessible to funds regulated by the Ucits rules – including hedge fund strategies, such as equity long-short, or momentum trading through managed futures.

It can also provide retail investors access to multiple managers through fund-of-hedge-funds structures.

At the same time as providing regulated, alternative investments, there’s also a need for liquid alternatives to insulate investors from market volatility. The days when a balanced fund with a 60/40 split between equities and bonds would be seen as a diversifying strategy are over as normal correlation across asset classes collapses.

The appeal of liquid alternatives has not been lost on players such as Aberdeen Asset Management, JP Morgan Asset Management (JPMAM) and Schroders, to name but a few. Each has launched products in this asset class recently.

The appeal of liquid alternatives has not been lost on players such as Aberdeen Asset Management, JP Morgan Asset Management (JPMAM) and Schroders, to name but a few. Each has launched products in this asset class recently.

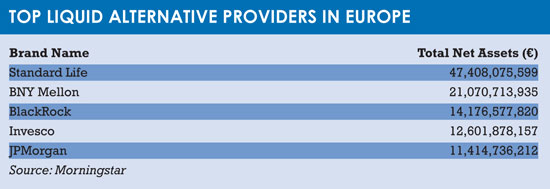

Morningstar only started categorising liquid alternatives as a separate asset class earlier this year; Lipper groups the products together with multi-asset.

More than two years ago, Goldman Sachs Asset Management (GSAM) was one of the first big houses to embrace liquid alternatives.

Marie Cardoen, head of alternative investments sales in Europe, the Middle East and Asia ex-Japan at the firm, says that although liquid alternatives had been available outside the US since 2005, it was the financial crisis of 2008 that brought about an acceleration of flows into the asset class, especially over the past three years.

According to Cardoen, in 2014 there was around $280 billion (€250 billion) in assets within Ucits liquid alternatives. Today that has exceeded $400 billion.

“Liquid alternatives is the only broad asset class that has attracted net positive flows so far this year,” she says.

JPMAM launched its liquid alternative product, which invests in underlying hedge funds, in January and now has €160 million in assets. The fund has returned 2.68% and, like many liquid alternative funds, is benchmarked against cash.

Natasha Petiton, vice president of product strategy at JPMAM, explains the business case and rationale behind her firm’s Multi-Manager Alternatives fund.

“The fund is within the Multi-Strategy category which has seen the most significant new flows [year-to-date] 2016. This Morningstar category has seen larger flows than any other category in Europe, driven largely by clients’ need to diversify their portfolios amid increased market volatility,” she says.

The fund targets a return of 5%-6% over the cash return with target volatility of 4-6% and low beta to the equity and fixed income markets.

One of the reasons liquid alternative funds are benchmarked against cash is due to the goals of portfolio diversification and lower correlation when compared with traditional equity and fixed income portfolios.

However, liquid alternatives have faced criticism for underperformance at a time when there have been double-digit returns in the high yield and equity markets.

Aberdeen’s Alternative Strategies Fund is benchmarked against both the Barcap Global Aggregate Bond Index and the MSCI World Total Return Index, which have returned 9.75% and 5.41%, respectively, compared to the Aberdeen fund, which is down 3.25%.

“The liquidity-fuelled market environment [with quantitative easing supporting bond and equity prices] means liquid alternative funds have generally not done so well against bond and equity indices,” says a spokesperson for Aberdeen.

But as Petiton says, even if liquid alternatives are not performing well compared to traditional asset classes, they are outperforming hedge funds generally – and as these products are available under Ucits, it gives retail investors an opportunity to invest in strategies previously inaccessible to them.

WIDENING THE APPEAL

Hedge funds are considered the devil in disguise in some European countries, leading to reputational concerns among institutional investors, so strategies offered within the Ucits ‘brand’ should offer some comfort.

Schroders GAIA [Global Alternatives Investor Access] range of funds also allows retail investors access to strategies that solely benefited the ultra-wealthy for years. The firm picks the top hedge fund managers and puts their strategies into a Ucits-compliant form.

One example is the GAIA Paulson Merger Arbitrage Fund, managed by hedge fund manager John Paulson. It is essentially a simple strategy – when a deal is announced, a manager will go long on the target and short the acquirer. Returns are generated on the completion of the deal. Under Ucits, the risk of this strategy is reduced if the deal goes wrong, as rules limit the amount that can be invested into the target at 10%.

Andrew Dreaneen, head of GAIA business development and product at Schroders, explains the appeal of strategies like this being offered through the Ucits regulated liquid alternatives channel.

“These strategies offer a toe in the water for many long-only investors seeking to diversify away from long-only equities, long-only fixed income and more long-only balanced funds,” he says.

The demand for these strategies is reflected in the numbers. The firm recently partnered with Two Sigma, a financial technology company with assets of $37 billion, to launch a combined equity market neutral and global macro trading strategy. Schroders raised $250 million in the first couple of weeks, which Dreaneen says highlights “the pent-up demand for differentiated liquid alternative investment products”.

For GSAM’s Cardoen, only funds that can go long-short are considered liquid alternatives. This means that real estate, despite being an alternative asset class by most people’s standards, does not strictly fall within the firm’s liquid alternatives range, given its long-only nature.

Cardoen is far from alone in her view of what constitutes a liquid alternative strategy. Pioneer Investments has a long history in providing funds that can be considered as liquid alternative strategies. Its Absolute Return Multi Strategy fund is one example.

Davide Cataldo, head of multi-strategy portfolios at Pioneer, says market conditions mean investors should consider new sources of return that offer adequate diversification, going beyond traditional and directional asset allocation. He adds that these strategies should also be able to offset potential drawdown risks and high market volatility with a view to generating “genuine alpha”.

State Street is another asset manger with an interest in liquid alternatives. Maria Cantillon, global head of alternative asset manager solutions, says industry reports have predicted the amount of assets in global liquid alternative funds to reach $1.7 trillion by 2019.

“There are several factors driving this investor appetite – none of which we see abating over the next 18 months,” she says, citing the search for yield, negative correlation and stable return streams as examples.

STANDING OUT FROM THE CROWD

With most major fund houses offering liquid alternative funds, you could forgive investors for being bewildered by the sheer choice on offer.

But a guide when making a decision is to ask what exactly the fund in for. Some investors use these funds as alternatives to holding fixed income, particularly with the current low-rate environment. Others may use them as an extension to their existing equity and fixed income strategies, perhaps to de-risk their portfolios.

Maybe investors are looking for lower costs – or just for greater liquidity with their exposures to alternatives, such as hedge fund strategies that were previously only accessible to institutional investors.

Liquid alternatives have made an impact on the fund industry – the large growth in its assets illustrate that investors are certainly interested. European investors are faced with the Alternative Investment Fund Managers Directive that hinders investment in offshore hedge fund domiciles such as the Cayman Islands. The European Union’s Solvency II directive, which came into force at the start of the year, requires stricter investment controls and high risk-weighted capital charges for insurers’ allocations to illiquid investments, such as traditional alternatives.

In the face of this regulatory framework, the draw of investing in liquid alternatives seems obvious – even if there are some question marks over the performance of the asset class.

©2016 funds europe