And more change. A small reduction in market share among larger asset managers is partly explained by the rise of alternative asset classes, finds Alan Chalmers.

Two key industry reports on the health of the asset management industry have been published in recent months.

First, a study by consultancy Willis Towers Watson looked at the change in assets under management (AuM) between 2017 and 2018, with historical data going back further. The report for the Thinking Ahead Institute on the world’s 500 largest fund managers noted a 3% reduction in AuM in 2018 compared to the previous year.

Complementing this is PwC’s ‘Asset Management 2025 – Looking ahead for the industry’, which examines trends in the US mutual funds sector in particular.

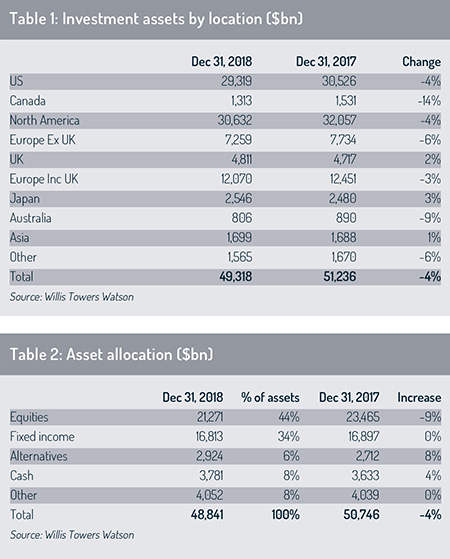

The 3% reduction in AuM noted by Willis Towers Watson masks a complicated story tied to markets, currencies and the wider business environment. Looking purely at the top 50 players, AuM fell by 5% from $62,073 billion to $58,778 billion between 2017 and 2018.

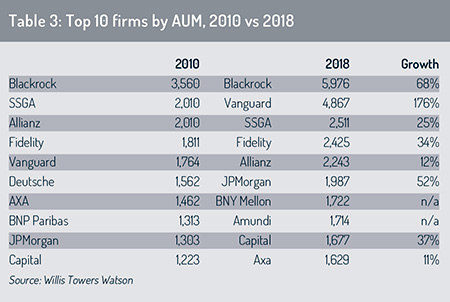

The top seven players did not change position. However, the French asset manager Amundi reached number eight for the first time. It was tenth in 2017 and one of the few top 50 asset managers to grow in 2018. Others in that category include Goldman Sachs Asset Management, Sumitomo, Power Financial, New York Life, Blackstone and Federated Investors.

The top seven players did not change position. However, the French asset manager Amundi reached number eight for the first time. It was tenth in 2017 and one of the few top 50 asset managers to grow in 2018. Others in that category include Goldman Sachs Asset Management, Sumitomo, Power Financial, New York Life, Blackstone and Federated Investors.

In the case of Power Financial, this was previously recorded as Great West Life and may now include more Power Financial firms – for example, Mackenzie Investments. The top three companies remain BlackRock, Vanguard and State Street Global Advisors, all of which have major passive strategies.

Noticeable fallers include France’s BNP Paribas Asset Management, with AuM down 18%. Its ranking dropped from 13th to 16th. Mitsubishi saw AuM fall 16%; Franklin Templeton, 14%; and Standard Life Aberdeen, 18%.

Markets and currencies

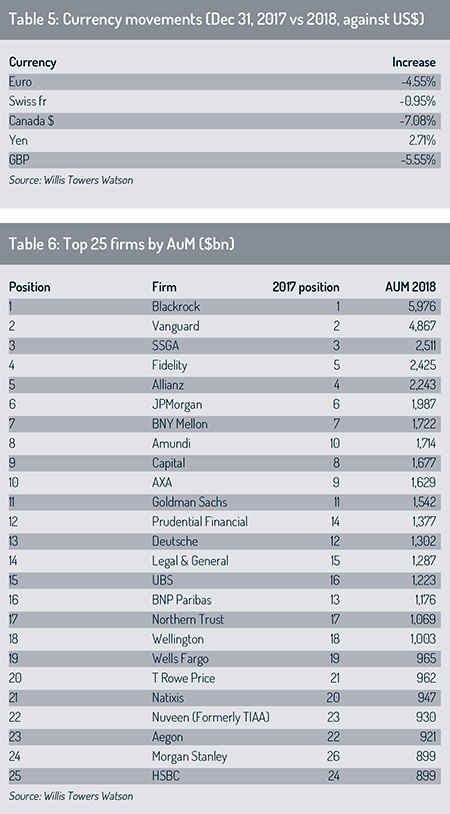

All AuM figures in the Willis Towers Watson report are denominated in US dollars. This had a major impact on the figures, with an average currency depreciation of 6 % against the euro, sterling and the Canadian dollar.

In addition, market movements had a large impact on AuM, with country of domicile a key factor. Both the Nikkei and FTSE stock market indices fell by about 12% between 2017 and 2018. The DAX recorded an 18% fall. These compare with a decrease in the US of less than 6%.

That said, markets at around mid-November 2019 had recovered somewhat. The DAX was up 22%; the Nikkei and Dow Jones nearly 15%; and the UK – where Brexit is the main, ongoing story – just under 8%.

Looking at market share, between 2011 and 2017, the 20 largest asset managers saw their share increase from 38.7% to 43.0%. But 2018 saw the first fall back, with their combined market share dropping slightly to 42.2%. This may have reflected falling equity markets, or perhaps the greater emphasis by investors on alternative products and gains by specialist managers in fields such as private debt (see box).

Looking at market share, between 2011 and 2017, the 20 largest asset managers saw their share increase from 38.7% to 43.0%. But 2018 saw the first fall back, with their combined market share dropping slightly to 42.2%. This may have reflected falling equity markets, or perhaps the greater emphasis by investors on alternative products and gains by specialist managers in fields such as private debt (see box).

The next strata of managers, ranked 21 to 50, also saw their market share fall a little, from 22.8% of total AuM to 22.0%.

Of the top 20 asset managers, 13 are US managers and account for 72.6% of the top 20’s AuM (T Rowe Price was a new joiner in 2018). The remaining seven are European. The asset managers are evenly split between independents and those owned by banks or insurers.

Fund flows

Interestingly, 2018 was the first year in which passive investments declined, registering a fall of 3.4%.

At the asset class level, there was a 9% fall in equity allocations between 2017 and 2018. Fixed income remained steady. Part of this was related to market values, but the movement – or lack of movement in the case of bonds – was also backed up by fund flow data. The flow data also revealed an 8% increase in allocations to alternative investments.

One noticeable trend in the 2018 survey is the increased interest in sustainable investment. The whole area of environmental, social and governance (ESG) investment is most definitely on the rise, particularly in Europe, though it is also gaining strong momentum in the US and Asia.

It is even a growing area in China – and with the approval of the government. According to the report, the number of ESG mandates grew by 23.3% in 2018. Looking at manager insights, 34% expected a significant increase in sustainable investing, with 49% expecting a moderate increase.

The asset management industry in China has seen continued growth more broadly. This is reflected in one firm particularly, with CCB Principal coming in at number 84 with $236 billion of AuM. It was 181st in 2017, with $72 billion of AuM. The rise makes it the leading China player by AuM, ahead of CITIC at 95 in the rankings (with $195 billion of AuM). Then comes E Fund (104th with $177 billion), Harvest (106th with $164 billion) and China Asset Management (113th with $146 billion).

All of which raises the question, when will we see a Chinese manager in the top 50?

The opening up of the Chinese market may also lead to more competition from Western firms as 100% ownership is permitted.

Industry growth

The survey also comments on the outlook for the asset management industry. Disruption in the years to come is highly anticipated, with fee compression and greater pressure on margins. The high cost of technology and ongoing regulatory activity need to be considered too.

A fifth of the survey respondents expected a significant increase in resources deployed into technology and big data, while 61% expected a moderate increase. In terms of regulation, 17% expected a significant increase and 40% a moderate increase.

In the past eight years, the asset management industry has seen a number of significant changes. Although BlackRock remained at the top of the rankings by AuM, it has several rivals when it comes to its rate of growth.

BlackRock has been in pole position since 2009, growing 68% between 2010 and 2018. In the same period, however, Vanguard has seen a 176% increase and moved from fifth position to second.

Another leader is Amundi, which was not in the top ten eight years ago but has grown by 88% in this period. Meanwhile, Deutsche Asset Management/DWS and BNP Paribas AM have dropped out of the top ten, to be replaced by Amundi and BNY Mellon.

Another leader is Amundi, which was not in the top ten eight years ago but has grown by 88% in this period. Meanwhile, Deutsche Asset Management/DWS and BNP Paribas AM have dropped out of the top ten, to be replaced by Amundi and BNY Mellon.

The period in question has been quieter in terms of consolidation. Federated Investors acquired Hermes Investment Management in the UK, but the anticipated consolidation onslaught has not materialised. Many companies are still digesting previous acquisitions, such as Amundi and Pioneer Investments, Standard Life and Aberdeen Asset Management, and Invesco and Oppenheimer. The lack of activity may reflect markets’ less certain state in recent months, as well as the difficulty of integrating large asset management businesses.

Growth areas for some of the larger asset managers have tended to be through acquisitions of specialist players in the private markets sector, mainly private equity, real estate and private credit. These tend to be much smaller firms and are more likely be manager-owned – but larger players sense that they will need these skill sets (see box, right).

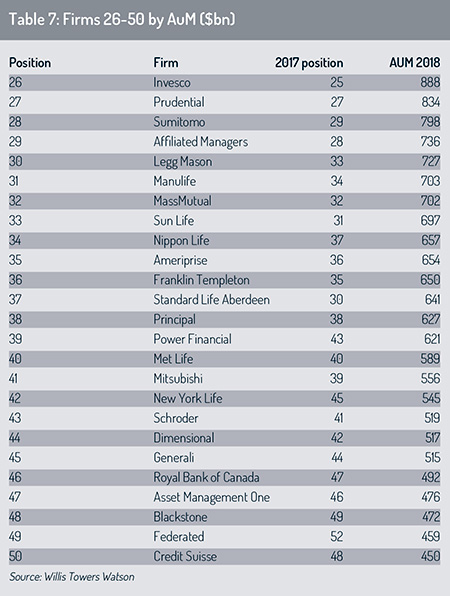

To highlight the degree of consolidation in the industry, 242 companies in the 2008 survey were absent from the 2018 survey. This reflected a near-50% consolidation rate in ten years.

The survey notes that there is a greater appreciation of culture within investment companies, but that this understanding of the role of culture may be a negative factor in future consolidation.

Challenges and outlook

PwC’s report into the US industry highlights the challenges faced by asset managers. A variety of outcomes by 2025 are predicted, including a lower rate of industry growth. On average, this could be 5.6% a year between 2018 and 2025, compared to 8.7% between 2011 and 2018.

The dominance of passive in the US is expected to grow from 36% in 2018 to 50% by 2025, with a corresponding reduction in expense ratios across both active and passive investment of 22%. Development of the passive market has been slower in other parts of the world.

In terms of the size of the US industry, PwC expects a 14% reduction in the number of mutual funds and ETFs between 2018 and 2025. In addition, the mega-managers are expected to account for 64% of the funds industry by 2025, compared to 55% at the end of 2018.

The industry is expected to undergo further consolidation up to 2025. As a result, 20% of firms in existence today are likely to be acquired or cease to exist. That would mean a further 100 firms drop out of the top 500, adding to the 242 that have disappeared since 2008 to be replaced by more specialist players, new competitors and regional players such as China.

The industry is expected to undergo further consolidation up to 2025. As a result, 20% of firms in existence today are likely to be acquired or cease to exist. That would mean a further 100 firms drop out of the top 500, adding to the 242 that have disappeared since 2008 to be replaced by more specialist players, new competitors and regional players such as China.

The expectation is that product lines will be rationalised as managers seek to reduce costs, and there will be more outsourcing in areas such as legal and compliance, fund accounting, data management, custody and IT services.

While this all applies to the US, parallels are likely to be drawn for similarly mature markets such as Europe. However, for emerging markets – especially India and China, where savings rates are low – this may not apply. The application of passive investment models may also be inappropriate due to a lower level of investment research and analysis – at least until these markets mature.

One major area that will help managers reduce their costs is technology, perhaps by 2% to 4% annually. Many expect it will revolutionise distribution too, though that remains to be seen.

The challenge ahead is in the transformation of businesses to meet changing investor demands, whether for more ESG, wider products or distribution. PwC states “there are two key foundations for re-orientating your business: redefining your purpose and determining what capabilities you need”.

Since 2008, and following the global financial crisis, the atmosphere in the industry has been all about change. It appears that this will not change in the near term.

©2019 funds europe