Nicholas Pratt examines the effect that the Alternative Investment Fund Managers Directive is having on a custody bank’s use of sub-custodians. Plus, the challenge from new depositaries.

This year’s custody survey is the first to be carried out in the era of the Alternative Investment Fund Managers Directive (AIFMD) which has been implemented in some, but not all, EU member states. One of the liveliest issues from the directive – particularly for custodians – is the liability obligations of an alternative fund’s depositary – a role that has been typically provided by custodians in the traditional asset management space.

Under the directive, the depositary will be responsible for returning assets to alternative fund managers should a counterparty default, even if the assets are held with a sub-custodian. This has sparked expectations that custodians will review their sub-custody arrangements and either choose to bring sub-custody mandates back in-house, switch sub-custody mandates from regional banks to larger and more established global custodians, or move out of riskier markets altogether.

This year’s survey has introduced a new question which asks for the percentage of assets under custody that are held with a third party sub-custodian. While not all the custodians were prepared to disclose this information, the survey reveals a clear variation.

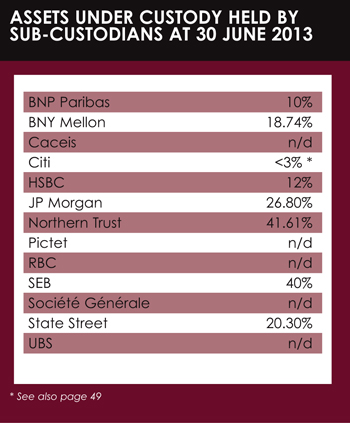

At one end are the investment bank-based custodians that offer a sub-custody service of their own. These include Citi (3%) and HSBC (10%), while at the other end are Northern Trust (41.61%), State Street (20.3%) and BNY Mellon (18.74%) that are more reliant on third party sub-custodians to provide their global coverage.

At one end are the investment bank-based custodians that offer a sub-custody service of their own. These include Citi (3%) and HSBC (10%), while at the other end are Northern Trust (41.61%), State Street (20.3%) and BNY Mellon (18.74%) that are more reliant on third party sub-custodians to provide their global coverage.

In between are the likes of Societe Generale Securities Services (SGSS)nd BNP Paribas Securities Services (10%) – two banks that have increased the number of countries they offer a direct custody service in as well as reducing the number of riskier markets in which they hold sub-custody agreements.

For example, in October 2012, BNP Paribas launched a direct custody service in the US (it previously used Brown Brothers Harriman as its sub-custodian) and, in July 2013, another France-based custodian, Caceis, launched depositary and custody services in Belgium and the Netherlands – moves which deputy chief executive Joe Caliba says will “play a key part in ensuring the highest level of security for those assets”.

Meanwhile, SGSS has added direct custody services in Central and Eastern Europe and withdrawn its sub-custody service in higher risk locations, including parts of sub-Saharan Africa. According to Etienne Deniau, global head of asset managers and asset owners at SGSS, these decisions are a result of greater due diligence on sub-custodians and central securities depositaries it uses around the globe.

“We have to know what happens in the event of a default and how easy it is to get assets returned.”

Arguments can be made either way in terms of the relative risk profile of custodians, both those with a large reliance on sub-custodians and those with a large sub-custody network of their own.

Paul North, head of product management, Europe at BNY Mellon, says that the bank has no plan to make fundamental changes to its sub-custody network other than strengthening its risk management and oversight.

“We see the diversification of our sub-custody selection as a mitigant of liability risk. We are not trying to become a local custodian in every market. I think that approach concentrates liability risk to an extent.”

SPLIT OF ASSETS

According to Dean Lumer, director of management consultant Knadel, the split of assets under custody between direct and sub-custody is one of the factors that fund managers are considering as part of their due diligence in custodian selection. It is not something that is influencing buyer behaviour as yet. However, Lumer does foresee it having an impact on pricing.

“The custodians are currently considering how they price the AIFMD risk into their custody rates. At present it is not clear whether firms with a larger external network will need to price in more risk.”

“The custodians are currently considering how they price the AIFMD risk into their custody rates. At present it is not clear whether firms with a larger external network will need to price in more risk.”

Clients are also taking greater interest in how their assets are held by their custodians, whether they are held on or off the balance sheet, how the assets are segregated and how easy it would be to identify those assets in the event of a loss.

This has led some clients to opt for a boutique custodian that will set up a special purpose vehicle for their assets in order to make the segregation process more identifiable. However, among the large asset managers that make up the majority of Knadel’s clients, Lumer does not anticipate that there will be major swings in either the managers’ choice of custodians or the custodians’ ratio of in-house versus third-party assets under custody.

There may, however, be more changes in their choice of sub-custodian and a move away from the regional banks to more internationally recognised banks, which could further complicate the arguments on the relative risk profiles of custodians if they are both involved in a sub-custody agreement.

NEW ENTRANTS

The AIFMD and its requirement for certain alternative managers in certain circumstances to appoint an independent depositary has opened the depositary market to new comers.

One of these is the specialist private equity fund administrator Ipes, which is now offering an independent depositary service to UK private equity firms that have sought AIFMD status from the Financial Conduct Authority (FCA).

Under the directive, UK private equity firms can use an FCA passport to market their funds throughout Europe on the condition that they appoint an independent depositary. Ipes has been appointed by two of the first three UK private equity firms to acquire AIFM status.

“It is a very competitive space with about 20 players, but there are some that are further along in their thinking,” says Ipes commercial director Justin Partington.

“Ipes is also quite narrowly focused in that we are looking only at private equity and infrastructure funds.”

The liability question may have focused more attention on the importance of a strong balance sheet, which is the biggest advantage for the global custodians and investment banks offering a depositary service.

However, as Partington says, making a private equity or real estate asset disappear is a far harder task than losing a custody asset.

Indos Financial was set up in October 2012 by Bill Prew to offer offshore hedge funds an independent AIFMD depositary oversight service and an alternative to what Prew sees as the conflicted model whereby existing depositary providers will, as a general rule, only offer a depositary service where an affiliate also provides fund administration.

Indos Financial was set up in October 2012 by Bill Prew to offer offshore hedge funds an independent AIFMD depositary oversight service and an alternative to what Prew sees as the conflicted model whereby existing depositary providers will, as a general rule, only offer a depositary service where an affiliate also provides fund administration.

As with Ipes, Indos has a very specific target market – the EU-based managers of non-EU funds which are marketed in the EU where private placement is allowed. Under article 36 of the AIFMD, these managers must ensure that one or more firms are appointed to perform safe keeping of assets, cashflow monitoring and oversight duties.

Unlike the article 21 single depositary model for EU funds, strict liability for loss of assets does not apply. Whereas the safe keeping of assets and the daily cash monitoring requirements are largely already provided by prime brokers and fund administrators respectively, the oversight function (where the depositary acts as a trustee and oversees fund valuations and investment guidelines compliance) is entirely new for offshore hedge funds.

NICHE SPECIALIST

Indos is likely to appeal to small to medium sized funds that will be attracted to the more attentive and flexible service a niche specialist can provide, says Prew.

“I appreciate that many managers would, in an ideal world, like a global custodian’s name on their prospectus but I expect many managers will find it hard to identify a brand name provider willing to act. The costs could also be high, in terms of minimum fees and having to fit into their standard models.”

©2013 funds europe