Outsourcing providers are ramping up their offerings but take-up among large managers is still rare. Nicholas Pratt asks if all the competition will be in vain.

A battle is brewing in real estate fund administration between three categories of providers. In one camp are long-term specialist administrators that have well-established practices based in the dominant offshore domiciles such as the Channel Islands and the Caribbean, as well as onshore centres like Luxembourg and the UK.

In another camp are the large asset-servicing firms that have made sizeable inroads into the alternative funds market and are looking to extend this to the real estate and private equity sectors. And a third group has emerged comprising large property fund managers that administer their own funds in-house and are looking to extend these services to other managers.

In July 2015, CBRE Global Investors, which manages more than $36 billion (€33 billion) of real estate assets, transferred 170 staff to a new unit called CBRE Global Investment Operations, which will offer fund administration, transfer agency, financial reporting, data management, regulatory support and other services to other real estate fund managers with multinational investment portfolios.

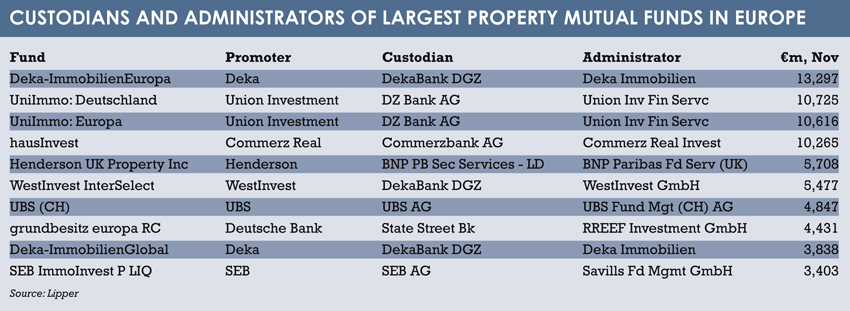

As fascinating as this competition may be, it is unclear if there is sufficient demand from real estate funds to match the providers’ ambitions. A look at the ten largest real estate funds domiciled in Europe (see page 48) shows that only one, Henderson UK Property, has appointed a third party as its administrator, in this case BNP Paribas Securities Services.

And according to one of the UK’s largest real estate fund managers, Legal & General Property (LGP), the property division of Legal & General Investment Management, third parties are still failing to convince. “We use our in-house fund accounting team to administer property investments held directly in the UK across the majority of our 19 real estate funds,” says Andy Banks, LGP’s finance director. Jersey-based administrators are employed for properties already held in Jersey property unit trusts or Jersey feeder funds for investors.

“Where we have outsourced, we have had mixed results,” he adds.

NOT UP TO SCRATCH

The main motivation for keeping administration and accounting in-house is the desire to have close control over data and the ability to interrogate information to check that net asset values (Nav) and unit pricing is accurate and reliable, says Banks. But there is also a belief that some of the third-party administrators are not up to standard.

“In some cases where we have outsourced, we have ended up bringing it all back in-house because we realised we could do a better job,” says Banks. “There are better lines of communication and it is easier to hire the right people.”

Banks recognises that a lot of outsourcing providers have been building up their real estate fund administration teams but there has been a mixed reaction from fund managers, not least because of the specialism required for pricing and Nav calculation of property funds. And while start-up funds may be more inclined towards outsourcing, larger, more established funds may still keep their administration in-house, for now at least.

Despite the scepticism of property fund managers, providers are buoyed by the idea that the real estate fund market is set to grow – a 2015 PwC report, ‘Real Estate 2020: Building the Future’, predicts that by 2020, investable real estate will have grown by 55% since 2012.

At the front of the push from asset servicing firms is BNY Mellon, which in February 2015 signed a deal with Deutsche Asset and Wealth Management to take on $46.3 billion of real estate and infrastructure assets and 70 staff. A year later, the Deutsche deal remains its sole mandate, although it has received numerous enquiries, says the global head of BNY Mellon’s private equity and real estate and fund services unit, Alan Flanagan.

In addition, says Flanagan, these types of lift-out outsourcing deals have a considerable lead time due to their size and complexity – the Deutsche deal took 18 months to complete – and are very different to liquidity-driven, open-ended mutual funds, requiring a different technology model to service them.

Flanagan is also confident that, despite the competition in the market, there will be enough business to go around. “There is only about 20%-30% of the market that has outsourced so far.” He cites the requirement under the Alternative Investment Fund Managers Directive (AIFMD) for a depositary licence as an advantage for asset servicers, who can then bid for the accounting and administration contract for those funds looking for a single service provider. “Some of the boutiques are struggling with this and I think we’ll see some consolidation with both the asset servicers and the property managers acquiring boutiques.”

This view is shared by Dirk Holz, director at RBC Investor & Treasury Services. “There is a huge amount of investment money allocated to real estate funds from institutional investors that only want to invest in AIFs [alternative investment funds] and they increasingly require similar portfolio overviews that they are used to getting for their Ucits funds. These investors need very detailed data and regular valuations to feed into their benchmarks and that is a big driver for outsourcing.”

BIGGER BALANCE SHEETS

BNP Paribas Securities Services is also targeting the real estate administration market, forming a private equity and real estate client segment in mid-2015. The division’s head, Philippe Tassin, believes a number of managers are looking for providers with bigger balance sheets and that the time has come for real estate funds to be brought into the same outsourcing model as other alternative funds. “If real estate fund managers are looking to enter new geographies or launch new funds, they are looking to consolidate their data, rationalise their costs and that will push them towards global outsourcing offerings.”

However, the specialist administrators are also acquiring depositary licences in anticipation of AIFMD-related mandates. Langham Hall acquired a depositary licence for London and Jersey prior to the AIFMD going live and in January 2016 acquired a third depositary licence for Luxembourg. “To have the depositary licence is vital for the AIFMD,” says Rob Short, founder and managing partner.

Short is less convinced by the asset servicers’ other claims. For one, he sees a slowdown in fundraising for 2016 and no huge number of property fund launches. And he does not imagine many managers folding their existing funds into the same outsourcing arrangements they have for other alternative funds. “To have a real estate fund administered by a hedge fund administrator is a recipe for disaster.”

Short’s view is shared by David Bailey, managing partner at specialist fund administrator Augentius, who cites the importance of expertise. “The asset servicing groups have traditionally done a lot of hedge fund administration work but they are not geared to the same level of complexity. I don’t think they train their staff to the same level of accountancy. And we’ve seen some significant withdrawals from the banks.”

Bailey also believes that it is no longer possible to be a property fund administrator in one domicile, given the number of funds employing multiple structures in multiple domiciles. This complexity, allied with a growing regulatory burden and the need for significant IT investment, has led a number of funds to reconsider administrating their own funds.

ONE-STOP SHOP

Another specialist fund administrator, Crestbridge, has not sought a depositary licence. “The large custodians have a first mover and scale advantage in providing depositary services,” says Miranda Lansdowne, director, fund services at Crestbridge. “And I’m not sure the one-stop-shop approach – where one firm provides administration and depositary services – is the most efficient option.”

Instead, Crestbridge is focused on providing management company services to the growing number of institutional investors looking to make direct investments in real estate assets and getting involved in collaborative investment ventures with property fund managers. These investors are looking to specialist service providers for a wider range of services beyond the normal accounting and valuation services such as risk management, management company services and other functions, says Landsdowne.

However ambitious the providers may be, the evidence suggests there will be no rush of outsourcing mandates in 2016 and the competition between them may turn to consolidation as property managers and asset servicers look to acquire specialist administrators, giving them both the multi-jurisdictional presence and skilled staff they are told they require.

LGP’s Banks would back such a move if it helped to raise the standard of outsourcers’ offerings. “I would like to see an improvement because there is definitely room for highly professional, well-trained specialist providers to support institutional real estate funds,” he says. “The industry is crying out for them.”

Until then, LGP, like many other large property fund managers, will retain many of its administrative functions in-house, says Banks. “Real estate fund management is a focused, value-add service and fund accounting is a necessary support service. We will continue to look at the economics of in-house fund accounting and whether there is a net benefit to outsourcing.”

©2016 funds europe