Digital transformation will play an important part in shaping the future direction and success of the asset management industry. For asset servicers, this is creating opportunities to help asset management clients to negotiate this journey, providing support around investment performance and risk analytics, regulatory reporting, data management, faster NAV generation and provision of contingent NAVs, along with a host of other areas.

In meeting this demand, asset servicers will continue to broaden their product portfolios and to extend their geographical coverage. The survey asked where asset servicing firms could deliver most value to asset management clients and the dominant answer – in terms of the respondents that selected this as their first priority and on the basis of a weighted-average ranking – was that asset servicers should be extending their coverage into new fund markets and jurisdictions (fig 5).

These results indicate that asset servicers also need to extend their support for new asset classes and product types, potentially including private markets, ETFs and digital assets. There has been a progressive rise in investment in alternative assets for some investors. This meets demand from investors for diversification within multi-asset strategies, as well as responding to a low interest rate environment, tight yields on fixed income securities and current caution around equities investment in light of geopolitical political uncertainties (e.g. Brexit, US-China trade tensions) and weak global economic data.

The survey also highlights demand to help asset managers and asset owners to unlock new insights through data analytics. Investment firms that have access to large, high-quality data sets and the skills to interrogate these effectively have opportunities to realise competitive advantage. There is a focus on the use of big data to generate investment outperformance through more effective structuring of investment strategies, along with use of customer segmentation analysis to tailor products for better fund marketing and distribution.

Respondents also highlighted the importance of being able to offer customised, flexible client reporting to asset management and asset owner clients. Many asset managers and asset owners have outsourced their reporting requirements to asset servicing companies. Some wish to retain flexibility to customise their reporting, potentially using APIs to access their investment data, maintained by the asset servicing provider, and to construct their own reports.

Respondents also highlighted the importance of being able to offer customised, flexible client reporting to asset management and asset owner clients. Many asset managers and asset owners have outsourced their reporting requirements to asset servicing companies. Some wish to retain flexibility to customise their reporting, potentially using APIs to access their investment data, maintained by the asset servicing provider, and to construct their own reports.

There is also demand for flexibility around the timing of reports. While some asset owners, asset managers or distribution partners (for example, a wealth manager or private bank), may be happy to receive periodic reporting, others are seeking ‘smart alerts’ triggered when there is a significant change in portfolio performance or asset allocation, for example.

But reporting is not only about customisation. A large asset owner that uses multiple asset managers may not wish to process reporting from each individual manager, requiring that it manages multiple APIs, multiple logins and a range of reporting formats. Rather, many asset owners are looking for consolidated reporting across their full multi-asset programme, employing an asset servicer or third-party reporting specialist to pull in data/reporting from these multiple sources and build a consolidated report with this information.

Managing vendor relationships

Managing vendor relationships

Although some asset management houses choose to meet most of their trading, settlement and asset servicing requirements through in-house provision, some fund managers have chosen to outsource parts of the investment lifecycle, which they deem to be ‘non-core’, to an external provider. This may involve a large-scale investment operations outsource contract, where a wide range of the asset manager’s activities outside of the money-management function are outsourced to a single provider. In other cases, the asset manager may adopt a ‘modular’ approach, appointing specialist providers to deliver specific requirements.

So too, asset servicing companies may outsource functions to third-party suppliers – for example, to supply and maintain a fund accounting platform, a payments system, a collateral management module or to provide cloud-based data management services.

A modular, multi-provider approach can add complexity, however, forcing the buyer to interface with multiple services providers and technology systems. With this in mind, some buyers are evaluating opportunities to consolidate their third-party relationships to simplify vendor management and to realise pricing benefits during contract negotiation.

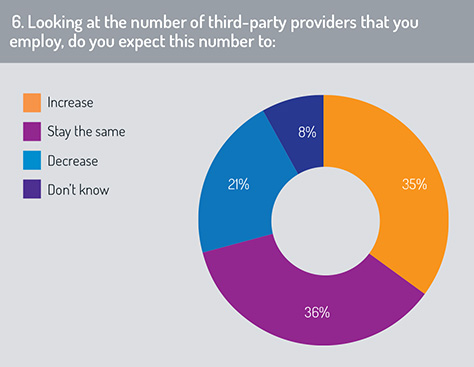

To gauge the direction in which the asset management industry is moving, we asked respondents whether the number of third-party providers they employ is likely to increase, decrease or stay the same in times ahead (fig 6).

To gauge the direction in which the asset management industry is moving, we asked respondents whether the number of third-party providers they employ is likely to increase, decrease or stay the same in times ahead (fig 6).

Thirty-five per cent of respondents told us that they will increase the number of third-party providers they employ. A slightly larger number, 36%, said they will remain with their current arrangements. This reflects the growing innovation taking place in the third-party supplier market and the desire of some buyers to broaden their appointments to take advantage of this expertise.

However, 21% told us that they aim to reduce their range of service providers, taking advantage of a simpler vendor management structure and the benefits of being able to source a range of service requirements from a single provider, often via a single technology platform.

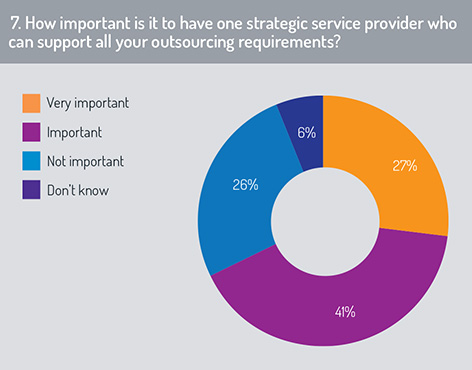

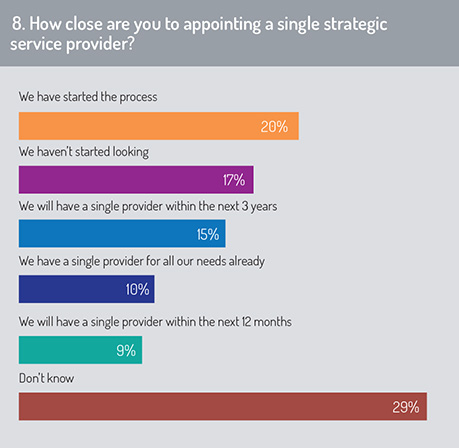

To assess this trend in more detail, we asked survey constituents how important it is to have a single strategic service provider (fig 7). The majority said that it is important to have a single consolidated third-party service provider. Moreover, survey results indicate that some respondent firms are already moving in this direction, with more than 30% saying that they have a single provider in place or will do so within three years (fig 8).

Insight and client empowerment a priority

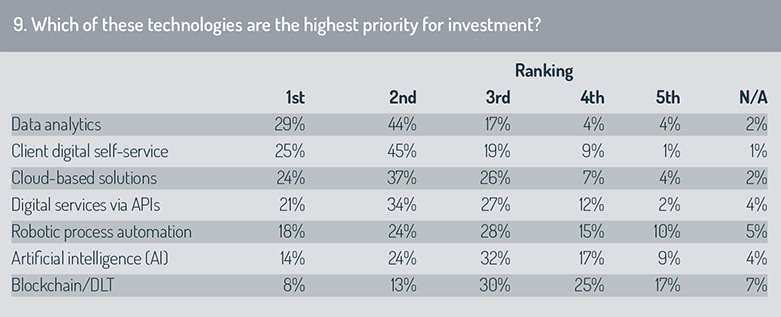

To gain further information about our respondents’ technology development strategies, we asked which technology segment or skills area is a priority currently for their technology investment (fig 9).

Data analytics was the dominant response: 29% of respondents selected this answer as their first choice and this also ranked as respondents’ highest priority on the basis of a weighted-average ranking.

Initiatives designed to extend client self-service capabilities through digital channels also ranked highly in this priority list. In the introduction to this report, we have highlighted the value that digital transformation may offer in delivering a better user experience, and in providing client interfaces that enable the user to pull out data and analytics customised to their own specialised requirements.

The survey also highlights the important role cloud-based solutions will play in shaping the future technology strategies of asset manager and asset servicing companies. Cloud computing typically refers to the use of a network of remote servers accessed via a Web interface to store and manage data and to deliver services to the user – for example via a software-as-a-service (SaaS) or platform-as-a-service (PaaS) type solution (see opposite page).

Interestingly, distributed ledger technology applications ranked at the foot of this list. At the current time, respondents indicate that they expect to be allocating their investment resources to other projects (such as the three areas outlined above) – and in some cases, they are unconvinced by the applicability of DLT to their business area or by the level of maturity of the technology. In the longer term, however, respondents tells us that DLT will play an important role in the technology development strategies, as indicated later in this survey in figure 15.

©2019 funds europe