Despite being Latin America’s third-largest economy equity managers aren’t unified on the merits of Colombia. This isn’t the case for bond managers, discovers Nick Fitzpatrick.

Perhaps no country in Latin America divides opinion about its investment promise more than Colombia. As Latin America’s third-largest economy, it is arguable that international equity fund managers are less unified on this oil- coal- and gold-exporting nation than they are about Brazil, Chile and Mexico.

This is not the case for bond managers: Colombia has enjoyed demand for its local currency bonds as much as other emerging market countries have done.

For active equity managers Colombia may need more conviction to be significantly included in portfolios.

The other large economies, particularly Brazil and Mexico, variously dominate the top country exposures in Latin America equity funds. A number of managers with international funds in Luxembourg, such as the Comgest Growth Latin America fund, have no exposure to Colombia. Others, at around the mid-year point, had a relatively low exposure.

Charles Biderman, Comgest Latin America fund manager, points out that Comgest’s investment philosophy is a bottom-up process focusing on picking quality growth stocks, rather than asset allocation. But he also says he is “very interested” in Colombia’s long-term potential.

Biderman highlights a young and dynamic population, pro-market policies and increasing demand for investment in different sectors.

He also says he is monitoring the impact of Colombia’s upcoming transition to International Financial Reporting Standards, “as we believe this will bring much needed clarity on accounting”.

But liquidity and valuations remain a problem.

“The size of the equity market is rather limited, discounting the banks and the national oil company, and the liquidity rather constrained,” he says, adding that the limited choice of companies, coupled with the dominance of Colombian pension funds, leads to prohibitive valuations.

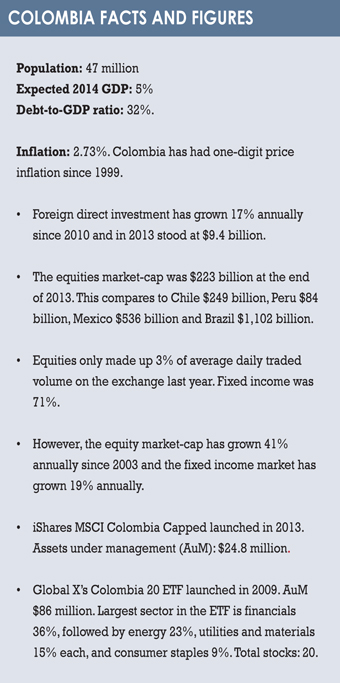

Colombian pension fund assets have grown significantly, hitting $88 billion in 2014, up from $7 billion in 2003, according to data from the Bolsa de Valores de Colombia, the stock exchange.

The market-cap of the equities market was $223 billion at the end of 2013. Equities only made up 3% of average daily traded volume on the exchange last year. Fixed income was 71%.

However, the equity market-cap has grown by 41% annually since 2003 and is growing further.

F&C Investment’s F&C Latin American Equity fund had a 5.5% country exposure to Colombia in July. This was the fund’s fourth highest country exposure, ahead of Peru, but behind Brazil, Mexico and Chile, in that order.

The Schroder ISF Latin America Fund was overweight Colombia versus its benchmark – 6% against 5.4%. However, Colombia was still only the fund’s third-largest country exposure and it was considerably smaller, too, than Brazil (60%) and Mexico (26%).

Aberdeen’s Global Latin America Equity Fund had a 3.3% exposure to Colombia – the fund’s fourth-largest country allocation after Brazil, Mexico and Chile.

Even an investment management player based in the region, Brazil’s Bradesco Asset Management, put Brazil, Mexico, Chile and Peru over Colombia. Colombia was its fifth-largest country allocation at 3%.

PEACE PROCESS

One of the largest country equity exposures, however, was the Neptune Latin America fund. London-based Neptune’s fund had its third-largest country allocation to Colombia – standing at 16.2% – after Brazil and Mexico. What attracts Neptune is the country’s strengthening economic data and the peace process under the country’s president, Juan Manuel Santos, who was re-elected to a second term in May. The peace process has diminished fighting between the army, drug gangs and rebels, which has dogged Colombia for decades.

A Neptune fund report said: “The re-election of Juan Manuel Santos as president was … a positive development. The economic policies of Santos and opposition candidate Oscar Iván Zuluaga were broadly similar, but they had very different policies regarding the peace process with the FARC [a Marxist revolutionary group].”

The report adds: “A continuation of negotiations is likely to yield results sooner and with lower costs, which should help stimulate investment and lower security costs in the medium term.”

A further sign of confidence in Colombia comes in the form of Ligia Torres, head of Asia Pacific and emerging markets at BNP Paribas Investment Partners. She cites Colombia as a key market for the firm in attempting to build its client base and assets under management. In Latin American countries, Mexican-born Torres says political risk – which she describes as the main driver of the emerging market premium – is reducing. The reduction follows some years of political continuity, demonstrated by smooth general elections and a cohesiveness of economic policies.

Encapsulating the favourable economic picture is Colombia’s improved credit rating. The rating reached investment-grade in 2011 for the first time in a decade. S&P moved first, followed by other agencies, and the rating improved further with S&P awarding a BBB rating, with a stable outlook, in April 2013.

The rating is in line with Brazil, Mexico and Peru and followed a boost in tax revenues thanks to the improving economy and the peace talks that have promoted investor confidence.

Colombian bond yields have fallen after a surge in foreign investment. The yield on the 10-year government bond stands at 6.5%, compared to Mexico’s 5.7% and Brazil’s 11.3%. In May, JP Morgan said it would add more of Colombia’s debt to its widely followed GBI-EM Global Diversified bond index. Colombia’s weighting was set to rise to 8.05% from 3.24%.

The maximum weighting in that index is 10%.

The maximum weighting in that index is 10%.

Explaining its move, JP Morgan noted the “improved transparency and accessibility for international investors” in Colombia’s government bond market.

Last year, the Colombian government cut the taxes foreigners pay on bonds as part of an effort to increase sales to foreign investors. The bank has noted that the surge of foreign investment that is driving down bond yields has also allowed corporates to prepare debt issues at lower rates. According to reports, in January Colombia successfully tapped the demand for emerging market debt after it sold $2 billion of 30-year bonds to overseas investors. The issue, priced to yield about 5.6%, attracted $4.2 billion in orders.

Colombia’s growth is expected to pick up this year, with subdued inflation, while its neighbours struggle with rising inflation.

Bradesco noted that the Central Bank of Colombia, which recently increased the interest rate by 25 basis points to 4.25%, revised the economic growth forecast for 2014 upwards from 4.3% to 5%.

In contrast, Chile has seen poor economic performance, with retail sales below expectations and a reduction in industrial production.

STOCK REACTION

So how has Colombia’s stock market reacted to all of this?

Perhaps not unexpectedly, it has been rising, though so have other Latin American and emerging market equity indices.

The main Colombia exchange-traded fund (ETF) – the iShares MSCI Colombia Capped listed in New York – returned 9.92% in the year to August 29, according to Yahoo Finance data. This compares to iShares MSCI Mexico Capped return of 8.56%, though both are a long way behind the iShares Brazil ETF, which returned 24.3% in the same period.

In the second quarter, the MSCI Latin America Index climbed 4.32%.

Many signs may point to an improved equity investment opportunity in Colombia. The peace process is welcomed – not least by the population. Political stability endures.

But for Comgest, it isn’t quite time. Either a broader market, or a pension fund shift to international investment, are needed.

“Investments from Colombian pension funds in local equities are high because the market is tiny, rather than in absolute terms,” says Biderman. “We have seen this in the past in Poland and in the region of Chile. This structurally pushes valuations higher and these valuations will remain high until the day regulation changes and Colombian pensions funds can invest more abroad.

“When this happens, there will be significant disruption to the market.”

©2014 funds global latam