One explanation for the strong growth of ETF assets in the US is that the American market is large and unified. Although Europe has achieved a high level of regulatory harmony, there are a large number of different exchanges operating on the continent. We asked our respondents if they thought the European ETF market, by being spread across many exchanges, was too fragmented. A majority (55%) agreed, of which 16% strongly agreed (see figure 5). Clearly, many respondents would like to see greater unification of Europe’s ETF market.

ETFs do have some accessibility benefits, however. We asked how ETFs compared with other fund types in terms of access to market. The most popular answer, attracting 39% of the responses, was that they ‘can be traded through international exchanges’ (see figure 6). Clearly, our respondents recognise that funds can both be exchange-traded and international. A close second was ‘offer a quicker route to market than Ucits funds’, attracting 35% of the responses. This finding suggests ETFs may sometimes be more appealing than conventional fund vehicles for asset managers hoping to launch products rapidly.

ETFs do have some accessibility benefits, however. We asked how ETFs compared with other fund types in terms of access to market. The most popular answer, attracting 39% of the responses, was that they ‘can be traded through international exchanges’ (see figure 6). Clearly, our respondents recognise that funds can both be exchange-traded and international. A close second was ‘offer a quicker route to market than Ucits funds’, attracting 35% of the responses. This finding suggests ETFs may sometimes be more appealing than conventional fund vehicles for asset managers hoping to launch products rapidly.

However, there are some controversies regarding what ETFs should be permitted to do. We asked how ETFs should operate with regard to securities lending and collateral management. The most popular answer, attracting 37% of the responses, was ‘ETFs should not do securities lending’ (see figure 7). It seems many respondents believe the structure of ETFs means they are inappropriate for this kind of activity, despite the potential to increase returns for investors. This result was not unanimous, though. A quarter of respondents said ETFs offer good prospects for additional returns via securities lending, while 26% said the decision should lie with the investment manager.

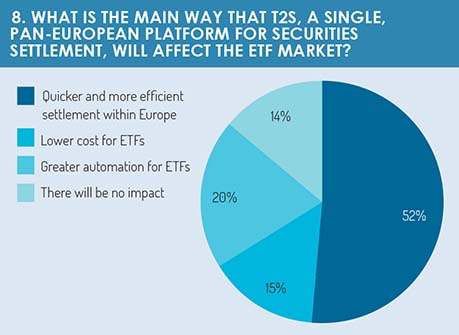

To return to the question of fragmentation, it should be noted that European authorities have embarked on various initiatives to make Europe’s capital markets more interconnected. One such initiative is TARGET2-Securities, a single, pan-European platform for securities settlement. We asked our respondents what effect this scheme would have on ETFs and the most popular answer, with 52% of the responses, was ‘quicker and more efficient settlement in Europe’ (see figure 8). There is room for optimism among those who think ETF settlement could be improved.

To return to the question of fragmentation, it should be noted that European authorities have embarked on various initiatives to make Europe’s capital markets more interconnected. One such initiative is TARGET2-Securities, a single, pan-European platform for securities settlement. We asked our respondents what effect this scheme would have on ETFs and the most popular answer, with 52% of the responses, was ‘quicker and more efficient settlement in Europe’ (see figure 8). There is room for optimism among those who think ETF settlement could be improved.

TARGET2-Securities (T2S) by itself may not, however, be enough to solve all the challenges related to market fragmentation. Clearstream has solved some of these problems with their issuance offering, in which the Luxembourg-based market infrastructure provider offers cross-border functionality for ETFs via T2S and via its international central securities depositary (ICSD). The results of our survey suggest more needs to be done to explain the benefits of such schemes, however, with 40% of respondents stating there is ‘no importance where an ETF is issued till it can be traded on multiple stock exchanges’ (see figure 9). A similar proportion, 36%, said they didn’t know how to answer this question. It would appear there is space for more education about the challenges connected to cross-border functionality of ETFs.

TARGET2-Securities (T2S) by itself may not, however, be enough to solve all the challenges related to market fragmentation. Clearstream has solved some of these problems with their issuance offering, in which the Luxembourg-based market infrastructure provider offers cross-border functionality for ETFs via T2S and via its international central securities depositary (ICSD). The results of our survey suggest more needs to be done to explain the benefits of such schemes, however, with 40% of respondents stating there is ‘no importance where an ETF is issued till it can be traded on multiple stock exchanges’ (see figure 9). A similar proportion, 36%, said they didn’t know how to answer this question. It would appear there is space for more education about the challenges connected to cross-border functionality of ETFs.

A similar result was obtained when we asked our respondents to consider the ICSD model, which has recently been chosen by some major ETF providers. The most popular result, with 39% of responses was, ‘the ICSD is not solving all operational issues’ (see figure 10). It would appear there is still more work to be done in this area.

For the next part of the report, click here.

©2017 funds europe