At the midpoint of an unpredictable decade, Funds Europe uses Towers Watson’s figures to look at how today’s global asset management industry compares with that of 2010.

At the midpoint of an unpredictable decade, Funds Europe uses Towers Watson’s figures to look at how today’s global asset management industry compares with that of 2010.

In a volatile decade marked by uncertainty, it’s instructive to compare and contrast the top 50 asset managers globally at the start of 2015 to those in 2010.

New names make the list and old ones disappear. But overall, assets under management (AUM) went up from $40.849 trillion (€37.2 trillion) to $50.205 trillion – a 23% rise.

The figures in this analysis are taken from Towers Watson’s The world’s 500 largest asset managers report, and are correct as of year-end 2014.

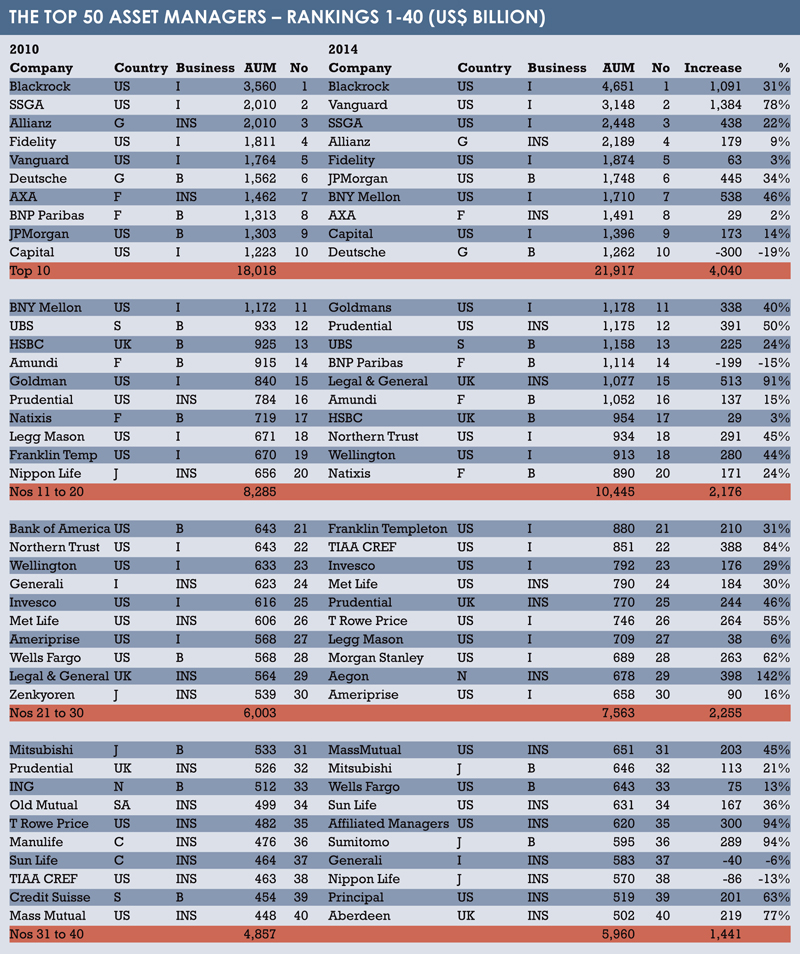

TOP 10 LARGEST FIRMS

The top 10 remains largely unchanged in terms of names, with BlackRock continuing to reign supreme. BNP Paribas no longer features (having fallen to 14), and BNY Mellon has joined (rising from 11).

Of those that remain from 2010, eight improved their assets under management, with only Deutsche Bank suffering a net reduction (of $300 billion – the firm fell from sixth to tenth as a consequence). Vanguard experienced the biggest increase in AUM, in both numerical and percentage terms ($1.4 billion, or 78%).

Aside from Deutsche, each firm enjoyed a net increase in AUM between 2010 and 2014; overall, AUM rose from $18 trillion to $21.9 trillion, an increase of 22%. On average, AUM increased by $404 billion.

THE NEXT TEN

There was greater movement in the next ten names. Franklin Templeton Investments fell from 19 to 21 (despite AUM increasing by 31%), Legg Mason from 18 to 27 (despite a rise of 6%) and Nippon Life from 20 to 38, its AUM falling by 13%.

The lower rankings can be attributed to strong relative performances by others, including new entrants Wellington, Northern Trust and Legal & General (which leaped from 29 to 15, and saw its AUM rise by 91% during the period in question).

Overall, AUM in this group increased by $2.2 trillion (26%) to $10.4 trillion in all, with an average increase of $218 billion.

THE TOP 21-30 FIRMS

Only three names remain from 2010 – Ameriprise, Invesco and Met Life – though these firms still saw increases in their AUM.

Ascending the ranks were T Rowe Price, whose AUM increased by more than half (55%), jumping $264 billion to $764 billion; Morgan Stanley, whose AUM grew by 62%, rose $263 billion to $689 billion; and TIAA CREF, whose AUM leaped 84%, from $463 billion to $851 billion. Most significantly, Aegon rose from 63rd in the top 100 in 2010 to 29th in 2014, with AUM growing by 142% to $678 billion.

Wells Fargo and Generali slipped down in the rankings, but Zenkyoren fell off the listings entirely after losing $12 billion to the 2011 Tohoku earthquake.

Overall, AUM rose by 26%, to $7.6 trillion.

THE TOP 31-40 FIRMS

Of 2010’s entrants, Mass Mutual, Mitsubishi and Sun Life remain, all having seen increases in their AUM. Old Mutual and Credit Suisse dropped into the next quintile. Manulife fell from 36 to 66, with AUM dropping from $476 billion to $272 billion (down 43%).

Manulife attributes this to the falling value of energy investments, prompted by the precipitous fall in oil prices since June 2014. ING likewise suffered, falling from $33 billion to $75 billion. However, this results from the firm divesting much of its AUM to new entity NN Group as part of its post-crisis restructuring.

Elsewhere, there are notable new entrants, such as Aberdeen Asset Management and Affiliated Managers, which climbed 21 and 15 places respectively to occupy positions 40 and 35. Total AUM rose by $1.4 trillion (23%) to $6 trillion.

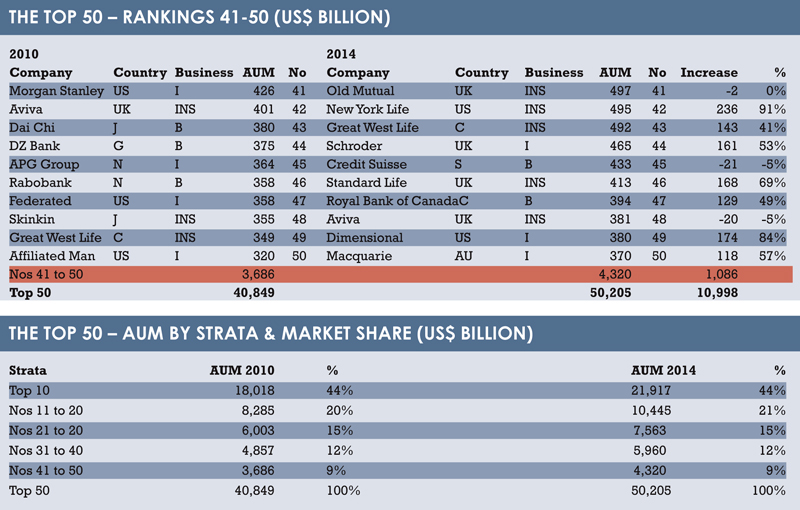

41-50: MAJOR CHANGES

This quintile has seen major changes – rises, falls and entirely new entrants.

Dimensional Fund Advisors, Macquarie Group, New York Life and Schroders – named in the report as the fastest-growing firms in 2014 – have all joined the top 50. Dimensional and New York Life saw their assets increase by 84% and 91% respectively.

Dai-ichi has disappeared entirely. In 2014, the firm combined with Mizuho Financial under the Mizuho imprint, but the entity’s AUM are not sizeable enough to plant the firm in the top 50. DZ Bank, which has suffered in the intervening years due to Europe’s ongoing economic struggles, has fallen out of the top 50 entirely.

Overall, AUM in this category improved by a modest $634 billion (approximately 17%).

CHINA: A JUMP IN ASSETS Notwithstanding the Chinese stock market’s ‘Black Monday’ in August 2015, and suggestions from some quarters that growth is finally slowing, the figures indicate China’s asset management industry has increased significantly since 2010.

Assets under management have jumped by $578 billion to $912 billion overall, an increase of 173%. The average AUM has increased from $12 billion to $29 billion, an increase of 141.6%. On an individual basis, some firms have recorded increases in their AUM of up to 620% (Bank of China).

While the same firms feature, new entrants have also entered the global 50; Baoying Fund, Huashang, HuaTai Pinebridge, SWS MU and Tian Hong. Between them, they account for $77 billion AUM.

INDIA: 136% GROWTH

Of 2010’s entrants, UTI Asset Management and State Bank remain. UTI’s AUM declined by $1 billion, and the State Bank of India’s increased by $2 billion – however, the AUM collectively held by India’s asset managers has increased from $41 billion to $97 billion overall, a hike of around 136%.

This is attributable to the arrival of three new entrants: Reliance Capital, Religare Enterprises and Birla Sun Life.

LATAM DECLINES

While in 2010, Latin America was tipped as a region abounding with growth prospects, since 2011 it has been hampered by economic slowdowns across the board.

This stoppage is reflected in the figures, with overall AUM declining by around 24% from $547 billion to $415 billion, and the average AUM of asset managers falling from $137 billion in 2010 to $104 billion today.

Banco do Brazil, previously the largest Latin American asset manager, no longer features. 2010 entrants Bradesco and Itau enjoyed AUM increases of $13 billion and $8 billion respectively, while Caixa’s fell by $4 billion.

Comprising $50 billion of the Latin American AUM is BTG Pactual. Since 2010, the firm has significantly expanded its asset management services, and has purchased regional brokerages Celfin Capital (Chile) and Bolsa y Renta (Colombia).

THE STEADY SWISS

Swiss firms increased their collective AUM to $2.9 trillion in 2014, up from $2.5 trillion in 2010 (an increase of 18.6%, or $470 billion). On average, firms increased their AUM by $40 billion, or 16%. However, average AUM remains largely unchanged at $230 billion (up from $229 billion).

This is perhaps attributable in part to several new arrivals in the rankings, including BCV, LGT, Vontobel and Zuricher Kantonal. Combined, they hold $332 billion AUM – 11% of the total AUM in 2014, but 70% of the increase on 2010’s total.

CANADA: NEW ENTRANTS

Since 2010, overall AUM have increased by $886 billion, from $2.3 trillion to $3.2 trillion. However, average AUM has fallen since 2010, partially driven by a rise in the number of Canadian entrants; BMO, Fiera, IGM, Industrial Alliance and Scotiabank. BMO is now fourth largest, with $326 billion AUM (around 10% of the total)

Manulife, in 2010 the largest Canadian firm, has dropped from first to fifth. Assets have almost halved, falling from $476 billion to $272 billion (down 43%) The firm attributes this to the falling value of energy investments, stemming from the plunging oil price.

AUSTRALIA: FEWER FIRMS

Since 2010, the number of Australian firms represented in the 500 has fallen from five to three, and total AUM has fallen to $583 billion from $632 billion.

Part of the reduction in entrants is attributable to the November 2010 incorporation of AMP into the AXA Investment Managers brand.

Conversely, the departure of NAB (National Australia Bank) from the rankings is not administrative. Since 2009, the bank has dented earnings by pursuing a strategy of undercutting retail banking and asset management competitors.

SOUTH AFRICA

Despite MMI Holdings’ AUM falling from $63 billion to $34 billion (down 46%), and Sanlam’s falling from $78 billion to $65 billion (down 17%), a 26% rise in Investec’s AUM, coupled with the entrance of Coronation Fund Managers (which holds $51 billion AUM) has resulted in total South African AUM rising by $32 billion to $261 billion since 2010.

JAPAN: CONTRACTION

The Japanese asset management industry was typified by contraction and conglomeration in the five years since 2010. Overall, AUM fell by $1.009 trillion between 2010 and 2014, from $4.94 trillion to $3.93 trillion.

Significant losses in AUM were recorded by most entrants over the period, most notably by Diawa. The firm’s assets fell from $164 billion to $47 billion (down 71%).

There were some increases, including Mitsubishi, which saw AUM rise by $113 billion to $646 billion (21%).

Orix Corporation, which did not feature in 2010, is now the fourth-largest Japanese representative on the list. Since 2011, it has expanded significantly into asset management, with the purchase of around 90% of Robeco’s equity.

Mizuho Financial and Dai-ichi Life Insurance combined in 2014 under the Mizuho imprint to create the eighth-largest Japanese entrant, with AUM of $226 billion.

Source: Towers Watson, The world’s 500 largest asset managers – year-end 2014

©2015 funds europe