Volatility in the solar sector is high. Nick Fitzpatrick looks at data from Markit, which indicates significant hedge fund interest in shorting, and speaks to a fund manager about why this may be.

The fortunes of the solar market rise and set like the sun. The industry seems to move through a series of boom-and-bust cycles as governments pursue renewable energy goals, handing out, then reducing subsidies.

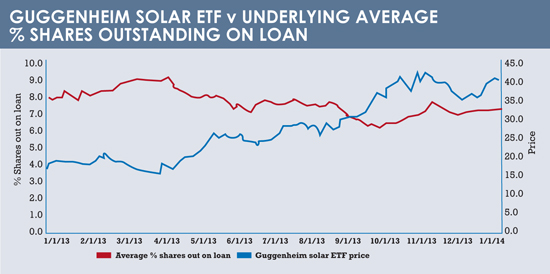

Equities in solar companies are fraught with volatility, and so it is no surprise that there is evidence of significant hedge fund short-selling activity in the sector.

The table shows the level of outstanding stocks in solar companies that were on loan in 2013 – or the level of “short interest”, which is how Markit, the data company that provided the information, puts it.

Shares on loan in these solar companies actually decreased over the year, indicating less short selling – though Andrew Laird, an equities product specialist at Markit, says: “The percentage of shares outstanding on loan [in solar] remains high compared to other sectors.”

The companies are drawn from the Guggenheim Solar ETF, an exchange-traded fund listed on the NYSE Arca and carrying the TAN ticker. TAN performed strongly last year, returning 127.8%. The long performance no doubt partly explains the decreased level of short interest. But the decrease was marginal, from 7.72% to 7.21% in 2012.

Most short interest centred around Chinese companies, both those with finance from American depositary receipts in the US, and companies listed in Hong Kong.

Lee Clements, an investment manager and solar expert at London’s Impax Asset Management, which specialises in resource efficiency and environmental investing, says that many Chinese solar companies have been unprofitable after a period of industrial build.

Lee Clements, an investment manager and solar expert at London’s Impax Asset Management, which specialises in resource efficiency and environmental investing, says that many Chinese solar companies have been unprofitable after a period of industrial build.

“There has been a rapid development of a very large Chinese industry. China now makes more than half of the world’s solar panels and this has seen the panel price slump by 70%,” he says.

China wants to reduce pollution through increased renewable power generation, which has led to more investment in solar. The country aims to produce 14 gigawatts (GW) of power from solar this year, up from 10-12GW last year.

One more issue potentially affecting all Chinese firms listed in the US, not just solar, is an auditing dispute between the Securities and Exchange Commission and the Chinese affiliates of the “Big Four” accounting firms.

SOLAR MANIA

But this is an isolated event and is the tip of the iceberg of the sector’s volatility. There are more underlying structural issues going back years and which largely centre on the various policy mechanisms designed to increase investment in renewable energy as governments seek to go greener.

A German initiative at the start of the century is sometimes seen as the mother of solar schemes. Germany introduced a feed-in tariff in 2004, meaning producers of solar electricity for the grid must be paid by grid operators. This caused an investment boom.

“The panel price did very well,” says Clements, “and there was a lot of venture capital activity and big IPOs [initial public offerings] up until 2007 and 2008.

“But then there was a significant reduction in the German feed-in tariff. A boom and boost situation developed for several quarters.”

Germany’s model has been widely copied.

“After the huge rush in Germany, other markets began to give generous tariffs, creating a rush in Italy and Spain.

“It is the deadlines for installation that create the rush. As the deadlines pass, a collapse has tended to follow.”

Reflecting other manias with a heady brew of new technology and private equity, the solar sector has seen insolvencies and astronomical price rises.

Germany’s Q Cells, created in 1999, floated in 2004 with private equity backing, and had to be rescued from insolvency in 2012 by a South Korean firm after China’s pricing power on solar panels impacted it.

Throughout the same period, the price of solar polysilicon, which is the raw material in solar panels, traded at $15-$30 per kg in the early 2000s, peaked at $300-$400 per kg in 2008, and is now ranging $20-$22.

A NEW DAWN

Clements says Japan could turn out to be last year’s biggest market, when the numbers are in. After the Fukushima nuclear incident, the country introduced a solar subsidy.

Also, despite no nationwide subsidy, in the US there is a tax credit that incentivises roof top installation and allows property owners to purchase electricity at a reduced market rate.

“These new markets have led to solar turning around up to the end of 2012,” he says.

Another ray of light for the sector is Warren Buffett, who attracted attention with large solar investments in 2013.

If these rousing developments continue, might it lead to a further reduction in short interest?

The sector would have to discharge its volatility first. But it may be the case that the level of short interest does not indicate a lack of faith in the technology, just in the ability of companies to efficiently monetise it.

©2014 funds europe