Over the past quarter of a century, Luxembourg has risen to be the main fund centre for Ucits processing. Nick Fitzpatrick looks back over some key events.

Think of a small country that has a feature of its commercial life so famous it belies the size of population or the expanse of land it covers.

Cuba (population 11 million) has its cigars; Panama (population 6.6 million) has its canal. Luxembourg (population 515,000) has its investment funds.

More specifically, they are “Ucits” funds, or ‘Undertakings for Collective Investment in Transferable Securities’, that the Grand Duchy is famous for.

When Brussels delivered the initial Ucits Directive to the European investment funds industry in 1985, which opened the way for a harmonised funds regime in Europe, it must have been hard to understand how a fund branded with such a cumbersome title and clunky acronym like Ucits could be marketed, especially to the general public.

But Luxembourg managed it. Though by their very nature Ucits funds are not the property of one particular country – rather Ucits is a set of rules meant to make funds in one EU country marketable in another – Luxembourg has become the nation most identified with the administration and distribution of these funds.

Chris Edge, managing director, JP Morgan Bank Luxembourg, says: “This was manifested for me just last year in Asia when I was talking to Asian asset managers about the basics of Ucits. The response you typically get is, ‘Ah, Ucits, that’s a Luxembourg fund, right’. That’s when you realise just how strong a brand it’s become.” (See roundtable starting on page 28).

ALFI IS BORN

In 1988, three years after the first Ucits directive was born, the Association of the Luxembourg Fund Industry – with the more approachable acronym of Alfi – launched. This year Alfi celebrates 25 years of existence, during which time Luxembourg has become the largest base for cross-border funds in the world.

The rise of Luxembourg’s funds industry began the same year as the founding of Alfi, when Luxembourg became the first country to transpose the Ucits Directive into national law.

Eleven years later, in 1999, Luxembourg became the largest fund centre in Europe, overtaking France for a while until 2002.

Then, in 2003, the country became the first to transpose Ucits III into national law. Ucits III broadened the types of assets available for investment funds – a move that still rankles some who fear greater complexity could damage the Ucits brand.

In May 2007 Luxembourg topped €2 trillion of assets, including non-Ucits funds, and by the end of the year 75% of all Ucits registered in at least three countries were Luxembourg funds.

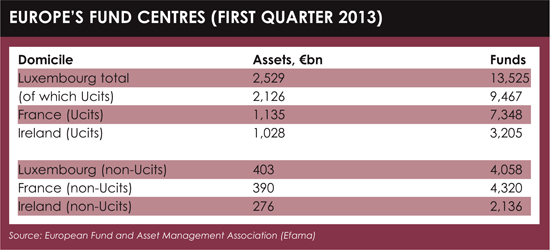

By 2012, Luxembourg was the largest investment fund centre in Europe, followed by France and Germany, and the second largest investment fund centre in the world, after the US.

Along the way, Alfi has raised the Luxembourg industry’s profile abroad, particularly Asia where it opened an office in Hong Kong in 2010.

A BRUSH WITH THE LAW

For its success, Luxembourg has depended primarily on a supportive government, a forward-thinking regulator (the Commission de Surveillance du Secteur Financier, or CSSF), and 14,000 staff, many who come in from neighbouring countries each day to work there.

But it has not all been smooth running. Luxembourg has been caught up in wider scandals, most recently the Bernard Madoff Ponzi scheme. LuxAlpha, one of the main European investment funds that placed money with Madoff, was a Luxembourg Ucits fund. It was a public relations disaster for Luxembourg.

For some, Madoff was not even the worst of the low points. That title goes to the Bank of Credit and Commerce International (BCCI), which underwent investigations into alleged money laundering and was forced to close in 1991. The bank was registered in Luxembourg, though its head offices were in Karachi and London. In London it was licensed to take deposits by the Bank of England, which was also criticised in its role of regulating the bank.

For some, Madoff was not even the worst of the low points. That title goes to the Bank of Credit and Commerce International (BCCI), which underwent investigations into alleged money laundering and was forced to close in 1991. The bank was registered in Luxembourg, though its head offices were in Karachi and London. In London it was licensed to take deposits by the Bank of England, which was also criticised in its role of regulating the bank.

The mud might not have stuck to the Bank of England, but ever since at least the BCCI scandal, Luxembourg has tried to fight off claims that it is associated with banking secrecy, on a par with various tropical boltholes. This perception particularly stings as the investment funds industry – trying so hard to disassociate itself from banks in all ways – moves towards ever-greater transparency.

As well as scandal, there has been disappointment. Luxembourg has not established itself as a major front-office centre, like London, though it would like to. Its expertise is in the operational departments – the middle and back offices – of fund management.

Ucits funds in Luxembourg, though, continue to thrive. The crown that Luxembourg wears as the pre-eminent Ucits fund domicile, administrator, and distribution hub is jealously eyed by rival Ireland. Luxembourg doesn’t have it all, though, and looks back enviously at the niche Ireland has created among US managers who, when they look to branch out internationally, often use Ireland as their key fund domicile in Europe.

ALTERNATIVE INVESTMENTS

The 25th birthday of Alfi comes at an auspicious time. Another fund acronym has entered the scene – AIFM, which derives from the Alternative Investment Fund Managers Directive (AIFMD), in force since July 22.

AIFMD enshrines alternative investments into a body of rules that, like Ucits, predominantly centre on how these funds are administered and distributed.

It brings Luxembourg into closer competition with Ireland, a strongly established service provider to alternative investment managers, and in readiness for this Luxembourg has overhauled its limited partnership regime to attract private equity firms.

AIFMD is the next main challenge and opportunity for Luxembourg. Further out on the horizon is the possibility of competition for fund servicing, and domiciliation, from other regions, particularly in Asia.

The next 25 years could end up looking very different from today.

* The following pages feature two roundtable discussions in Luxembourg. The first looks back on the past 25 years, and the second, starting on page 38, takes a broader view of the state of the funds industry.

©2013 funds europe