Nicholas Pratt examines the 2014 survey results and finds that although administrators all face similar challenges, they are dealing with them in different ways.

There are three new additions to this year’s third-party administrator survey. The first of these, Credit Suisse, cannot be considered a newcomer with more than 20 years of experience in the industry. The second, SS&C GlobeOp, is the result of a 2012 merger between the independent administrator GlobeOp Financial Services and the specialised software firm SS&C Technologies.

The third new survey entrant, Luxembourg-based Alceda, is representative of the numerous independent administrators with a line in alternative administration looking to grow their market share in wake of the imminent introduction of new regulation in Europe, notably the Alternative Investment Fund Management Directive (AIFMD).

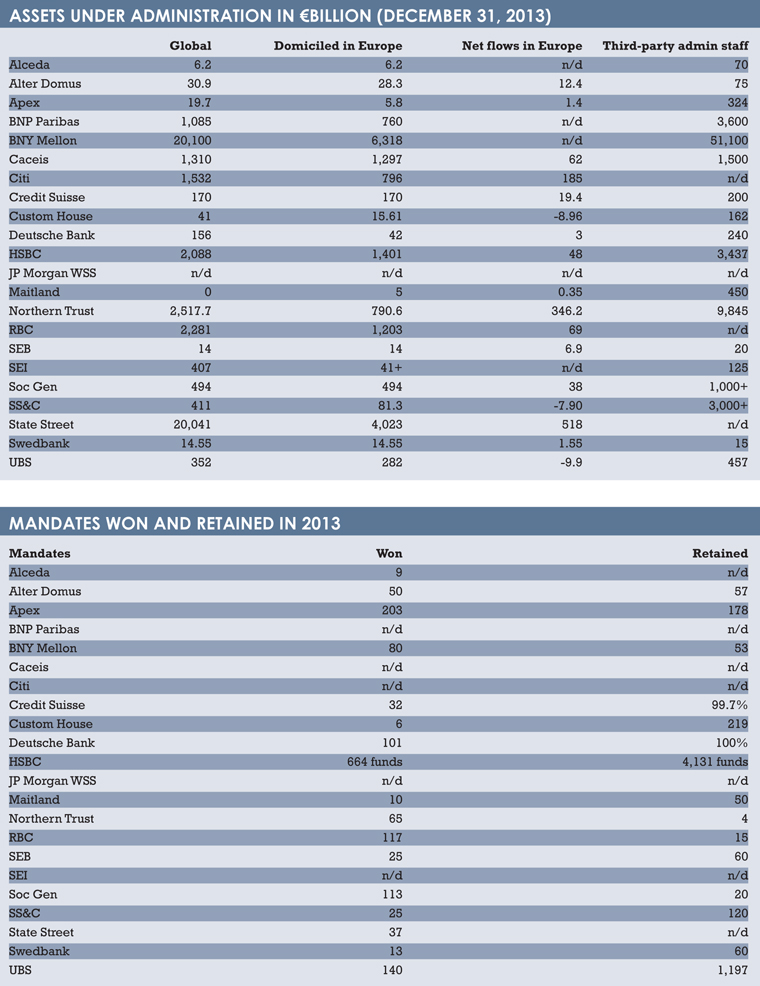

The majority of the survey respondents are bank-based asset servicing companies with more than €1,000 billion in assets under administration (AuA) while at the opposite end of the spectrum are the likes of Alecda, Alter Domus, Apex and Custom House – independent administrators with a background in alternatives and hedge fund administration.

The major theme of the 2013 survey was the increasing prominence of alternative administration and while this has become no less important, a much-talked-about trend in the fund administrations space during the last 12 months has been the difficulties facing independent administrators that do not have the luxury of a large balance sheet.

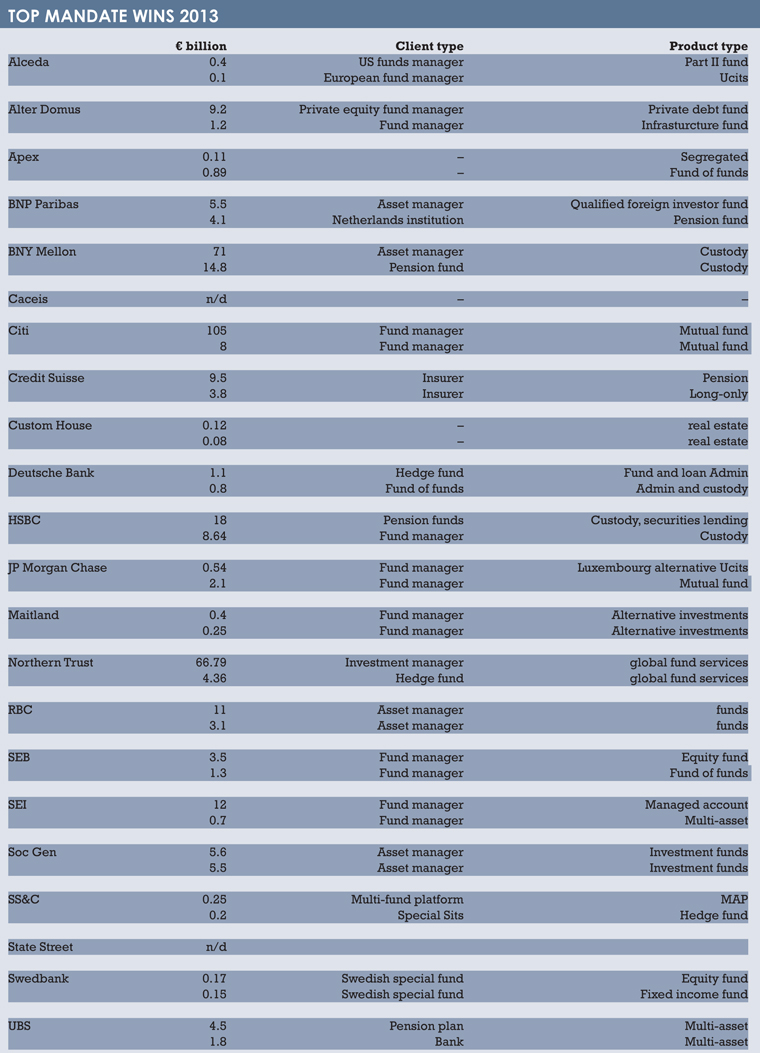

Looking at the flow of AuA and the number of mandates won or retained, 2013 was a positive year for administrators. There were positive net flows for all but three administrators (Custom House, UBS and SS&C Globe Op) and an aggregate figure of €942.66, excluding some of the largest providers such as BNY Mellon, BNP Paribas who were unable to disclose this information.

NEW SERVICES

Administrators are continuing to push new services to both meet clients’ demands and develop new revenue streams in reaction to pricing pressure. All agreed that the days of stand-alone administration are over, however different strategies are being deployed by the respective providers.

The larger administrators are looking to exploit their balance sheets and broad service offerings. HSBC has its “full outsource service” for middle office and investment operations. Caceis has its Prime Fund Solutions service comprising electronic execution services, clearing and collateral management. RBC has integrated its Investor Services division and established a specialist asset servicing business and is looking to further integrate a funding and liquidity management business.

Data is the most precious resource that administrators have at their disposal and is at the centre of the services they are looking to offer to managers, ranging from regulatory reporting to performance attribution and investor reporting. For example, State Street spent much of 2013 rolling out its data and analytics service Global Exchange, which offers research-driven investment data.

Meanwhile among the independent administrators, data has also become a key focus and a much more attainable part of their portfolio due to developments in technology. According to Mark Hedderman, chief executive of Custom House, “the spread of affordable technology has bridged the gap between front and back office reporting capabilities and therefore the end product of an administrator has evolved” to levels where administrators are offering front-office style reporting that is independently priced and reconciled.

RELATIONSHIPS

Pascal Berichel, global head of fund operations at Societe Generale Securities Services, says “the ability to leverage the large amount of data that are part of [the fund administration] business is becoming a key differentiator, by providing real time access to fully controlled information, reports and analytics”.

Managing the relationship with data vendors will therefore be a significant topic says Berichel, encompassing fee renegotiations and legal agreements for data dissemination purposes, from asset servicers to their clients. “This might deeply affect administrators’ business models and the way we interact with our customers and support their business development.”

CHALLENGES

The positive net flows enjoyed by the majority of the survey respondents should not belie the sizeable challenges facing administrators in the coming year. The key challenge for administrators, says Charles Cock, head of client development at BNP Paribas, is to “address expectations and constraints” resulting from regulatory change. Clients want “24/7 servicing, increased efficiency and decreased cost”. Administrators will therefore need to expand their servicing capabilities.

Unsurprisingly these demands have placed administrators under increasing pricing pressure. One reaction to this pricing pressure has been consolidation, thus enabling providers to exploit economies of scale, reduce operational costs and improve revenues. Of the large providers, Northern Trust has been the most notable acquirer of recent times when in 2011 it acquired both Bank of Ireland Securities Services and Omnium, the hedge fund administration arm of US-based investor services firm Citadel.

This has become a familiar pattern in the past 12 months with a number of hedge fund administrators being snapped up by mainstream players looking to build an alternatives expertise. Japan-based Mitsubishi UFJ Fund Services acquired Meridian Fund Services and Bermuda-based Butterfield Fulcrum. US-based Bancorp Fund Services bought the Dublin-based administrator Quintillion. And global outsourcing business TMF Group is set to complete its acquisition of Custom House

This is unsurprising given that regulations like the AIFMD are so new to the alternatives market and therefore likely to cause greater upheaval in the coming months. Regulated products will increasingly become the investment of choice for investors with AIFMD likely to create the same gold standard as Ucits funds and lead to Asian and US managers taking their strategies to Europe, says Michael Sanders, Alceda chief executive and chairman.

This globalisation of the asset management industry is “causing considerable headaches for market participants” and a “fundamental structural shift” in the asset management industry. For independent administrators, says Sanders, “new alliances and co-operations are more than necessary in such an environment”.

The AIFMD will also change the way many alternative managers operate in terms of service providers given the mandatory obligation to appoint a depositary for certain funds. For independent administrators, this will mean either developing a depositary service (or the more cost-effective depo-lite service) or else partnering with a custodian or depositary for this purpose.

Alceda, for example, has signed a depositary agreement with BNY Mellon and Maitland has similarly partnered with custodians to act as an independent third-party administrator. There may be similar deals and alliances that take place over the next 12 months as the new directive becomes implemented. For the independents that see themselves as the natural competitors to the service providers offering bundled custody and administration services, these partnerships will be an interesting development.

PRICING PRESSURE

Fund managers should consider themselves warned. It may well be a buyers’ market with administrators investing heavily but the pricing pressure they face brings with it the prospect of “service level creep” says Apex founder and chief executive Peter Hughes. “Services must be offered on a commercial basis. The market is ill-served by service providers that price below cost in order to maintain or buy market share, and this can only end in despair.”

It is a view shared by Joanna Meager, global head of client operations and head UK, at RBC Investor & Treasury Services, who refers to the number of providers “competing aggressively on price” and the need for a “disciplined approach to pricing” that is supportive of a “sustainable and profitable business model” as well as the “increased fee transparency and clarity” that managers are seeking.

This transparency should be a key factor in the relationship between managers and their administrators, whether they be independent or bank-based, or a global custodian or stand-alone specialist. As the environment changes, competition increases and price pressure starts to tell, it will become crucial that managers remember the importance of paying proper price for a proper service and are able to assure themselves that is the case from the fees provided by their providers.

©2014 funds europe