Hiring teams is becoming increasingly popular among asset managers as they aim to fill strategic product gaps and raise assets fast. Stefanie Eschenbacher finds this strategy is not without pitfalls when it comes to integration, cost and legal issues.

Hiring teams is a legal minefield. Several asset managers have crossed this minefield in recent months to fill strategic product gaps, raise assets more quickly and strengthen credibility.

Led by Habib Subjally, the 10-strong former First State global equities team is moving to RBC Global Asset Management; a four-man European equities team, led by Muhammed Yesilhark, is joining Carmignac Gestion from SAC Global Investors; two team members followed Richard Buxton from Schroders to Old Mutual Global Investors.

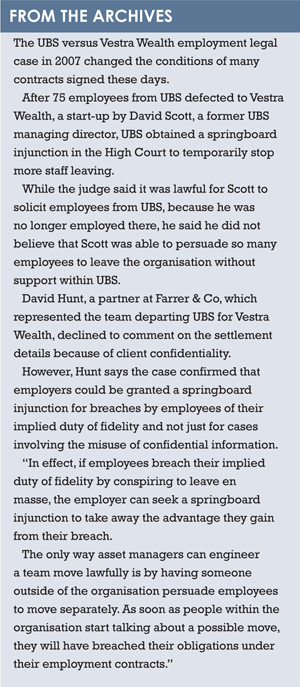

Since the defection of 75 UBS employees to Vestra Wealth in 2007, it has become far more challenging to hire teams from competitors (see box).

Today, many asset manager employees have tight contractual agreements that preclude them from soliciting other team members either before they leave or for a period after they have left.

How tight those clauses are is a major factor when it comes to what moves are possible or what the constraints are for an asset manager to hire a team.

When Buxton joined Old Mutual Global Investors in June last year, Errol Francis, who has worked with Buxton for 16 years at Schroders, and at Barings Asset Management before that, followed.

Poached by a third-party headhunter, Ed Meier, a co-manager, followed after the move was published. “It could have gone either way and was not a given that he would also join,” Buxton says of the tactical use of a third-party headhunter.

Poached by a third-party headhunter, Ed Meier, a co-manager, followed after the move was published. “It could have gone either way and was not a given that he would also join,” Buxton says of the tactical use of a third-party headhunter.

Now head of UK equities, Buxton says his team has been, and is, “crucial” to his performance. “There is a huge advantage of working with colleagues for many years. I have always said it is not something I could have done on my own, it is a team effort.”

Unrelated to Buxton’s departure and under different circumstances, Schroders itself created a convertible bonds team within its fixed income division in December, which included three people from Fisch Asset Management.

“It was probably the single case where we did not pursue a team, they pursued us,” Philippe Lespinard, co-head of fixed income at Schroders, says.

Schroders already had a business relationship with Fisch Asset Management, which had its convertibles experts working on its funds.

“That relationship became so big after a while, they thought they would be better placed if they ran the Schroders funds from within Schroders, rather than from a third party,” Lespinard says. “It was really their decision.”

Lespinard says team leaders are not only under a contractual but also a moral obligation to preserve their employer’s welfare.

“It is difficult for someone who is hiring to put the team head in a position where they have to persuade colleagues to leave because they are not allowed to do this. We have always dealt initially with the team head.”

He says if the team head asks for his colleagues to be considered, the team head is then advised not to mention it to his colleagues.

“We would then use a search firm, but we would never compromise someone’s integrity by asking them to pull out other employees,” he says. The team head, or whoever is being poached, would have to enter a contract in which he would not be allowed to tell the other members of the intention to leave.

“They will have to make their own decisions if they want to leave, independently of knowing whether someone else is leaving.”

Lespinard says in that process, asset managers learn a lot about “how committed everyone is to the rest of the team”.

Andy Smith, partner and head of Europe, the Middle East and Africa asset management practice, at Heidrick & Struggles, an executive search firm, says hiring teams is becoming ever more popular as asset managers aim to address strategic product gaps. He says there is considerable demand from institutional clients for concentrated and differentiated global equity strategies, which has led to demand for talent.

The same is true for emerging market equities, where assets are concentrated with a handful of players, like First State Investments and Aberdeen Asset Management. “Many asset managers still have a latent or active interest bringing in a team or successful senior fund managers to plug a capability gap,” Smith says.

Richard Phillipson, principal at Investit, a consultancy, agrees.

As investors are becoming slightly less domestic-focused, they look for global equity and global bonds strategies. Diversified growth and diversified income are other strategies where teams are in demand.

“They could hire individuals, build a philosophy and build up a track record, but that takes a few years,” Phillipson says, adding that asset gathering is quicker when hiring a team that has a credible approach that is scalable and replicable.

SOUL-SEARCHING

Didier Saint-Georges, a member of the investment committee at Carmignac Gestion, says there was “a fair amount of thinking, if not soul-searching” behind the hire of the four-strong European equity team from SAC Global Investors.

He acknowledges that Carmignac Gestion has never reached the same level of recognition in European equities it has in global equities, emerging market equities and fixed income.

The opportunity to change that came when SAC Global Investors closed its office in London last year. Its US headquarters, SAC Capital Advisors, is involved in a long-running insider trading investigation.

“One area we needed to add more value was in the bottom-up stock selection,” he says.

“The head of the team was running a long/short portfolio, which could be useful for one of our European funds.”

Saint-Georges says Carmignac Gestion has found “a chain that works together and onnects to the other parts of the investment team” in the team led by Yesilhark.

The hire is a complete overhaul of the French asset manager’s European team; Laurent Ducoin and two co-managers, Samir Essafri and François-Joseph Furry, have left since.

Dan Chornous, chief investment officer at RBC Global Asset Management, which has recently hired ten members of the former First State Investments global equities team, says there are clear benefits to bringing in new, experienced individuals and teams. “In hiring a team with established processes, we benefit more broadly as an organisation by learning from each other,” he says, adding that this is especially true because the specific skill set was not in-house.

“Their investment process is philosophically consistent with ours – deep fundamental research with strong quantitatively based portfolio management. With the core of the team having worked together for the past seven years, they have developed a positive synergy.”

Aiming to grow its investment business in the Asia Pacific region, BNY Mellon Investment Management has hired a six-strong team of investment professionals, led by Miyuki Kashima, all from ING Investment Management. Alan Harden, Asia Pacific chief executive officer, says the company had no domestic Japanese equities capability in Japan but it was something it wanted to offer.

“We could have done this organically and through hiring one person at a time as the business grew, but we had a rare opportunity to add immediate and deep expertise to our organisation.

“It was widely known in the market that ING was divesting its investment management operations in Asia, and Japanese equities was one of the areas they were looking to divest.”

Neuberger Berman hired 22 people to manage emerging market debt, 19 people, including the team head, Rob Drijkoningen, joined from ING Investment Management.

“We hired each of the team as individuals,” a spokesperson says. “This was not a team lift but rather hiring each person as they were right for the role we were filling.” Neuberger Berman declined to elaborate on the hiring strategies, saying only it is strengthening this part of its investment business.

ESCAPE

A spokesperson for ING Investment Management confirms that it is divesting part of its insurance and investment businesses, a condition for bailout money for ING, but says there are “no mass departures”.

Phillipson says that there are often both “push and pull factors” when it comes to hiring. “We talk about the desire to hire and there is a desire to escape something that is not going well,” he says of team moves in general.

“In some company structures, the team is operating as a business unit and probably has ambitions for itself quite as much as for the host company. What is it that makes a team become available?”

Hiring teams or individuals, it all comes down to a cultural fit. Some asset managers are effectively an office share where a promoter gives the fund managers a platform. Phillipson says as long as the team produces a promotable product, the team culture or the investment process is not a major factor.

Other asset managers have investment and cultural approaches engrained, and Phillipson says they need to find people who fit in and share fundamentals with the rest of the organisation.

“They might find it much easier to bring people in one at a time to absorb the culture and the approach that already exist, rather than transplant a team,” he adds.

Up until 2008, the prevalent approach was for multi-product boutiques to seek out high profile fund managers or small teams to free them from what Smith says were the “perceived constraints of big, European or global firms, to give them the freedom and autonomy of a boutique environment”.

One recent move of a high-profile fund manager to a boutique is that of Neil Woodford, Invesco Perpetual’s head of UK equities. He will join Oakley Capital Management in April.

One colleague from Invesco Perpetual and one former colleague will follow.

Neither Invesco Perpetual nor Oakley Capital Management was prepared to comment.

Today, hiring teams is more popular among larger asset managers with a strong distribution capability. Those hires tend to be into strategic product areas where they lack a presence.

Over the past couple of years, the emerging market debt sector has seen the highest levels of multiple hires or teams doing fills – asset managers hiring one or two senior fund managers from a team and complementing them with analysts. Smith adds: “Some asset managers have hired a team while others have hired a couple of members of the team but have not necessarily been able to hire the entire team they wanted so they have hired individuals to support that group.”

©2014 funds europe