German equity markets were the best performers in the developed world last year. Unfortunately, the Germans remained largely in bonds. Fiona Rintoul looks at why the German market did so well, and asks if it’s time to get out.

To misquote a line from the film The Producers, it’s been springtime for equities in Germany for some time now. Meanwhile, it has been winter, if not quite in Poland and France, certainly in southern Europe – or “peripheral Europe” as some people like to call it these days – particularly if they want to throw Ireland into the mix.

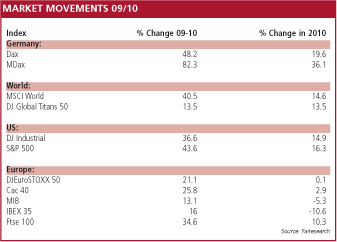

The table overleaf shows just how much better than the rest of the world the headline German index, the Dax, and most particularly the mid-cap index – the MDax – performed in 2009 and 2010. The nearest contender to this index is the S&P 500.

In Europe, the German index had no peers, especially in 2010, when it returned 19.6% against 0.1% for the DJ Eurostoxx 50, 2.9% for the headline French index, the Cac 40, and negative numbers in Italy and Spain: -5.3% and -10.6% respectively.

As for the MDax, it is way ahead of anything else in the developed world, returning a phenomenal 82.3% from 2009 to 2010.

Aviva Investors sums the situation up from a pan-European perspective in a recent research note. “The major industrialised nations of northern Europe and Scandinavia are growing at a robust pace, fuelled in part by the emerging market-led global economic recovery. By contrast, the economies of southern Europe and Ireland remain depressed as the first wave of austerity measures designed to restore their fiscal credibility and competitiveness begins to bite,” they were quoted as saying.

As a result of these trends, international investors have been piling into German equities – frequently described as the only European equities worth buying. As far back as 2008, Dresdner Kleinwort, the then investment banking division of Allianz Group, identified a trend towards greater investment in German equities by non-German investors.

A report on German companies’ share ownership and revenue trends released by Dresdner Kleinwort at the beginning of 2008 highlighted “evidence of a clear shift from domestic to foreign ownership of German companies, with US investors taking the lead”. The report found that the proportion of German equities owned by US-based investors had risen from under 2% in 2001 to 18% in 2006.

Foreign investors have maintained their interest in German equities. In May 2010, German equity was the top-selling fund sector in Europe, according to data from Lipper FMI, as canny investors took advantage of a temporary dip in the German stock market to buy up Dax exchange-traded funds (ETFs).

High performance

German investors will have accounted for some of those sales, but by no means all. They remain committed bond investors. While German investors have definitely taken advantage of their local stock market’s good performance to buy German country funds – the German fund association, the BVI, reported net sales totalling just over €2bn for German country funds from January to November 2010. Net sales of bond and balanced funds outstripped those of equity funds by €25.6bn to €8.8bn in the eleven months to November 2010, according to BVI figures.

“German investors in general have rather reduced their equity holding during the course of the past two years,” says Hans-Peter Wodniok, of the Kronberg-based independent research company, Fairesearch. “Germans aren’t equity investors. They got their fingers burnt when the market collapsed in the 1990s.”

At the same time as German country funds and direct holdings of German equities have been attracting considerable interest from foreign as well as domestic investors, European fund portfolios have been heavily weighted towards northern Europe, and Germany in particular.

“The market has made this blanket assumption that northern Europe is good and southern Europe is bad,” says John Surplice, fund manager for European equities at Invesco Perpetual.

So, what’s so special about Germany? How has the country produced the performance numbers it has and inspired confidence in investors worldwide?

First of all, the country still has a strong industrial base compared with other European countries. The love affair with services that has done for the economies of other European nations, most particularly the UK, never reached the besotted stage in Germany. German companies still make things and, as Christoph Ohme, senior fund manager at DWS Investments says, that doesn’t just mean that companies have things to sell, it also helps to maintain the brand name of Germany.

“In Germany we still have a manufacturing base, especially in small businesses in the engineering sector,” says Ohme. “You need a manufacturing base to keep up the brand. People like the brand ‘made in Germany.’”

Another important factor has been the businesses German companies have built up in the developing markets of Latin America and Asia, especially China. Many German companies were early to see the potential of these markets. Volkswagen, for example, was one of the first western car manufacturers to start a joint venture in China.

Chinese exposure

Having been active in the likes of China for some time, when export demand from developed markets fell away after the global financial crisis, German companies were able to fill the gap with sales to the still-growing emerging markets. A company such as Daimler saw its sales to China grow by more than 100% last year.

“Exporters benefited from exposure to emerging markets, particularly in Asia,” says Surplice. “Companies such as Siemens and auto manufacturers Daimler, Volkswagen and BMW all have significant business in China.”

Overall, Germany’s exports to emerging markets were higher than those of other European countries. Crucially, German companies were able to offer the kind of goods that consumers in the likes of China want.

“German car manufacturers are known for upmarket cars,” says Wodniok. “Those type of cars are in enormous demand in developing countries.”

Furthermore, consumers in the developing countries were willing to pay full price for their upmarket cars. “Those clients paid without negotiating discounts,” says Wodniok. “Demand recovered and the pricing situation was better.”

This, says Surplice, has led to a dramatic improvement in utilisation levels at plants in Germany. “The likes of Daimler did increase local production in China,” he says, “but the bulk of the demand was supplied out of plants in Germany.”

Road to recovery

Another factor that has helped Germany is low leverage among both consumers and companies. “Debt levels in Germany are lower than in other developed countries, such as the US, the UK and southern Europe,” says Ohme.

“That gives companies more flexibility to invest in certain growth regions,” he adds.

It also meant that consumers both suffered less in the downturn and were able to start spending again more readily when economic conditions started to improve – a crucial plus that will help to sustain confidence in German companies should either the US or emerging markets falter.

The question now is whether German equities can sustain their excellent performance in 2009 and 2010 into 2011. The law of averages would suggest not.

“The market that is the leading market one year doesn’t tend to be the leading market the next year,” says Surplice, who also points out that the German’s good performance over the past two years was partly due to cyclical factors.

“Whenever you get a downturn in the global economy, Germany does well because it has a lot of early cyclicals in its economy,” he says. “It supplies a lot of investment goods.”

In the most recent global downturn, the Dax headline index also benefited from the somewhat accidental fact of it being light on bank holdings, as compared to other European countries.

“Banks make up a low percentage of the German stock market because many German banks are savings banks and aren’t listed,” says Surplice.

The immediate aftermath of the downturn is over and the future beckons. Many feel it is unlikely that German equities will be able to keep up the exceptional performance they have demonstrated over the past two years.

“I cannot imagine that this type of outperformance will continue in the current year – except if the banking system has a major problem,” says Wodniok.

One problem is that the all-important car manufacturers are running at almost full capacity, leaving little room for expansion. And, says, Wodniok, they need to modernise.

Another is that, should demand for cars in emerging markets falter, domestic demand is unlikely to pick up the slack, although domestic demand is predicted to rise in overall terms in Germany. This is because so many cars were already bought under the government scrappage scheme introduced in 2008 that provided incentives for car owners to trade in their old cars for new ones.

But perhaps the most significant problem is the interconnectedness of Europe. However strong Germany’s export business in emerging markets such as China may be, in the end, the bulk of its exports go to its European neighbours.

“About 60% of exports still go to other European countries,” says Wodniok. “It used to be 65%. China was about three per cent. Now it’s 5.5%.”

Road to recovery

Recovery in distressed European markets, such as Spain, is not just essential for those markets. It is essential for Germany’s future development, too.

“Part of our exports go to these countries. Of course it’s important that we see a recovery and have a stable financial situation,” says Ohme.

The road to recovery for some of the distressed European markets is going to be long and hard. In some cases – Greece, for example – it can be quite hard to see how the necessary changes are going to be achieved. But in other countries, such as Spain, important steps have already been taken.

“Spain is a big country,” says Surplice. “Sorting Spain out is essential for Europe to have a reasonable recovery. If you look at what Spain has done on its budget deficit, it has done more than France or the US.”

Spain has also moved to reform its banking system, says Surplice. The number of savings banks has already been reduced significantly from 50 to the high teens. Pension reform and labour market reform are also on the agenda.

Such a programme for recovery in a core European country such as Spain will help German companies in the sense that it will secure their core export markets. But some fund mangers – Surplice, for example – also believe that investors have become rather myopically focused on Germany and northern Europe, and that it is now time to look beyond the German story when considering European equities.

Surplice compares the focus on Germany seen at the end of last year in particular to the extremes of the new technology boom at the end of the 1990s and start of the 2000s.

“There was a real move that you had to be in Germany and northern Europe, and have no exposure to peripheral Europe,” he says. “We need to take a step back and look at Europe. European markets are a lot cheaper than the US or emerging markets at the moment, and most of that value doesn’t reside in Germany right now.”

That, says Surplice, is not to say that Germany is overpriced. “It performed well last year for the right reasons,” he says.

And a Germany country fund manager, such as Ohme, sees plenty of reasons to optimistic about Germany’s performance in 2011. “The development of the German stock market last year was supported by very good fundamental developments,” he says.

Unemployment is decreasing and salaries are increasing. Plus there’s evidence that domestic demand is improving.

It is not that anyone thinks Germany is about to falter. However, in terms of the European picture, perhaps it’s time to rebalance.

“As a fund manager you look to the future,” says Surplice. “This year should be about the risk premium on European equities in peripheral Europe.”

©2011 funds europe