In scandal-hit Brazil, recession is on the cards and a political crisis threatens much-needed fiscal reforms. But as equity investors tell Nick Fitzpatrick, the country could bounce back sooner than many expect.

Let’s look on the bright side. Brazil’s stock market has been clawing its way up since at least the start of the year. In the months to May 11, the Ibovespa index had risen by 14.3%. Even the ordinary shares of scandal-hit Petroleo Brasileiro, known as Petrobras, had shot up 53%.

The turnaround in the Ibovespa, the main stock index, comes against a background of a much-welcomed battle against inflation. Brazil’s inflation rate is about 8%, above the official tolerance level of 6.5%. The benchmark Selic interest rate, held static at 11% for much of 2014, started to rise in October and stood at 13.25% in May 2015, with no sign of easing.

Fernando Honorato Barbosa, chief economist at Bradesco Asset Management (Bram), a Brazil-based fund house, says policy mismanagement landed Brazil in this situation, where high inflation and low growth are leading to recession. But he also thinks the economy is headed for a faster-than-average recovery.

“The inflation rate is not such a big risk any longer because GDP is very low and the unemployment rate is rising, meaning inflation will probably be tamed,” he says.

Unemployment in March stood at 6.2% of the working-age population.

Honorato acknowledges that Bradesco’s positive view is “out of consensus”, however.

INVESTOR SENTIMENT

Once an emerging markets star, Brazil has seen its fortunes alter dramatically, though this may be only temporary. Certainly the mix of inflation, low growth, a weaker currency, lower commodity prices and political uncertainty have affected investor sentiment.

Redemptions from Brazilian equity funds were seen earlier this year and persisted into May. That same month, allocations to Brazil in global emerging market funds were at their lowest point since 2003, according to data from EPFR Global, which tracks global fund flows.

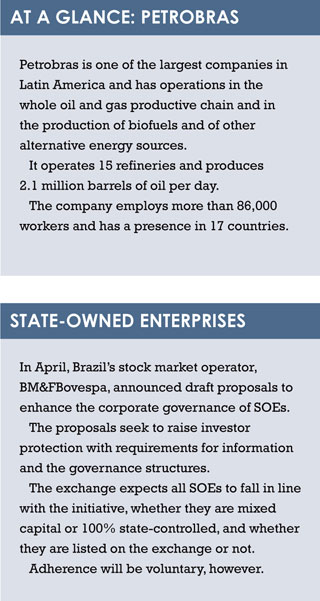

Since her election to a second term of office last October, the presidency of Dilma Rousseff has turned sour. Her popularity rating plunged to 13% earlier this year after Petrobras, a state-owned enterprise (SOE), was embroiled in a massive scandal involving bribery, money-laundering and racketeering. Top politicians have been implicated, and though prosecutors have given her the all-clear, the mud has stuck to Rousseff, who was chair of Petrobras from 2003-10.

Since her election to a second term of office last October, the presidency of Dilma Rousseff has turned sour. Her popularity rating plunged to 13% earlier this year after Petrobras, a state-owned enterprise (SOE), was embroiled in a massive scandal involving bribery, money-laundering and racketeering. Top politicians have been implicated, and though prosecutors have given her the all-clear, the mud has stuck to Rousseff, who was chair of Petrobras from 2003-10.

Central bank action on inflation may be welcomed, but given the public’s low opinion of the president, the government’s ability to drive economic progress further is debatable. For equity investors, it is very much a question of whether Rousseff will be able to push through fiscal reforms designed to help the economy, says Juliette Alves, portfolio manager of the Comgest Latin America fund. Comgest is a Paris-based asset manager with $22 billion of assets under management.

Alves says 2015 will be a year of recession, high inflation and high interest rates, and that the issues surrounding Petrobras add further pressure, particularly in terms of how fiscal reform unfolds.

“Everyone is focused on this because it will be an indication of where Brazil is heading. The question is, will the government be able to pass fiscal tightening? That is what the economy needs,” she says.

The fiscal measures consist of a gradual end to tax subsidies in several sectors that will impact the costs of many companies. Increases in payroll tax will affect quite a few industries, including industrials and IT.

Despite the pressure Brazilian equities have been under, companies that have successfully restructured themselves have extended their profit margins and surprised markets, says Alves.

BRIGHT SPOTS

She highlights BRF, formerly BRF – Brasil Foods, one of the world’s largest food producers, and Embraer, an aerospace conglomerate that is a large exporter.

Along with Natura Brasil, a cosmetics company that plugs into Brazil’s large domestic market, and Cielo, a Brazilian credit and debit card operator, these are quality companies providing some bright spots – though they are also exposed to the tax risks of fiscal reforms. Alves says the tax system in Brazil is very complicated and could affect many companies.

For her, a major risk stemming from the macro level for Brazil’s companies is the national currency, the real.

The real has devalued by about 40% over the past year. The currency’s weakness has helped push inflation higher and has negatively impacted local-currency bond flows.

“We don’t want companies to be indebted in hard currencies or have a big portion of their costs in US dollars,” says Alves.

Bram’s economist, Honorato, and Roberto Shinkai, senior equities portfolio manager, acknowledge that currency weakness has played a major role in the huge drop in equity investment.

That said, there are numerous other problems for Brazil, including power generation issues, drought, inflation and the political corruption surrounding Petrobras.

PRICED IN

Honorato says the high central bank interest rate will offer protection against further dollar appreciation.

“Four months ago, the real would have been a high-bid currency because Brazil was not carrying out policy changes. Whenever the dollar appreciates in the global economy, the real used to weaken much faster and higher than other currencies.

“But now I see the opposite happening. High rates and the right economic policy mean the real should devalue less,” he says.

He is supportive of the economic measures unveiled in recent months by finance minister Joaquim Levy, who was president of Bram prior to his appointment by Rousseff in January.

Shinkai, meanwhile, says stocks are positioning for a recovery. “Most of the factors, like the energy crisis and inflation, are already priced into the market,” he says.

“We are seeing risk sentiment for Brazil going down and equity prices are already predicting a longer-term recovery. Investors are looking at the next cycle and we are probably going to see a turning point in next two quarters.”

It is not known how the Petrobras scandal might affect Brazil’s economy, says Honorato.

It is alleged that construction firms paid about $2 billion in bribes to secure contracts with the state-run oil company.

Rousseff, who was elected president of Brazil in 2011 and October 2014, was chair of the Petrobras board at a time when bribes were being routinely paid.

Dozens of arrests have taken place, including politicians and senior business people, and thousands of jobs have been lost as firms caught up in the scandal lay off workers.

Some of the construction firms are important to the Brazilian economy.

“What we still don’t know is to what extent the operations of the federal police in Brazil will delay the recovery phase,” says Honorato.

“Many companies in Brazil are under investigation and many are important players in domestic construction. If they are out of the market for too long, it might delay recovery.”

He notes, however, that the government is considering bringing in foreign partners and small and medium-sized companies to be part of construction programmes around Petrobras.

Alves, at Comgest, says the scandal is a warning about SOEs in Brazil. She says her fund does not own any, and adds that most other private companies in Brazil are well managed.

“The scandal is of course very bad for perceptions of the country, but I don’t think it’s a reflection on the average corporate governance standards.”

TRICKY LEGISLATION

In 2000, the Brazilian stock exchange launched the Novo Mercado – a listing segment designed for shares issued by companies that voluntarily agree to abide by corporate governance practices and transparency requirements that are more rigid than those required by current legislation in Brazil.

“Most Brazilian companies have transferred to that market,” says Alves.

In a note written in March, Jan Dehn, head of research, and Gustavo Medeiros, portfolio manager at Ashmore, a London-based emerging markets specialist, noted positive developments at the political level.

For a start, the government managed to obtain approval for the 2015 budget, which locks in the fiscal adjustment proposed by the finance minister.

Also positive was the fact that a vote on “tricky legislation”, which could have resulted in increases in public-sector pensions, was postponed.

Rousseff has fostered good relations in parliament, which should serve to stave off the impeachment process some have demanded over Petrobras. As Dehn and Medeiros note, impeaching the president would pose a real threat to the ongoing and “absolutely necessary” fiscal adjustment.

©2015 funds global latam