Funds Europe sought the views of European asset managers in December with the first comprehensive survey on legacy systems. The results reveal just how much of a problem outdated technology poses.

legacy systems have long been the stuff of nightmares for asset managers’ IT departments. When the term was originally coined, ‘legacy’ referred to a 20-year-old system that was impenetrable to all but the individual who designed it. That person had left the company some time ago, but in the meantime, the system had become embedded in the heart of the IT infrastructure, lodged like a bullet in the cranium. You knew it should be removed, but worried that the process could trigger a fatal haemorrhage.

Things may be somewhat different in 2015 with the rise in outsourcing and with cloud computing starting to gain traction among asset managers. But legacy issues have not disappeared. There are still

four or five-year-old systems that are no longer supported by the vendor – and like a household appliance for which you can no longer obtain parts, these need to be replaced before they break down irreparably.

And as if that weren’t worrying enough, the pace of technological advances means that software has an ever-decreasing shelf life, granting systems the unenviable ‘legacy’ tag all the sooner.

Issues such as these have prompted an inaugural survey designed to shed light on one of the biggest and most persistent operational problems asset management firms face: the state of their legacy systems and how best to replace them.

In all, 67 executives responded. As well as heads of IT and chief operational officers, these included managing directors and chiefs of staff, lending weight to the argument that, far from being limited to technology teams, legacy issues are now boardroom concerns too.

The questions are grouped into three distinct categories. The first of these involves firms’ operational strategies and the nature of their planned IT investment; the second examines the prevalence of legacy systems, the operational problems they create and the economics of replacing them; and the final section looks at the alternatives to legacy systems.

The results show that legacy systems are still present in more than half of asset management firms and are widely acknowledged to be a problem – not so much in terms of their performance, but rather their lack of compatibility with other systems and the increasing cost of maintenance.

Conscious of software’s diminishing shelf life, it seems that more and more firms are considering alternative approaches to in-house installation such as outsourcing and cloud computing.

Fears over data security and the immaturity of suppliers is holding back wider adoption – but as legacy issues come to a head, many firms may be forced to overcome such concerns.

OPERATIONAL STRATEGY (QUESTIONS 1-3)

OPERATIONAL STRATEGY (QUESTIONS 1-3)

According to respondents, the primary drivers for firms’ technology investments are more or less evenly spread between operational efficiency (63%) and business growth (59.7%), with regulatory initiatives (49.3%) slightly behind and system consolidation/cost reduction (23.9%) trailing further back.

These figures support what we have heard anecdotally over the past 12 months – that the focus on cost-cutting and compliance, which has dominated budgets since the start of the financial crisis, is finally fading.

Instead, firms are now devoting the majority of their IT investment into more positive channels – either technology improvement or new product development and helping to support expansion into new products or markets.

Following years of miserly budgeting at some firms, IT infrastructure has been neglected and is in need of updating. The problem takes on an urgent note when a firm sets out to do something new, only to discover that system limitations are holding it back.

Looking at the answers to question 3 and the nature of firms’ operational strategy, only 38.8% of respondents state that their systems and processes are satisfactory. More than a third (34.3%) say that their current systems and processes are unable to meet the firm’s objectives, while almost a quarter say that systems and processes are under such strain that they will need either significant bolt-ons (13.4%) or significant upgrading or development (10.4%).

When we look at where firms plan to direct their IT investment over the next three years, overall IT infrastructure (58.2%) is the clear priority with an importance almost twice that of positions management, compliance and reporting (31.3%). In the past, most of an asset management firm’s IT budget was taken up with meeting new regulatory requirements. Given that this provided no competitive advantage, money was spent on quick fixes and patches.

Though compliance remains a big driver of IT investment, it seems that many firms intend to address the more profound and long-term development work needed at the heart of their IT infrastructure. One can assume from the survey results that some of this work will involve replacing legacy systems.

LEGACY SYSTEMS (QUESTIONS 4-7)

LEGACY SYSTEMS (QUESTIONS 4-7)

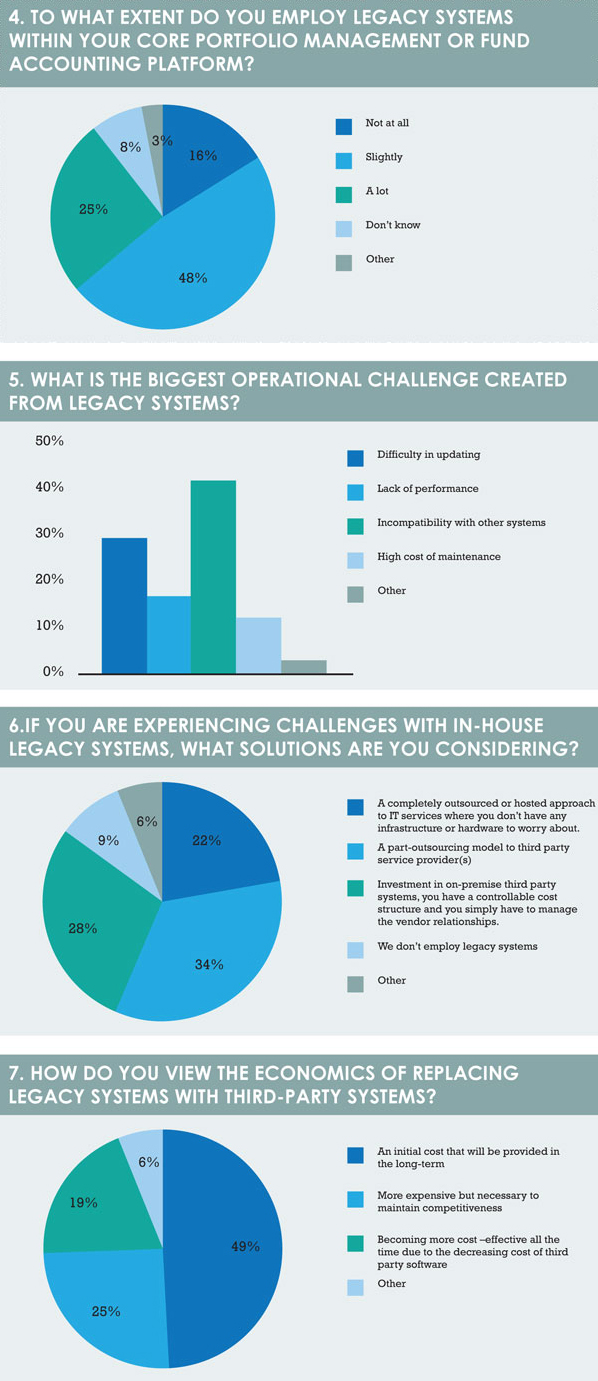

The most illuminating series of answers come from questions 4-7. Firstly, legacy systems are present within either the core portfolio management or fund accounting platforms in almost three-quarters (73%) of firms. There may, though, be some scepticism about the 16% of respondents who say they have no legacy systems at all.

While some companies may be in denial about the state of their IT, there are also a number of start-ups that have had the benefit of starting with a blank slate, either bringing in new technology or outsourcing the lot.

Of course, it could be that a number of firms are sufficiently well-organised to have ensured that their core platforms are free of legacy, limiting the blight of outdated systems to periphery platforms and technology.

Then there is the other possibility, indicated by the 7.5% of people who answered ‘don’t know’ to question 4, that people simply don’t recognise a legacy system when they see one.

Looking at the operational challenges created by legacy systems, it is clear that the most pressing issue is not a lack of performance (cited by only 16.4%). Instead, many of the challenges reflect firms’ relationships with vendors – either difficulty in updating systems (28.4%) or the high cost of maintenance.

The most commonly cited challenge was the incompatibility of legacy systems with other technology (40.3%). This provoked an additional comment from one respondent, who laid the blame for legacy issues at the door of vendors rather than users. “If a client has a legacy system, it is the provider’s role to adapt to the system and not to change it. The more you, the supplier, push against the legacy system, the more your clients will become frustrated by the inability of the new system to provide information with the clarity of

the old system.”

One is tempted to say: “Good luck with that,” but such a comment underlines the challenge facing vendors and clients when replacing legacy systems with a third-party alternative. As well as the operational risk that the replacement process will be highly disruptive and won’t perform as well or consistently as the old one, there is also an economic challenge.

Nonetheless, the survey results suggest most firms are confident that the replacement will prove to be economically positive. When asked, almost half of those surveyed (49%) accept that there is an initial cost involved but that it will provide a return in the long term. In addition, 19.4% believe that the decreasing cost of third-party software is making the process ever more cost-effective.

OUTSOURCING OPTIONS (QUESTIONS 8-9)

OUTSOURCING OPTIONS (QUESTIONS 8-9)

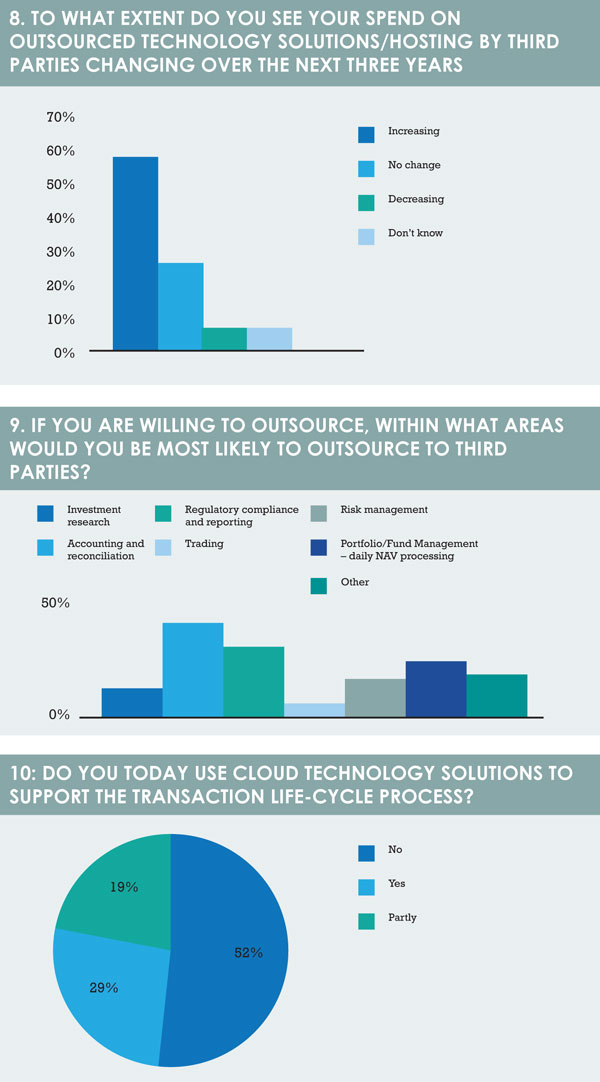

The alternative to installing replacement systems is to outsource. As question 6 tells us, more than half are taking this option with either a completely outsourced or hosted model (22.4%) or a part-outsourced model (34.3%). The response to question 8 suggests that the outsourcing trend is about to grow stronger, with the majority (58.2%) set to increase their spending on outsourcing or hosted solutions over the next three years and only a small minority (7.5%) likely to reduce this spend.

Looking more specifically at where exactly this outsourcing investment will be directed, the back office (43.3%) remains the main destination, but it is clear that other functions are increasingly considered to be suitable for outsourcing. These include risk management, investment research, portfolio management/daily NAV processing and even front-office functions such as trading (6.0%) that were previously considered too proprietary to be left in the hands of a third party.

CLOUD COMPUTING (QUESTIONS 10-13)

It’s apparent that firms are reconsidering which processes are a genuine core competency (to be kept in-house and as proprietary as possible) and which are commoditised and non-competitive. These considerations might be further influenced by the maturity of cloud-based services. Indeed, the final section of the survey suggests that asset managers are warming to the idea of storing data in the cloud.

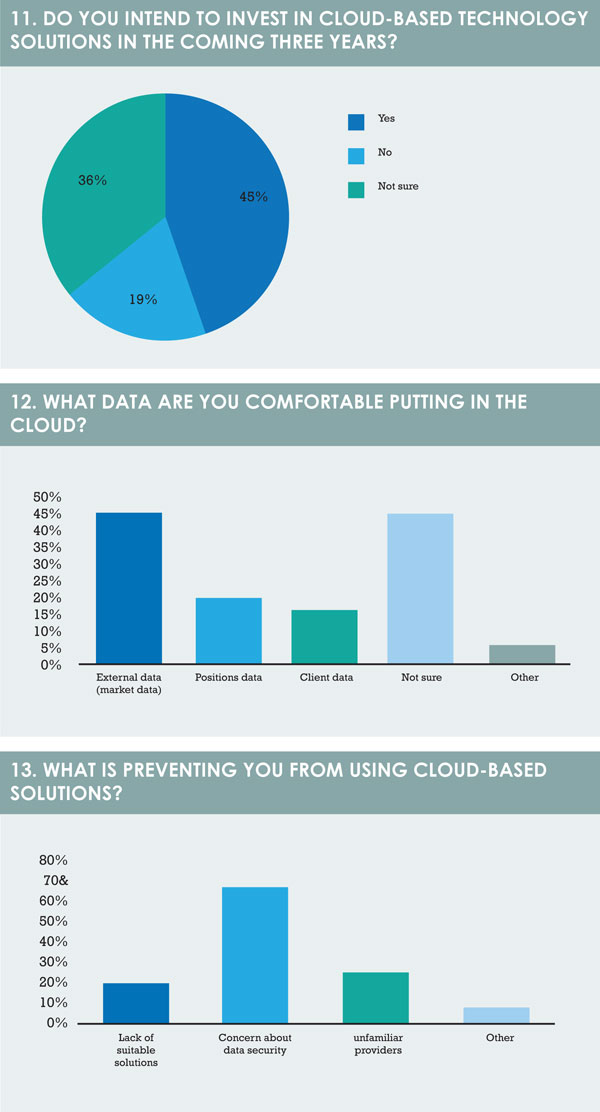

According to question 10, although more than half of the respondents do not currently use cloud solutions for any part of the transaction life-cycle process (52.2%), question 11 shows us that a similar percentage (44.8%)do intend to invest in cloud-based technology over the next three years. More than a third (35.8%) are unsure, leaving less than a fifth (19.4%) who have no plans to do so at all.

When it comes to data types, there are similar if not greater levels of uncertainty about how and where cloud technology would be deployed. For example, while almost half of the respondents (44.8%) are comfortable putting external or market data into the cloud, an equal number are unsure what sort of data they would trust to it.

Given that concern about data security is by far the biggest obstacle (67.2%) to the more widespread adoption of cloud technology, the uncertainty about what data to send to the cloud is only to be expected. However, as the other two hurdles mentioned are unfamiliar providers and a lack of solutions, the immaturity of the vendors is as much an issue as the concept of cloud computing itself.

As vendors in the cloud space become more familiar to asset managers and introduce a broader range of services, there is every reason to expect that

the adoption of cloud services will grow considerably in the years to come. In some respects, the timing could not be better. The issue of legacy technology has been around for as long as systems, and the time it takes for technology to become obsolete

is shortening all the time.

The days of an age-old portfolio management system remaining at the core of a firm’s IT infrastructure are definitely over, as are the days of the in-house designed system. But as more asset managers hand over IT responsibilities to third-party software vendors, the problems associated with legacy systems show no signs of disappearing.

These problems simply transfer to the vendors, whose responsibilities then include making sure their clients use the latest version of their software. What easier way to do this than to assume responsibility for IT maintenance on their behalf?

Though there may be some trepidation about the safety of their data (particularly confidential client data) and trusting their IT to a third party, the ongoing cost of avoiding legacy issues will hasten the move to outsourcing and the cloud. For many firms, the clock is ticking.

©2015 funds europe