What are active ETFs and why are they suddenly so popular? Nicholas Pratt has the details.

An active ETF has all the main properties of a passive ETF but the fund manager is able to deviate from the benchmark index and take active investment decisions about the underlying portfolio. The active ETF reflects, but does not mirror, the benchmark index and so there is a chance of higher returns.

Providers sometimes describe them as “enhanced” ETFs with all the attractions of a standard ETF (price transparency, daily liquidity, tax efficiency, low fees) but with the potential to generate returns above the index.

Having an active manager makes the ETF more agile in the sense of being able to react to market volatility by shifting away from underperforming positions.

However, allocating investments based on market conditions could make the fund less diversified than a true passive.

The existence of active ETFs creates a conundrum: Is an active ETF a cheaper version of an active fund, or a more expensive version of a passive fund?

And are these products aimed at active management devotees who want a more economical product, or are they aimed at passive investors who want someone to at least avoid the worst securities in an index?

The answer is all of the above.

How popular are active ETFs?

Most active ETFs invest in bonds, but adoption and performance have been underwhelming. There are more than 400 active ETFs in the US market alone and close to 800 worldwide, but they account for just 2.7% of the assets in the $7 trillion ETF market globally (end July 2020), according to consultant ETFGI.

Furthermore, over a quarter of those assets are held within just two fixed income-based active ETFs (Pimco Enhanced Short Maturity Strategy Fund and JPMorgan Ultra-Short Income ETF).

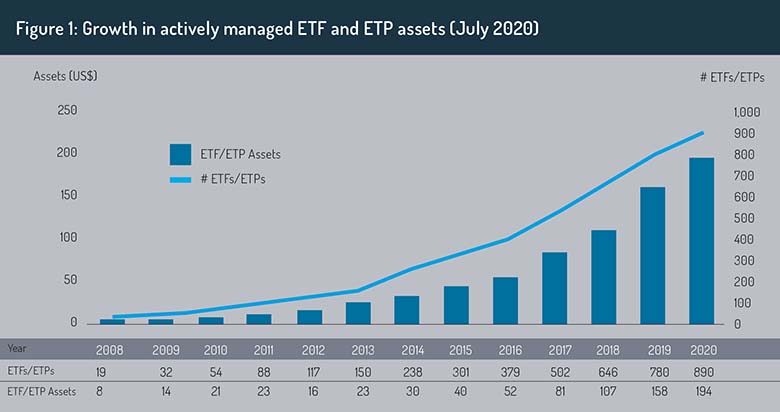

However the figures for the first half of 2020 (Fig 1) show much greater growth and with a number of large players – both established ETF providers and well-known active managers – entering the market, the forecast for the next two to three years is optimistic.

According to ETFGI, active ETFs reached a record high of $194 billion of assets under management by the end of July 2020.

This came after gathering inflows of $9.16 billion in July and $35.41 billion in the year-to-date period at July 31 – a figure almost twice as much as the $19.27 billion gathered in all of 2019.

The majority of active ETFs – nearly 68% – are still invested in fixed income. But inflows for equity products are growing faster, jumping from $4.05 billion in 2019 to $12.48 billion in July 2020. JP Morgan Asset Management (JPMAM) forecasts that 40% of all client money allocated to ETFs will be in either active (21%) or smart beta (18%) ETFs by 2023.

Why have active ETFs become more popular?

A turning point came with two decisions by the US Securities and Exchange Commission (SEC). The first was to introduce the ETF Rule in September 2019, removing the need for new ETFs to seek “exemptive relief” – basically reducing the time-to-market of new products.

Secondly, and more importantly, the SEC also approved five new ETF structures – created by Precidian, T. Rowe Price, Natixis/New York Stock Exchange, Fidelity and Blue Tractor Group – that remove the need for daily transparency about underlying securities. Previously, ETFs were required to disclose their holdings daily, a requirement which scared off many active managers worried that their investment strategies could be mimicked or that their trades would incur market impact.

The SEC move has led to a raft of active non-transparent ETFs, otherwise known as ‘ANTs’, which allow mutual fund managers to switch to an ETF wrapper but maintain quarterly – not daily – disclosure requirements.

These ANTs are viewed as ETF versions of active funds, a concept that is much easier to sell when they are being launched by well-known US-based active managers like Legg Mason, Dimensional Fund Advisors and American Century Investments. A further manager, T. Rowe Price, launched four active ETFs in August 2020 that have the same managers and follow the same investment strategies as some of the firm’s flagship mutual funds.

JP Morgan says active ETFs have the ability to achieve specific investment objectives such as sustainable investing, and this, says the firm, is likely to lead to many more active ETFs invested in equities as opposed to fixed income.

What will happen next?

Traditional active managers launching active ETFs is seen as a turning point and, for the first time, filings in the US for active ETFs outnumbered passive: 42 actives compared to 35 passives. Furthermore, there have been more passive ETFs closed than launched so far in 2020, a sure sign of a crowded marketplace.

It is also possible that the emergence of active ETFs may lead to a levelling of cost. Passive providers may have cheered the relentless erosion of margins for active managers but in the past two years, they have seen their own margins shrink thanks to fee pressure. Salt Financial in May 2019 applied a negative fee of five basis points to an ETF and attracted just $9 million. It is now being relaunched by new owner Pacer Advisors, this time with a fee of 60 basis points.

Proponents of active ETFs believe fees will come down, just as passive ETFs move away from zero or negative fees.

However, two of the biggest names in the passive world, BlackRock and Vanguard, could also be set to dominate the active ETF market.

In the recent JP Morgan AM survey, 320 respondents picked BlackRock and Vanguard as the two firms they would like managing their active ETF investments due to performance expectations and value for money. Yet JP Morgan AM says there is still plenty of runway for growth in the active ETF market, especially for those that will invest in equities.

Who will invest in active ETFs?

While active ETFs are no longer seen as a contradiction in terms, there are still plenty of market participants that will need to be convinced.

Winning over traders and market makers could be challenging because they like transparency and products that trade smoothly. Other active fund managers are unlikely to invest in competing active ETF products from rival firms. In some cases, investors may want to see a three-year track record before committing any capital.

The final and arguably most important challenge for active ETFs will be performance. All the benefits of the ETF structure – low cost, tax efficiency and price transparency – are reduced the more active a fund becomes and will be totally redundant if they are not matched with the returns of a five-star fund manager.

© 2020 funds europe