FactSet’s Adam Salvatori analyses some of the challenges of making the UN’s Sustainable Development Goals a reality, and looks at what role impact and ESG investors can play.

One of the keys to wider adoption of the UN’s Sustainable Development Goals is access to better data for both the social and environmental pillars. Prior to ESG going mainstream in the last couple of years, it was harder to get buy-in from asset managers and owners to incorporate ESG into the investment process.

Materiality became the lead talking point for ESG because any fiduciary would be required to incorporate sustainability issue to fulfil their legal obligations as they impact the financial condition, operating performance and enterprise value of companies.

The next logical evolution in the financial industry is to focus on the full suite of experienced stakeholder externalities, from both an impact and materiality lens. For the purposes of this commentary, an impact lens refers to the SDG goals and materiality lens refers to the Sustainable Accounting Standards Board (SASB) Materiality Framework.

The two vantage points – Impact (SDG) and Materiality (SASB) – overlap and can change as new issues emerge or erupt over time as we saw with corporate responses to the Covid-19 pandemic. Looking at both allows for a more holistic sustainability assessment.

Most SDG analytical offerings measure revenue assigned to individual goals. In certain cases, a corporate revenue lens might not be a good proxy for experienced stakeholder externalities. For example, a clean energy car company that has a history of poor labour practices should be evaluated not just on the goal of clean energy, which generates revenue, but also on the goal of decent work, which does not. This is an important difference and illustrates why having both perspectives are essential.

Gaps in existing SDG data include lack of company-reported data, greenwashing risk, data without the ability to capture both positive and negative information, and the need to measure country-specific Impact Signatures.

For example, when looking at the Truvalue Labs’ SDG Monitor’s data for US corporations it is evident that goal 16: peace, justice, and strong institutions, is a big focus with a dynamic impact of 27.3%, whereas in Europe it is just 12.4%. This is intuitive given a hyper focus on social factors in the US this past year and provides evidence of why a one-size-fits-all approach to SDGs is not suitable.

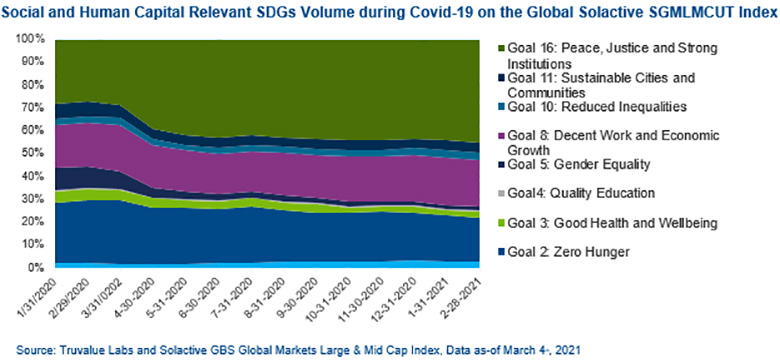

It is evident when looking at Sustainable Development Goals during the Covid-19 pandemic that stakeholder attention increased for social and human capital-relevant goals. Stakeholder attention increased for the following SDG Goals from January 2020 to February 2021: goal 1 (no poverty), goal 4 (quality education), goal 8 (decent work and economic growth), goal 10 (reduced inequalities), and goal 16 (peace, justice, and strong institutions).

Just as ESG has gone mainstream in the last couple years, impact investing is on the same trajectory to become axiomatic in the industry. The EU regulatory frameworks being put into place from the EU Green Deal and EU Action Plan will further accelerate adoption and increase the availability of sustainability information. The growing influence of impact investors, following in the footsteps of ESG, can help make the 2030 UN SDGs a reality.

*Adam Salvatori is global head of ESG client solutions and research at data research firm FactSet.

© 2021 funds europe