The bond bull market might – perhaps – be over, but QE is boosting Europe’s €480 billion high yield market, finds David Stevenson, who looks at the risk factors in the corporate bond market.

Bond fund managers may well be adding Mario Draghi, president of the European Central Bank (ECB), to their Christmas card lists. Though his trillion euro bond-buying quantitative easing (QE) programme has pushed sovereign yields to zero and below, it has also opened up opportunities in other, riskier fixed income areas for bond investors.

This comes at a time when some say the 30-year bull market in bonds is over, and others – such as Tanguey La Sout, head of European fixed income at Pioneer Investments – have said that European bonds offer no value.

But Draghi has a problem. Committed to buying sovereign bonds, the ECB was only able to buy debt with yields higher than the central bank’s deposit rate of -0.2%. Compounding this, those holders of eligible bonds – realising that they had a forced buyer of last resort who is not price-sensitive – may well have bought these assets ahead of the programme, waiting for prices to rise, as certain institutions are mandated to carry these assets anyway. With no viable income, they had to rely on capital appreciation of the bonds themselves.

Bill Eigen, absolute return bond fund manager at JP Morgan Asset Management, points out what most fixed income investors are thinking about the sovereign bond end of the market. “The only way to make money in bonds is through income and capital appreciation. Once you get to zero – or perhaps even go negative – then that’s it, you’re guaranteed to lose money or at best earn a zero return on your investment… Zero rates means zero opportunity for any income or capital appreciation.”

But then came the global bond sell-off in the middle of April. Prices dropped while yields rose. Draghi seemed back in business, allowing him to spread his printed money across a wider range of government bonds that had previously yielded below the -0.2% limit. If the ECB could now buy a wider range of bonds due to higher yields, fixed income investors may also have been tempted back. Meanwhile, TV networks such as CNBC were urging investors to buy anything but European bonds, feeling that bonds were still below fair value.

But then came the global bond sell-off in the middle of April. Prices dropped while yields rose. Draghi seemed back in business, allowing him to spread his printed money across a wider range of government bonds that had previously yielded below the -0.2% limit. If the ECB could now buy a wider range of bonds due to higher yields, fixed income investors may also have been tempted back. Meanwhile, TV networks such as CNBC were urging investors to buy anything but European bonds, feeling that bonds were still below fair value.

Recent moves in bund yields have been dubbed ‘duration tantrums’. Investors are not getting the income to cushion the losses on capital and duration has lengthened as yields have risen. One commentator has described this as “return-free risk, rather than risk-free return”.

The sell-off came at a time when China eased its monetary policy, triggering a recovery in oil and commodity prices. Markets realised that the spectre of deflation had ended in advanced economies and speculative positions in Eurozone fixed income were set for a reversal.

April’s events would have been catastrophic for anyone who had purchased bunds immediately before the sharp increase in yields. David Lloyd, head of institutional portfolio management at M&G Investments, says: “Your loss would be about 20% if you bought 30-year bunds a couple of weeks [before the sell-off]. On current yield levels, it would take about 20 years to get your money back”.

However, in the run-up to the sell-off, former sovereign bondholders turned to investment grade debt, and holders of investment grade bonds started to look at high yield (and may even have been tempted by emerging market bonds). The recent market correction was the biggest bund sell-off since 1990, although yields are essentially where they were last December.

It has not dampened investors’ appetite for other forms of fixed income, although QE did impact corporate bonds.

“In the short term, QE wasn’t good news for us. In March, corporate spreads widened because of the programme,” recalls Eric Vanraes, fixed income portfolio manager at EI Sturdza Investment Funds.

There are other reasons that explain the spread widening. David Zahn, head of European fixed income at Franklin Templeton, says it was coincidental that spreads moved out in March, as there was a lot of issuance at the time and the market had to digest this oversupply.

Olivier Lebleu, head of international business at Old Mutual Asset Management, sees the flows into investment grade bonds as a natural consequence of QE’s impact on sovereign yields. “The investment grade market has clearly been a beneficiary of the flows. You see that in fund flows and the extra interest that’s being asked to take on with investment grade risk, which are very low by historical standards,” he says.

QE did make credit incredibly cheap in Europe and attracted top US corporates such as Berkshire Hathaway, Kellogg’s, General Mills, Coca-Cola and most recently McDonald’s to execute ‘reverse Yankees’, where debt is issued in euros. But in April, even these top investment grade companies’ yield spreads were widening. At one stage that month, Berkshire Hathaway was up 33 basis points (bps), Kellogg’s 15 bps and Coca-Cola 14 bps, according to Bank of America Merrill Lynch indices.

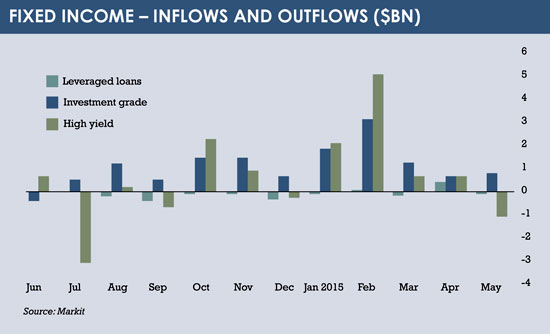

Still though, the appetite for investment grade debt from investors seems undiminished. Flows into iShares European investment grade exchange-traded funds (ETFs) have been around $2.7 billion (€2.5 billion) since the start of the year according to Brett Pybus, iShares fixed income strategist.

Flows into investment grade bonds, be they passive funds or active, were a reaction to QE. The question then is how much extra risk are investors willing to take on in an extremely low-yielding environment?

HOW LOW WILL YOU GO?

“In investment grade land, finance directors are noticing that triple-B is the new single-A,” says Lebleu. Companies that were once afraid of being stigmatised by a downgrade no longer seem as concerned because they have access to cheap financing.

Further down the scale in regards to high yield bonds, Zahn says there’s nothing wrong with taking on the additional debt as long as investors are paid the appropriate spread to take on additional risk.

“Has everybody who has taken on additional risk for additional return done that with their eyes open?” asks Lloyd. “I would say there is a heightened risk that people are taking risks that they don’t understand.”

Pybus says iShares launched a cross-over ETF product, designed to appeal to investors with lower risk aversion, which focuses on triple-B and double-B rated companies. Launched on February 3, it already has $290 million invested.

It should be noted that Tesco, the UK’s largest supermarket chain, is among those companies rated double-B. It was downgraded in part due to financial reporting irregularities (leading to the replacement of long-term auditors PwC), but illustrates that investors are attracted to so-called ‘fallen angels’ as they have the potential to bounce back and bring returns.

Typical double-B-rated bonds will yield around 3.5%; a single-B-rated company yields about 6.2%. But how much of these overall yields is made up of credit risk? The answer is 3.8% of the average yield of a high yield bond fund (which is 4.1%), according to Andrew Wilmont, Neuberger Berman’s portfolio manager for European high yield portfolios.

Given the additional yield for a single-B-rated company, some are frustrated that there hasn’t been much interest in them. Zak Summerscale, head of European high yield at Babson Capital Management, says: “Some institutions preclude them, but we think single-Bs are very cheap compared to the overall capital structure and are mispriced compared to triple-Bs and double-Bs. I expect some of the recent outperformance of double-Bs to trickle down to the single-B level, but it hasn’t happened as fast as it did for higher-rated bonds.”

He also says that, in his opinion, limiting the scope of investment mandates on ratings alone can be a mistake. He believes that rigorous bottom-up analysis on individual credits provides more insight into a company’s future prospects than looking at the credit rating assigned to a particular issuer by a rating agency.

Some active managers are prevented from entering the high yield bond market, which is fine by Vanraes. “I don’t like them,” he says. “Yields are attractive but you are not paid for the risk.” Vanraes also singles out the US energy market as particularly weak, but as others say, this market is now in a healthier position, in part because of the commodity price recovery.

Europe doesn’t have a great many energy companies – unlike the US, where companies in the sector were teetering on the edge of default for some time. But there are broad similarities between US and European high yield markets, each of which rose about 4% between February and May.

THIS IS THE END

‘Bond king’ Bill Gross, co-founder of asset manager Pimco and now with investment firm Janus Capital Group, famously stated recently that this was the end of the bond bull market, which had run for more than 30 years. The bull market probably goes some way towards explaining investor behaviour. As Bill Eigen says, investors have been conditioned to keep buying fixed income as it’s been in a bull market for so long.

If we are at the end of the long bull run, what happens if there is a huge market downturn, similar to 2008? Central bank intervention has brought interest rates down to zero and numerous QE programmes have stimulated economies around the world. What else do central banks have in their toolkit?

Vanraes says: “I pray that it won’t happen, but what if there’s another crisis in 2017? Before the last crisis, you had central banks with rates of 4%-5%, so you could afford to have a very accommodating monetary policy. But now all the central banks have negative rates. They have already done a lot of QE, an unconventional measure, so if there’s another crisis, what do

Vanraes says: “I pray that it won’t happen, but what if there’s another crisis in 2017? Before the last crisis, you had central banks with rates of 4%-5%, so you could afford to have a very accommodating monetary policy. But now all the central banks have negative rates. They have already done a lot of QE, an unconventional measure, so if there’s another crisis, what do

they do?”

The European corporate bond market has transformed over the past 10 years, growing exponentially. High yield does well in a secular stagnated market characterised by low interest rates and QE. The environment lets poorer-quality companies borrow money for refinancing, or what is mockingly referred to as ‘extend and pretend’. The European high yield market is worth around €480 billion, which is a fraction of the US market, valued at almost €2 trillion, according to figures from Credit Suisse. But the US had a 20-year head start on Europe and with comparable levels of GDP between the two regions, high yield and investment grade debt are on the ascendency.

Now all eyes are on the US. If the Federal Reserve tightens rates, managers will thrive in a divergent monetary policy environment. But with weak employment data in May from the US, this is not a foregone conclusion.

As the ECB continues its bond-buying programme with gusto, investors will continue to move along the spectrum, away from sovereigns to high yield.

©2015 funds europe