The final article in the ETF series considers trading and future developments. Written by Felix Goltz and Lin Tang, of Edhec, the article is based on research carried out as part of the Core-Satellite and ETF Investment research chair sponsored by Amundi ETF

One of the great advantages of ETFs is that they are easily traded on conventional exchanges. So we asked the respondents to the survey how much of their ETF trading is done over the counter (OTC), rather than on exchange. Although 58% of respondents do not trade a significant share of their ETF investments over the counter, more than 20% of respondents do more than half of their ETF trading on OTC markets.

The percentage of respondents who report that they trade more than 90% of their ETF investments on OTC markets has grown from 6% in 2009 to 12% in 2010. This growth reflects the greater willingness of ETF users to use more advanced trading mechanisms, which can lead to lower transaction costs; they thus benefit from the liquidity of ETFs without bearing the entire cost of this liquidity in the form of bid/ask spreads.

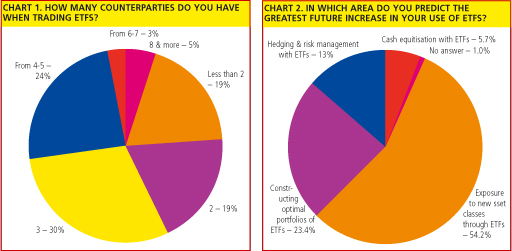

Next, we turn to the number of counterparties used when trading ETFs. On average, respondents use about three counterparties, with the mean at 3.29 and the median at three. Chart 1 shows the exact breakdown. Roughly 40% of respondents have up to two counterparties, and another 54% use three to five. Only 8% rely on more than five. This year, respondents are more likely to have more than two counterparties than they were last year. Possibly as a result of the 2008 financial

crisis, investors prefer to diversify their counterparty risk.

Advanced features

In our survey, we asked about the use of inverse and leveraged ETFs, options written on ETFs, the short selling of ETFs, and the use of ETF shares in securities lending.

ETFs packaged with advance trading strategies (inverse or leveraged ETFs) are used by about one quarter of respondents in spite of their recent appearance. By contrast, only some 10% of respondents write options on standard ETFs, sell them short, use them in securities lending or make other advanced uses of them.

Insufficient knowledge of advanced uses of ETFs is not a reason for the reluctance to use these products: indeed, only between 4% and 11% of respondents report that they are unfamiliar with them. The greater popularity of inverse and leveraged ETFs may be the result of their operational simplicity.

Inverse and leveraged ETFs are pre-packaged margin products. It is not necessary for investors to manage the margin account on their own as they must when they short ETFs by themselves. Moreover, the recent criticism of short selling in general may raise obstacles to shorting or lending ETFs.

We also asked whether those respondents who do not make use of ETFs for these advanced purposes intend to do so in the future. The results show that some 10% of respondents do indeed intend to do so in the near future, results that suggest a coming increase in the advanced use of ETFs. For instance, 11% of respondents are currently lending ETFs, and 10% report that they plan to lend them in the future. This is growth of nearly 100%, not even taking into account the growth possibly spurred by educating the investors who are unfamiliar with the strategy.

Future development of ETFs

Our questions have hitherto focused mainly on current uses of ETFs. A clear advantage of our survey methodology, which gives us access to investment management professionals, is that, rather than merely note what is being done, we can also analyse plans for the future.

We asked those surveyed to identify the area in which they predict the greatest increase in the use of ETFs. These areas include exposure to new asset classes through ETFs, constructing optimal portfolios of ETFs, hedging and risk management with ETFs, and cash equitising with ETFs.

Chart 2 shows that the greatest increase (chosen by 54.2% of respondents) is expected to come in accessing new asset classes. ETF providers’ strategies of covering new asset classes such as listed real estate, listed private equity, commodities, and even more specific alternative asset class segments would seem justified. Slightly more than 23.4% of respondents would like to increase the use of ETFs for optimal portfolio construction. By implication, respondents not only see ETFs as purely passive means of covering broad market segments, but also want to exploit diversification benefits from optimally constructed portfolios combining ETFs.

In recent years, as it turns out, asset managers have launched funds of ETFs whose sole focus is asset allocation. There is ample evidence that asset allocation strategies with ETFs may provide significant value add. Respondents seem to share this view and thus see optimal portfolio construction as a major area in which future use of ETFs may be increased. The other main area seeing growing use (23.4%) is risk management/hedging (13%). An increase in using ETFs for cash equitisation is predicted by only 5.7% of respondents.

It has now been ten years since the first ETF appeared in the European market. Over this period, the industry has matured and there are now more than 800 products available. Are investors interested in seeing still more products developed and, if so, of what kind?

Emerging markets equity ETFs (52%) are of greatest interest to respondents. About one-third of the respondents would like to see new products for alternative asset classes, especially for commodities (39%), currencies (28%) and hedge funds (27%). With 29% of respondents, ETFs based on new forms of indices also rank high on the wish list.

Unlike standard capitalisation-weighted indices, these indices are equally weighted or based on fundamental company characteristics, or on weights derived from portfolio optimisation. Emerging market bond ETFs are also of interest to investors (37%). By contrast, new products in ethical investment (14%) and actively managed equity (10%) are not in high demand.

On the whole, investment management professionals are thus requesting access to non-standard beta (emerging markets and alternative asset classes) or to traditional equity beta through new weighting schemes. On the other hand, investment managers are far less interested in ETFs that select securities either through ethical screening or through active stock picking by a manager.

Felix Goltz PhD is head of applied research, and Lin Tang is a research assistant at Edhec-Risk Institute

©2010 funds europe