“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.”

John D. Rockefeller, 1908.

In the current environment of ultra-low interest rates, investors are increasingly looking to equities for a source of income. However, high dividend strategies look attractive in today’s markets for a wide range of reasons.

When John D. Rockefeller, the world’s first billionaire and renowned philanthropist, remarked on his pleasure in receiving dividends from Standard Oil, he was inadvertently making the case for companies that pay high dividends. Not only do these stocks reward their investors with an attractive level of income, but their other qualities can translate into higher than average total returns.

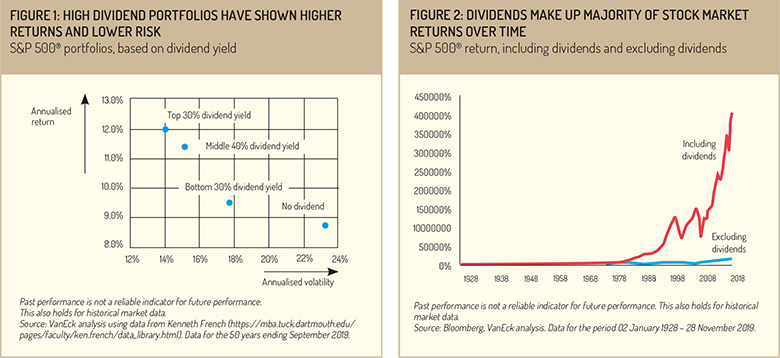

Historically, higher dividend paying stocks have shown both higher returns and lower levels of risk (see figure 1).

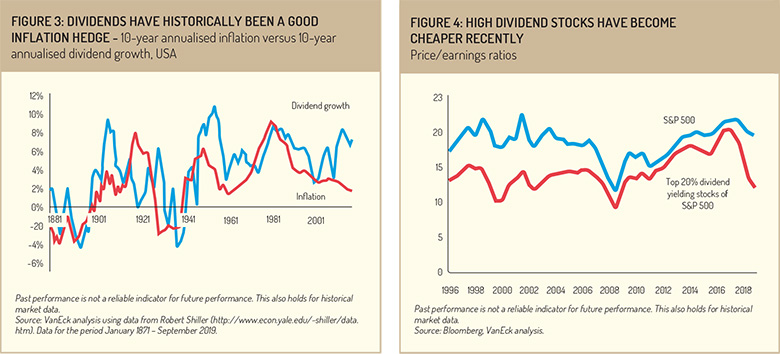

One reason given for high-dividend stocks’ superior risk-return characteristics is that a high level of dividend payout disciplines management. If a firm has too much free cash flow at its disposal, managers might be tempted to undertake value destroying projects, or spend on excessive salaries or perks. Another fact to consider is that, over the long term, dividends are the main driver of equity returns. In figure 2, we compare the performance of the US S&P 500 index including dividends and excluding dividends. It is clear that the former dwarfs the latter over time. Only a few companies have been able to generate above-average long-term returns from share price increases alone.

Dividends have also proved to be a good hedge against inflation. As can be seen in figure 3, dividend payouts have historically walked in lockstep with inflation levels. The explanation is intuitive: in periods of inflation, most companies can raise the prices of their goods or services, and as such, increase nominal earnings. This then translates into higher dividends.

But beyond the long-term arguments, high dividend strategies seem particularly well suited for the current macro-economic environment.

A high dividend equity strategy can nowadays yield between 4% and 5% when investing in blue-chip companies such as AT&T, HSBC, GlaxoSmithKline and IBM. In order to achieve such yields from Euro fixed income, one needs to make big sacrifices in both credit quality and duration.

Also, the fundamentals of high income strategies seem favorable. Currently, high dividend stocks are priced attractively, both in comparison to other stocks and to historical prices (figure 4).

Investors can find further comfort from current high levels of cash on companies’ balance sheets, which compare well with historical norms (figure 5). This gives companies sufficient capacity to sustain dividend payouts, even if their earnings fall. Yet despite the stockpiling of cash, current payout levels are below historical averages, giving leeway for further increases in dividend payouts.

Investors can find further comfort from current high levels of cash on companies’ balance sheets, which compare well with historical norms (figure 5). This gives companies sufficient capacity to sustain dividend payouts, even if their earnings fall. Yet despite the stockpiling of cash, current payout levels are below historical averages, giving leeway for further increases in dividend payouts.

John D. Rockefeller may have extolled the virtues of high dividends over 110 years ago, but his sentiment has held true over the long term. Given today’s extraordinary economic environment of low or even below zero rates, the attraction of high dividends is stronger than ever.

This publication is for marketing and informational purposes only and does not constitute investment advice. All data is sourced as at the date stated.

By Philipp Schlegel, Co-Head Sales Europe, VanEck

©2019 funds europe