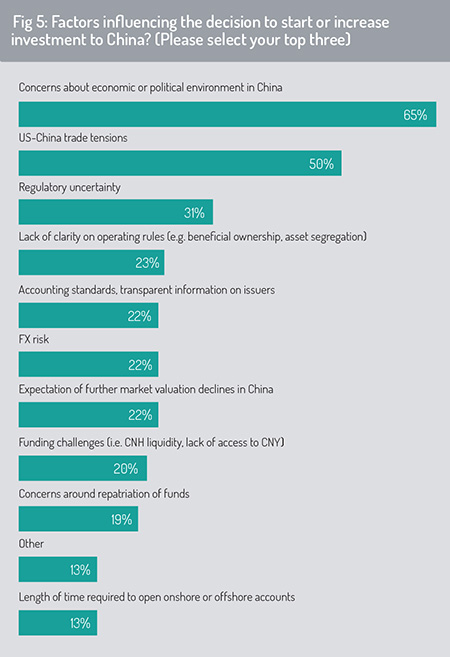

While the survey highlights a positive outlook for China-bound investment, it finds that 65% of respondents are monitoring economic and political developments closely (fig 5), both within the Greater China region and globally, to identify potential risks and opportunities these may present for their investment strategies.

Respondents also point to US-China trade tensions (50%), regulatory uncertainty (31%) and the need for transparent financial reporting and accounting standards (22%) as primary factors that are shaping their decisions about when, and how much, to invest into China.

While investors are clearly sensitive to these political, economic and regulatory risks, it is clear that respondents do not expect these to act as a significant brake on cross-border investment flows on to the mainland.

When consulting with foreign investors two to three years ago, clarity around operating rules featured prominently among the factors shaping their decision to invest in the Chinese market. Although this remains important, it now lies fourth in their priority list.

Two other factors that have slipped down this priority list are funding challenges and FX risk. With the implementation of Provisions of Cash Administration of Domestic Securities and Futures Investment by Overseas Institutional Investors by PBoC and SAFE, effective from June 6, 2020, inbound investment from overseas institutional investors (OIIs) is no longer subject to quota limitation or currency restriction. OIIs can inject foreign currency and RMB according to their investment needs. For repatriation, other than in cases of liquidation, OIIs need only submit a commitment letter of tax clearance to enable profit repatriation.

Overseas institutional investors require a flexible suite of CNY-denominated hedging instruments to manage their currency exposures in the Chinese market. Although this remains a concern for foreign investors, Chinese regulators have been taking gradual steps to improve the range of risk-management tools available – including announcements from the China Foreign Exchange Trade System (CFETS) permitting up to and including three domestic financial institutions as counterparties for FX derivatives.

Overseas institutional investors require a flexible suite of CNY-denominated hedging instruments to manage their currency exposures in the Chinese market. Although this remains a concern for foreign investors, Chinese regulators have been taking gradual steps to improve the range of risk-management tools available – including announcements from the China Foreign Exchange Trade System (CFETS) permitting up to and including three domestic financial institutions as counterparties for FX derivatives.

Investors may also apply to be a CFETS member, enabling them to trade directly in the inter-bank FX market for CIBM Direct (effective from February 1, 2020). For Bond Connect, CFETS announced changes on September 24, 2020, which allow Bond Connect investors to conduct FX conversion and hedging with up to and including three Hong Kong Special Administrative Region (HKSAR) Settlement Banks.

Investors have also focused on the need for adequate CNY liquidity to fund growth of transaction volume through onshore channels and CNH liquidity to support growth in trading volumes through Stock Connect and Bond Connect (see below). Prior to China’s entry into the MSCI Emerging Markets equity index from May 2018, respondents were concerned about the availability of CNH liquidity to cover spikes in Stock Connect activity during index rebalancing (discussed further in the next section). Having seen this transition pass with no major liquidity shortage, funding challenges have dropped down respondents’ priority list in this 2020 survey.

Additionally, speed and ease of account opening have been longstanding priorities for foreign investors wishing to increase their exposure to China and for financial intermediaries acting on their behalf. It is noteworthy that this factor has fallen to the foot of this priority list, highlighted by just 11% of respondents. Whereas the registration, quota approval and account opening procedures for QFII applications may have taken several months in times past, the Chinese authorities have streamlined application and account opening procedures for QFII, RQFII (QFII and RQFII are known as Qualified Foreign Investors, QFI, after November 1, 2020) and CIBM Direct investments.

Moreover, Stock Connect and Bond Connect, providing access to mainland investments via Hong Kong, typically offer registration and account opening in weeks rather than months. For example, Standard Chartered is currently getting Bond Connect accounts up and running within two to four weeks, whereas at the beginning of 2020, this might have taken up to two months.

© 2020 funds europe