The next section has been included in the survey for the past two years. This analyses which companies will be the most valuable partners to asset management firms in managing business innovation and which will be the primary sources of disruption to the investment funds industry.

The largest group of respondents, representing 38% of answers received, said that the growth of distribution through industry fund platforms will be the most important driver for changes in distribution and marketing strategies. Over two decades, we have seen the rise of fund platforms such as Allfunds, Cofunds, FundsNetwork and Charles Schwab Global, establishing an extensive fund distribution network and extending access to a wide universe of investment funds and ETFs.

A slightly smaller group (representing 31% of responses) told us that the involvement of technology companies – potentially including ‘BigTech’ such as Google and Microsoft – will be a major promoter of change in this sector. A number of global technology firms have been establishing strategic relationships with firms in the financial sector, deepening their understanding of the financial ecosystem and how its technology requirements are evolving (fig 11).

In focusing attention on which companies are most likely to disrupt asset managers’ business models, respondents highlighted online retailers such as Alibaba and Amazon as the most likely source of disruption – this group of companies displacing large technology companies such as Google and Microsoft from the top of the weighted-average rankings (fig 12).

Given the huge network that online retailers have established for merchandise distribution, as well as the expertise that they can offer in distribution supply chain management, financial payments and platform technology, these retailers are now realising the opportunity to extend their service coverage into the funds distribution sector. For example, Ant Financial Services Group, an affiliate of the Chinese Alibaba Group, announced in June 2019 that its wealth management platform, Ant Fortune, had established collaboration with 80 asset management companies to apply its artificial intelligence technology to deliver a tailor-made wealth management service.

According to Ant Financial, this will apply its algorithms and knowledge of user behaviour to assist brokerages, asset managers, insurers and private equity firms to target investors more effectively through Ant Fortune. Ant Financial indicates that the Yu’e Bao money market fund now has more than 600 million users managing cash balances through its mobile payments channel Alipay.

Survey respondents also highlight the likelihood that disruption will come from other new entities that we do not know about yet.

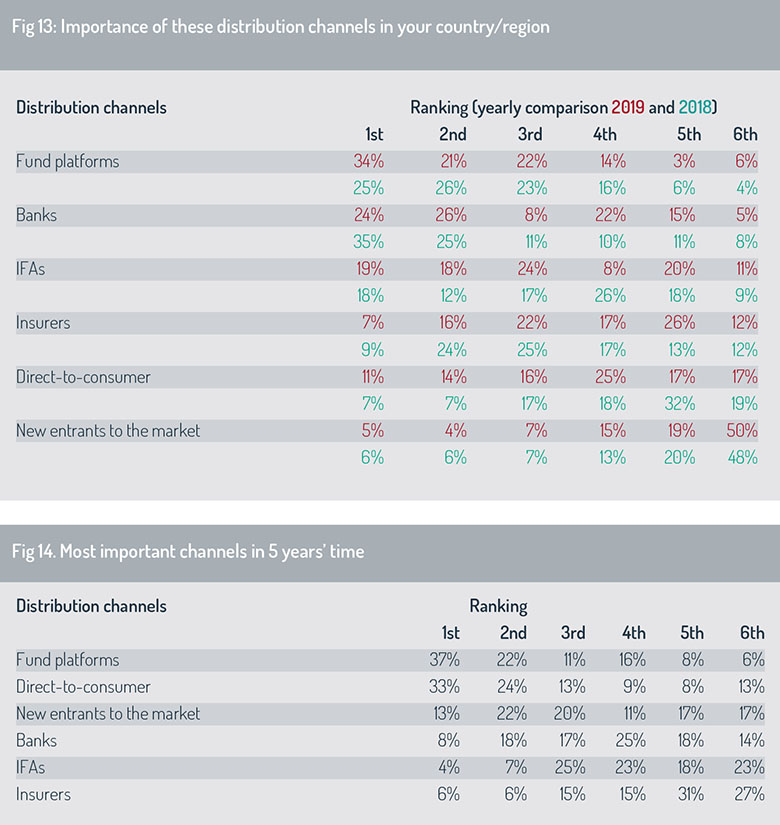

Distribution channels

In this section, the survey evaluates how channels that asset managers are using to sell their fund products are evolving over time. We asked respondents to rank the importance of key distribution channels in the country or region. Respondents highlighted that distribution sales via fund platforms are gaining importance in the EU and UK, rising to the top of the weighted-average rankings from second position last year (fig 13).

Third-party distribution of fund products via fund platforms has assumed rising importance over a number of years, potentially eroding the position of independent financial advisers as the UK’s dominant distribution channel to retail investors in the wake of RDR. In the EU, banks continue to play an essential role in driving sales to retail investors, although third-party distribution via fund platforms is also making headway in some jurisdictions.

Direct-to-consumer distribution currently ranks near to the foot of the rankings across EU and UK respondents as a whole, but respondents indicated they expect this channel to gain currency in the UK market over the coming four to five years (fig 2).

This point is confirmed in fig 14, where fund platforms and direct-to-consumer channels are expected to establish themselves as the dominant distribution channels for EU and UK investors in the coming five years. Respondents also highlighted the potential for new entrants to the market – perhaps distribution channels linked to online retailers highlighted in fig 12. This reconfiguration of customer purchasing preferences is expected to result in a decline in distribution through bank channels in the EU, and gradual erosion in the position of the IFA as a core intermediary steering investment fund sales to UK retail investors.

Distributed ledger

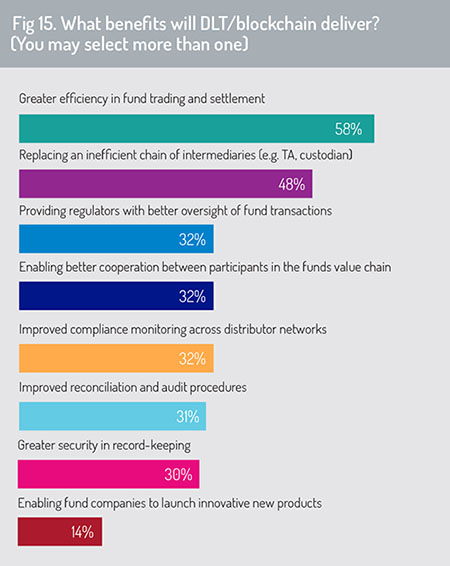

In commenting on fig 4, we outlined potential benefits that distributed ledger (blockchain) technology may deliver to asset managers and their investors. In asking industry participants to identify which potential benefits of DLT will be most important to the investment funds industry, nearly 60% of respondents indicated that they expect DLT implementation to deliver greater efficiency in fund trading and settlement (fig 15).

The survey predicts that greater use of DLT will also result in a redesignation of responsibilities along the fund value chain – resulting in potential displacement or “disintermediation” of some financial intermediaries (for example, custodians and transfer agents) from the post-trade process as a blockchain-based book of record is deployed more widely.

The survey predicts that greater use of DLT will also result in a redesignation of responsibilities along the fund value chain – resulting in potential displacement or “disintermediation” of some financial intermediaries (for example, custodians and transfer agents) from the post-trade process as a blockchain-based book of record is deployed more widely.

More broadly, extension of DLT applications is likely to support more efficient regulatory oversight and compliance reporting, providing regulators with a better overview of fund transactions, facilitating improved cooperation between participants in the funds value chain and enabling asset management firms to strengthen compliance reporting across their distributor networks – for example, in meeting the product governance components of the MiFID II directive.

In exploring where the application of distributed ledger technology will deliver the most obvious benefits to investors in fund products, the survey finds that the dominant gain will be experienced through a reduction in transaction fees. This mirrors the result generated in the 2018 survey, when 44% of respondents also indicated that the primary benefits of DLT implementation will be through a lower aggregate cost of trading.

It is apparent from these results that respondents currently rank the cost-efficiency benefits of blockchain – and also potential improvements in client service – above the risk-management benefits that DLT may provide through a lower risk of record-keeping errors or provision of a safer investment environment.

Breaking these results down by respondent type, we find that 47% of respondents from the distributor community and 39% of respondents from the fund administrator community believe that the use of DLT will result in lower transaction costs (but just 13% of respondents from the fund manufacturer segment said so). In contrast, just 16% of fund administrator respondents and only 7% of distributor respondents believe that the primary benefit from DLT application will come through lower risk of record-keeping errors.

Fund manufacturer respondents said that the primary benefits of DLT would come through improved client service (25%) and by facilitating development of new investment products (25%).

©2019 funds europe