The FTSE Russell indices tracked by Lyxor lead to fewer specific risks, fewer valuation and crowding issues and more consistent performance.

2016 promised much for active managers to exploit – dispersion, uncertainty and greater differentiation between countries, companies and sectors. But for many, this brought a challenge too great, with style and sector rotations eluding all but the best managers. 2017 promises more of the same, albeit some significant hurdles have already been overcome.

Hard to beat for all but the very best

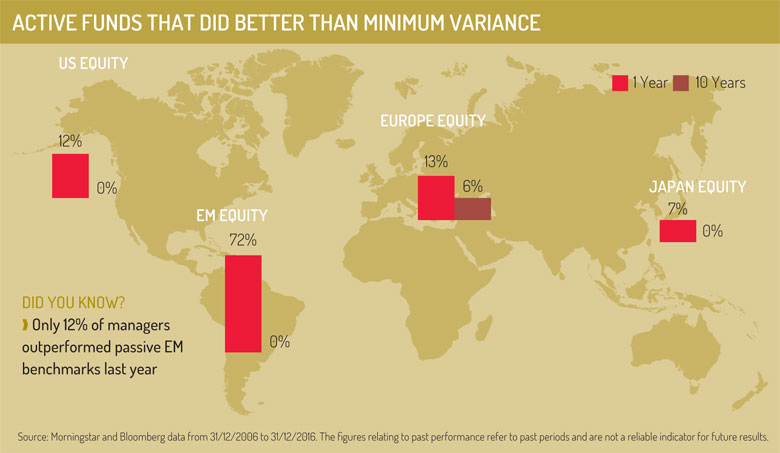

Our annual deep dive into 3,800+ active funds tells us only 28% of active managers outperformed their benchmarks last year, marking a significant decline on the year before1. It also told us that fewer still managed to outperform minimum variance benchmarks.

In fact, only 13% of active large-cap European equity funds outdid the FTSE Europe Minimum Variance Index. Only 5% have done it over ten years1. Benchmarks like the FTSE Minimum Variance Indices:

• Offer more attractive risk/return profiles over the short and long term

• Have a Sharpe ratio 1.7 higher than that of the average active fund over 1 year and 2.4 higher over ten years

• Outperformed 89% of active managers in our US, Europe and Japan universes in 20161

• Outperformed 98% of active managers in those universes over the last decade1

Building better portfolios

The FTSE Russell minimum variance indices work because they are that little bit different. Most traditional volatility reducers tend to concentrate on a relatively narrow number of predominantly large-cap stocks. But why would you add one risk (concentration) to replace another, especially with mid-caps and broad indices having proven less volatile than ultra-liquid large-caps over the last few years?

The FTSE Russell indices we track adhere to some of the strictest diversification targets in the industry, so you hold at least twice as many stocks as you would in any of the other similar strategies available today. It leads to fewer specific risks, fewer valuation and crowding issues and more consistent performance – because you don’t lose touch with the beta of the market in the way other strategies can.

Dealing with downside

The crux of the matter is of course risk reduction. Because the strategy takes volatility, correlations and diversification targets (retaining 55%-70% of original universe) into account, it tackles risk in a way few other volatility reducers can. Maximum stock and sector weights of 1.5% and 20% respectively ensure risk is spread further across the portfolio. Over the last ten years, our European strategy has for example reduced risk by just over 24%1.

Up, up & away

Greater diversification comes with another, less obvious, benefit. Holding more stocks means expanding the opportunity set to include smaller large-caps and some mid-caps so, when markets rise, FTSE’s strategy tends to capture more of those gains than any of its competitors. Indeed, in five of the last nine up years, it has led the way. Should Europe’s improving fundamentals finally get the attention they deserve, but tail-end risks still trouble you, this could be your play.

Choosing minimum variance doesn’t mean compromising on performance. Our European strategy has delivered annualised excess return of 2.7% vs. the benchmark over the last ten years. That’s a best-in-class result2.

Having differences is good

The index, which is rebalanced semi-annually, throws up some natural differences between the parent (FTSE Developed Europe) and the minimum variance index.

It’s no surprise sectors like banks, oil & gas and automobiles are significant sector underweights, but it might come as a surprise that a relative equity ‘safe haven’ like Germany is the second-largest underweight at the country level.

Rule (out) Britannia

By far the biggest underweight, however, is the UK. We should not overlook the Brexit burden and the way UK companies’ earnings could be affected. We believe the complacency we are seeing today is misplaced. Deal or no deal, Brexit will be a battle. The FTSE Russell strategy has less exposure to the UK than any of its peers.

Improve your long-term results

Adding the FTSE Russell strategy to your portfolio could lead to better outcomes. Take a portfolio that’s split equally between European bonds and equities – replacing 30% of the equity allocation with our strategy would have reduced volatility by 12.2% while delivering excess cumulative returns of 7.5% over the last decade3.

Despite the Lyxor FTSE Europe Minimum Variance UCITS ETF being the cheapest of its kind (TER of just 0.20% as at May 23, 20171), you get an awful lot for your money.

Disclaimers: 1, 2 & 3 Lyxor/Bloomberg. Data from 30/03/07 to 31/03/17 unless otherwise stated. Past performance is no guide to future returns. Opinions expressed are as at May 2017. This communication is for professional clients only.

This document is for the exclusive use of investors acting on their own account and categorised either as “Eligible Counterparties” or “Professional Clients” within the meaning of Markets In Financial Instruments Directive 2004/39/EC.

This document is of a commercial nature and not of a regulatory nature. This document does not constitute an offer, or an invitation to make an offer, from Société Générale, Lyxor International Asset Management or any of their respective affiliates or subsidiaries to purchase or sell the product referred to herein.

We recommend to investors who wish to obtain further information on their tax status that they seek assistance from their tax advisor. The attention of the investor is drawn to the fact that the net asset value stated in this document (as the case may be) cannot be used as a basis for subscriptions and/or redemptions. The market information displayed in this document is based on data at a given moment and may change from time to time. The figures relating to past performances refer or relate to past periods and are not a reliable indicator of future results. This also applies to historical market data. The potential return may be reduced by the effect of commissions, fees, taxes or other charges borne by the investor.

Lyxor International Asset Management (Lyxor ETF), société par actions simplifiée having its registered office at Tours Société Générale, 17 cours Valmy, 92800 Puteaux (France), 418 862 215 RCS Nanterre, is authorized and regulated by the Autorité des Marchés Financiers (AMF) under the UCITS Directive and the AIFM Directive (2011/31/EU). Lyxor ETF is represented in the UK by Lyxor Asset Management UK LLP, which is authorised and regulated by the Financial Conduct Authority in the UK under Registration Number 435658.

©2017 funds europe