Senior company executives answer questions on business development, regulation and the future of the industry.

BNP PARIBAS SECURITIES SERVICES

Executive Q&A: Jean Devambez, global head of products and solutions, asset and fund services, BNP Paribas Securities Services

What are your operational concerns at present affecting the growth and development of your business?

We are still experiencing growth in our business. So our focus is on managing this growth while coping with a fast-changing environment. We have built specific programmes from a technology and client-servicing standpoint in order to focus on our delivery while managing this growth.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Ucits V is a well-known regulation and we have been working for a long time with our clients on its implementation.

Our leading position allows us to leverage best practices across locations and we don’t see any major gap or issue in the implementation process.

MIFID II is a much more complex topic. First of all it covers many different areas and there are still open questions.

As far as client preparation is concerned, we see a heterogeneous situation in the market specifically on cost and charges, reporting and around product governance and suitability.

Over the next five years, how do you see the asset servicing sector changing?

Over the next five years, some key changing factors will be:

• the search for global solutions able to support new asset managers’ and investors’ operating models

• new technologies within the development of digital solutions increasingly focused on data

• the continuous regulatory pressure resulting in more transparency and a growing focus on compliance.

All this will have a significant impact on our business and will bring new opportunities to develop our services around data management, compliance, risk monitoring, outsourcing and fund distribution.

More than ever, technology with the right set of skills (data but also new technologies and design) and asset safety will be key for success.

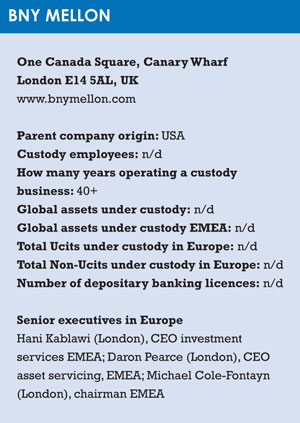

BANK OF NEW YORK MELLON

Executive Q&A: Daron Pearce, chief executive, asset servicing Emea, BNY Mellon

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

Our operational team’s focus is to maintain service quality whilst improving efficiencies and reducing costs in this challenging market. The benefits of detailed data-based analytics of current performance can help, but innovation may be limited in the short term when the regulatory programmes we must run are added into the equation.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Ucits V, CRS and MiFID II are the top three priorities for our clients. We believe our clients, having largely addressed Ucits V, are now focusing on MiFID II given its revised implementation date. However, its impacts are broad, cutting across organisations and varying according to clients’ business models.

For example, UK-centric businesses, having dealt with MiFID I and RDR, may have less to address than EU clients with larger distribution networks. As a directive, MiFID II also has national interpretations to consider, meaning work can only progress so far at this stage.

Over the next five years, how do you see the asset servicing sector changing?

There are many uncertainties in markets at the moment, from Brexit and stability in the EU to the long-term impact of regulations, the potential impact of fintechs and digital disruption and also economic variables such as debt, leverage and interest rates. At BNY Mellon, we feel we are well placed to support our clients in managing through all these challenges and to facilitate their technology transformation and digitisation plans in this challenging market.

CACEIS Executive Q&A: Pierre Cimino, managing director, Caceis Bank Luxembourg, member of Caceis executive committee

Executive Q&A: Pierre Cimino, managing director, Caceis Bank Luxembourg, member of Caceis executive committee

What are your operational concerns at present affecting the growth and development of your business?

Downward pressure on fees along with ‘zero defect’ demands have been a constant feature of our business, and finding the balance between making cost savings and maintaining quality is one of the biggest operational challenges we face.

The sheer volume of mandatory regulatory reports that need to be generated within the framework of Priips, MiFID and Emir also put a heavy strain on operational resources.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Clients are well prepared for Ucits V as it’s for 2016 and is not revolutionary [ground already covered by AIFMD]. MiFID II implementation is further off (early 2018), and it represents far more than a simple upgrade, so clients are perhaps currently less well prepared. Nevertheless, through regulation-focused newsletters and client visits, we ensure they have the necessary information to prepare for compliance.

Over the next five years, how do you see the asset servicing sector changing?

The biggest changes to the industry will be driven by financial technology, across applications, processes, products and business models.

Asset servicing is starting to look at the new opportunities in distributed ledger technologies, like blockchain.

It is increasingly benefiting from ongoing digitalisation advances that increase the efficiency and accuracy of processes.

Mobile technologies enable asset servicers to handle the entire investor subscription process, and finally, data analytics is unlocking the marketing potential of the data an asset servicing provider holds.

HSBC SECURITIES SERVICES

Executive Q&A: John Van Verre, head of global custody, HSBC Securities Services

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

HSBC is delivering a significant two-year investment programme designed to realise material sustainable operational efficiencies for the benefit of customers impacted by competitive margin pressures.

We continue to connect clients with new investment opportunities in China, e.g. access to the China interbank bond market and to the new Shenzhen-Hong Kong Stock Connect model once open.

It will take time to understand the true impact of the UK’s Brexit decision. Firms are using scenario analysis to assess potential operational impacts and to formulate contingency plans.

We expect clients to leverage our existing footprint in the UK and Europe to successfully implement their plans.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Ucits V represented a natural extension of AIFMD, simplifying complexity of implementation. It has materially improved investor protection by extending the obligations of depositary banks.

The MiFID II one-year compliance delay was welcomed by clients. Changes to reporting, research, trading venues and distribution remain their key implementation priorities.

Over the next five years, how do you see the asset servicing sector changing?

We will see significant streamlining and technology investment across the value chain, alleviating competitive cost pressures and simplifying platform distribution.

Asset gathering will pivot to Asia, requiring local market presence, capability and operational scalability. International manufacturers will demand globally consistent operating and client service.

JP MORGAN

Executive Q&A: Christopher Rowland, global head of custody, JP Morgan

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

• Data strategy – our business growth requires the ability to quickly extract data and provide business insight

• Automated control process – reduce risks in processing and connectivity to agents and markets

• Global operating and service model – our clients’ global expansion drives demand of global consistent service, regional timezones support and in-depth market knowledge.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Increasing regulatory scrutiny burdens clients, depository, and custodians. Client look up to industry leadership for guidance in tracking these new regulations.

JP Morgan is working with its clients to address additional obligations and oversight duties imposed on custodian and depository on the back of Ucits V.

MiFID II has been the topic of discussion with clients recently. However, due to lack of clarity on a number of fundamental aspects of MiFID II, clients are waiting for further details from regulators.

Over the next five years how do you see the asset servicing sector changing?

Securities services industry is undergoing a dramatic change with a need for providers who have the scale to deliver a fully integrated product set across jurisdictions. JP Morgan has evolved to facilitate client investment decisions, distribution strategies, harmonise global operations and drive technological innovations while maintaining highest level of assets safety. While we cannot predict all the effect onto the securities service industry, JP Morgan is focused on identifying those key changes, and adapting to them.

NORTHERN TRUST

Executive Q&A: Toby Glaysher, executive vice president & head of global fund services (Emea), Northern Trust

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

As asset managers are compelled to refocus on their core business, given margin pressures, there is an increased demand for a full asset servicing solution. This is leading to a greater outsourcing of functions such as middle offices and derivatives processing, which we are supporting. Managing and providing data to clients with the frequency and format requested is also a key focus.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

The delay to MiFID II has undoubtedly given all a helping hand in terms of preparedness. However, some key aspects remain uncertain, meaning there is a sense of hesitation across the industry. Providing clarity comes soon, those who continued their MiFID II project efforts should be well placed to implement the change required.

Over the next five years, how do you see the asset servicing sector changing?

Asset managers will continue to evolve their business models across traditional and alternative sectors. This will drive asset servicing firms to support an increasingly broad spectrum of fund structures and asset types. We also anticipate:

• Growing use of unitised funds rather than segregated mandates, coupled with the continued attractiveness of tax transparent funds

• More asset owner consolidation leading to bigger asset pools and use of fund investment platforms to launch product quickly and efficiently

• Emerging technologies, such as blockchain and robotics, becoming more mainstream

• Changing distribution models driven by regulatory and political changes, such as MiFID II and Brexit.

PICTET & CIE

Executive Q&A: Claude Pech, global head of business development and client relationship management, Pictet & Cie

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

Ongoing regulatory issues – mainly in the EU – have given rise to operational concerns in the asset servicing segment. These include Emir extension, Priips, CRS for transfer agents, etc. The situation in 2016 is similar to The Myth of Sisyphus (new regulations are introduced only to be followed almost immediately by more new ones). Even though our business is essentially client-centred, we paradoxically invest more to comply with regulatory requirements (which are perceived as a burden rather than a benefit to clients) than we do on improving client service.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

These two issues are not of concern to us. Ucits V is now behind us and merely affects service providers rather than fund promoters.

MiFID II will affect fund distribution. However, in our view, asset managers and distributors are quite well prepared. In our capacity as a service provider, we have adapted to this new paradigm by accommodating the needs of our clients.

The fact that calculation of trailer fees may disappear is certainly no bad thing for us. All service providers will agree that this has been an inefficient area of service for a large number of years.

Over the next five years, how do you see the asset servicing sector changing?

There are two elements impacting this sector: higher expectations from service providers on the part of clients and at the same time pressure on fees (“we want more for less”).

In fact, I still see room for further concentration with two remaining segments: the big service providers with a factory approach and the smaller players that can provide tailor-made services. Smaller in this case is not really small, as providers still need to be of a reasonable size to be credible and profitable in this business. Consequently those that will disappear will be the ones that have not clearly defined their strategy (either industrial or tailor-made), or those that do not have the critical mass to be economically viable.

A three-tier system of ‘economy class’, ‘business class’ and even ‘first class’ makes sense in the asset services sector as well.

RBC INVESTOR & TREASURY SERVICES

Executive Q&A: Sébastien Danloy, chief executive, RBC Investor Services Bank

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

RBC I&TS has an unwavering commitment to operational risk management and efficiency. Our focus is on delivering excellence, supporting our clients, and meeting regulatory obligations. RBC I&TS’s multi-year technology strategy is designed to improve client satisfaction and is integral to business development while driving operational efficiency and enhancing operational risk management. Our transformational approach to technology places our clients at the centre of activities through ongoing engagement and dialogue to align with their requirements.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Asset managers increasingly face stricter regulatory requirements including Ucits V and MiFID II and are seeking support. It is crucial for providers to align with clients’ priorities, and adapt to evolving regulation and market conditions. As a leading provider focused on industry regulation and market best practices, RBC I&TS is well prepared to support clients.

Over the next five years, how do you see the asset servicing sector changing?

Change will likely be driven by ongoing market shifts, regulatory developments, and financial technologies impacting on how providers serve clients, plus clients’ focus on efficiency, risk, costs, and regulatory obligations. Continuous transformation in technology will be vital to meeting clients’ evolving needs. Clients will be able to take advantage of RBC I&TS’s strength and stability, specialist expertise, regulatory support and agile approach to technology.

SEB BANK

Executive Q&A: Göran Fors, deputy head of investors services, SEB

Over the next five years, how do you see the asset servicing sector changing?

Over the next five years, how do you see the asset servicing sector changing?

The post-trade area is going through enourmous changes and the industry is facing a lot of challenges.

First of all we have developments that affect in many various parts of the financial sector. Cyber crime is one of the most worrying areas today and could potentially harm developments and make cross-border activities more difficult.

The other major change is distributed ledge technology/blockchain. The developments in this space could really mean a paradigm shift in how we work in the space of post-trade.

Even if the changes will be more limited, we will definitely see a lot of services and processes being handled in a technology that we today have limited competence of.

In the securities post-trade area we have a lot of developments that will mean tremendous challenges – but also opportunities for those that can handle the new world.

Infrastructure is changing driven by T2S, implementation of new IT systems and all of it being fuelled by regulatory changes like CSDR.

Regulatory changes in general are also a very big part in many other areas of the post-trade area. This means that we will have to invest in technology and knowledge.

Risk management is the third pillar in the post-trade area and will mean that investors will have to be very careful when they choose providers –not that many custodians will be able to support their clients in this area or live up to the demands from regulators.

Cost reduction will continue to be an important part of the post-trade world and will, in combination with the aforementioned areas, mean that a limited number of providers will survive on the European scene.

SOCIETE GENERALE SECURITIES SERVICES

Executive Q&A: Olivier Renault, country manager, SGSS Luxembourg

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

Our success will increasingly depend on technology and data analytics to provide a more client-centric experience. Our Beacon initiative will digitise every aspect of our business. Our aim is to simplify our core business processes, improve client service, foster the creation of new insights and increase the accuracy of portfolio information. We have also raised the bar on client engagement and are deepening relationships with our clients to deliver integrated, innovative and impactful solutions.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Over State Street’s long history, periods of significant regulatory change provide the best opportunities to partner with our clients to solve the challenge. We work closely with clients to develop new solutions that enable efficient governance and transparency across diverse portfolios. We have created a European regulatory reform programme to address Ucits V and MiFID II and how they affect our business and clients.

Over the next five years how do you see the asset servicing sector changing?

Significant changes are already taking place – particularly with big data. We are seeing the power of data impacting how asset managers invest and, in turn, how back and middle office providers address their clients’ reporting and information needs. Data management and gathering insight from data is one of our clients’ biggest challenges. We see a new generation of (risk) data analytic tools providing more advanced insights in real-time becoming an increasingly important competitive advantage.

STATE STREET

Executive Q&A: Jeff Conway, chief executive officer, Europe, Middle East and Africa, State Street

What are your operational concerns at present affecting the growth and development of your business?

What are your operational concerns at present affecting the growth and development of your business?

Our success will increasingly depend on technology and data analytics to provide a more client-centric experience. Our Beacon initiative will digitise every aspect of our business. Our aim is to simplify our core business processes, improve client service, foster the creation of new insights and increase the accuracy of portfolio information. We have also raised the bar on client engagement and are deepening relationships with our clients to deliver integrated, innovative and impactful solutions.

Changing regulation is affecting the industry – how well prepared are clients for Ucits V and MiFID II?

Over State Street’s long history, periods of significant regulatory change provide the best opportunities to partner with our clients to solve the challenge. We work closely with clients to develop new solutions that enable efficient governance and transparency across diverse portfolios. We have created a European regulatory reform programme to address Ucits V and MiFID II and how they affect our business and clients.

Over the next five years how do you see the asset servicing sector changing?

Significant changes are already taking place – particularly with big data. We are seeing the power of data impacting how asset managers invest and, in turn, how back and middle office providers address their clients’ reporting and information needs. Data management and gathering insight from data is one of our clients’ biggest challenges. We see a new generation of (risk) data analytic tools providing more advanced insights in real-time becoming an increasingly important competitive advantage.

2016 funds europe