Funds Europe, in association with RBC Investor & Treasury Services, hosted an event to discuss how one of the biggest political decisions since the Maastricht Treaty will affect the asset management industry. Speakers from RBC Capital Markets, Unigestion, Investec Asset Management and Lothbury Investment Management took part.

British voters will decide whether to remain in the EU on June 23 and Funds Europe and RBC Investor & Treasury Services recently held an event: ‘Brexit: What could it mean?’ to hear views from the funds industry.

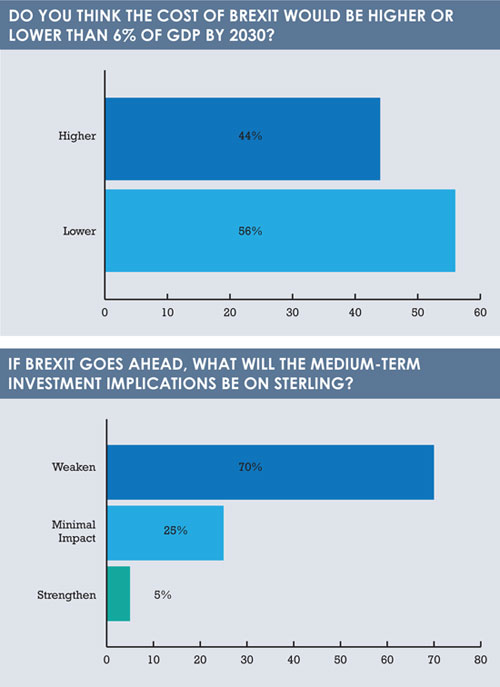

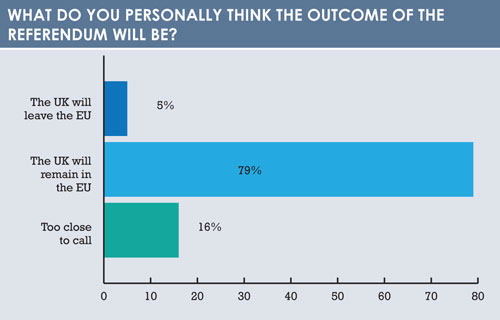

Four industry figures spelled out possible scenarios in the event of the ‘Leave’ campaign winning, and the audience expressed their views through a number of polls to do with economics and investment (see bar charts).

Ahead of the first poll – concerning how much a Brexit would cost the UK as a percentage of GDP – Sam Hill, senior UK economist at RBC Capital Markets told the audience that estimates varied widely. He noted a wide range of predictions arising from a Bank of England report on the EU referendum. One pundit (presumably Eurosceptic) thought that the level of UK GDP would be 5% higher if outside the EU. Another effectively took the view that UK GDP would shrink by 20%. The report also contained many other answers, Hill said.

His main concern was that a Brexit could turn into a “SMexit” – an exit from the EU’s single market. “Restrictions to the single market might restrict the level of business the UK does with the EU if there was to be a Brexit,” he said. This would be a challenge for the UK’s financial services industry as it could jeopardise the passporting freedom it currently enjoys to be able to provide services to the rest of Europe.

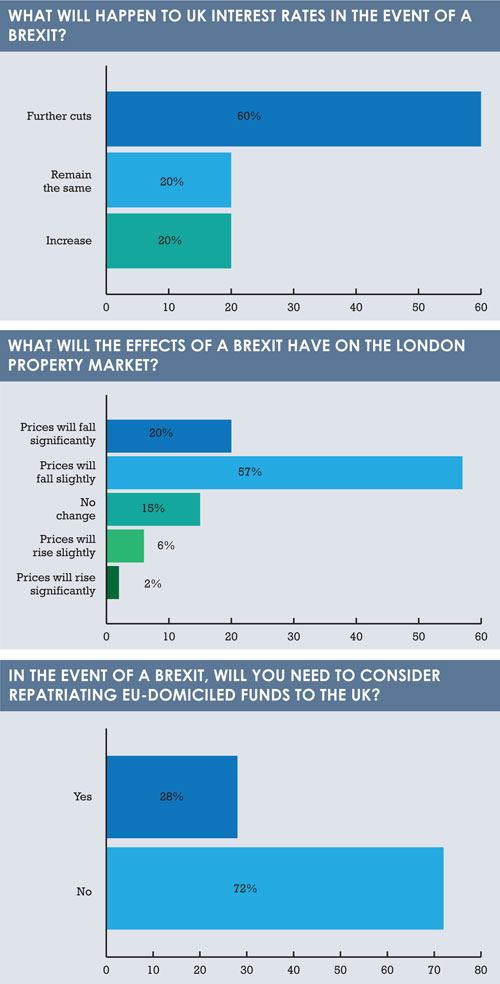

The audience was then asked what impact a Brexit would have on sterling. Hill is not optimistic about the impact on the UK’s currency, although as a caveat, he did say it would depend on what form the Brexit takes. There are scenarios where it might be necessary for the Bank of England to cut interest rates and even engage in some asset purchases of UK gilts. This would drive sterling even lower and if the currency depreciated 10%-15%, the result would be a brief spike in inflation.

The audience was then asked what impact a Brexit would have on sterling. Hill is not optimistic about the impact on the UK’s currency, although as a caveat, he did say it would depend on what form the Brexit takes. There are scenarios where it might be necessary for the Bank of England to cut interest rates and even engage in some asset purchases of UK gilts. This would drive sterling even lower and if the currency depreciated 10%-15%, the result would be a brief spike in inflation.

Philip Saunders, co-head of multi-asset at Investec Asset Management, another one or our panellists, suggested the UK is getting ahead of itself in terms of its global economic relevance. He said that while Brexit might matter to the British, more important things are happening on the world stage, such as the Federal Reserve’s interest rate policy, which has altered dramatically since December. While markets were expecting four hikes this year, it looks like the US may only manage two.

Concern over China is another factor that seems to put the Brexit impact in perspective, as markets continue to worry about the world’s second-largest economy suffering a hard landing and the impact of it on the global economy. There are also concerns about commodity prices, despite their recent rally. This is having a big impact on emerging markets, especially oil producers.

Saunders believes investors can strive to negate the impact of a Brexit by using globally diversified portfolios. “Those with regional bias to UK assets should be worried,” he said.

Given the relatively small amount of assets in the UK, many investors will have global portfolios – and if they wanted to hedge against the negative impacts of a Brexit and market volatility, then they might short European assets.

“The general unity of views is that it [Brexit] will be pretty bloody in the short term,” said Saunders, adding it would be best for portfolio managers to keep politics at arm’s length.

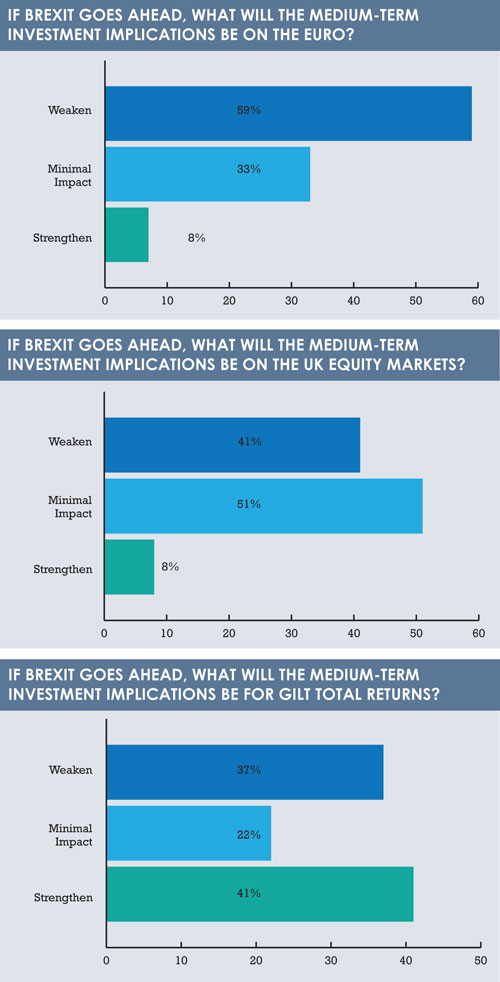

Luca Simoncelli, investment manager, cross asset solutions at Unigestion, another of our speakers, identified three main issues stemming from Brexit: recession risk, inflationary shock and market stress. Simoncelli said a recession could happen if consumer confidence was shaken by higher inflation, which would in turn be brought on by sterling depreciating markedly.

Market stress signals would be heightened volatility, tighter financial conditions with wider credit spreads and, most likely, less liquidity in the market.

Simoncelli based his views on how he constructs his multi-asset portfolios. He said that when building such portfolios, his focus is on the macro risk, which means identifying macro regimes that define different behaviour in different asset classes and risk premia.

“The price of hedging against falling sterling is becoming more expensive,” he said, adding this was especially the case against the dollar. Simoncelli suggested he would focus on hedging against the euro, which would be cheaper.

His opinion on the UK equities market was that small and mid-cap firms would suffer more from a Brexit than their large-cap peers. This is because the smaller companies universe relies more on trade with Europe for revenues, whereas the large-cap firms derive more revenue from outside Europe.

One thing that may cause the most concern is house prices, and Simon Radford, chief executive of Lothbury Investment Management, was present to allay any fears on the matter. Transactions reached £66 billion last year, with 50% of investment coming from overseas investors. In the first quarter of the year, transactions were down 20% to £13 billion. However, Radford said: “Although activity is down it’s still substantial and 50% of those purchases are from overseas investors.” He added that when supply increases, there could be a reduction in rents.

One thing that may cause the most concern is house prices, and Simon Radford, chief executive of Lothbury Investment Management, was present to allay any fears on the matter. Transactions reached £66 billion last year, with 50% of investment coming from overseas investors. In the first quarter of the year, transactions were down 20% to £13 billion. However, Radford said: “Although activity is down it’s still substantial and 50% of those purchases are from overseas investors.” He added that when supply increases, there could be a reduction in rents.

The audience heard interesting scenarios, but however the British electorate votes, it is likely that asset management would be able to cope with the Brexit.

©2016 funds europe