Small changes in inflation or interest rates can have a significant impact on pension funds, given the long-term nature of their liabilities. Stefanie Eschenbacher finds they look to inflation-linked assets, despite falling inflation.

Inflationary pressures in Europe have eased in recent months, at least according to the European Central Bank (ECB), making way for even more stimulus.

Eurozone inflation is forecast to stay below, but close to, 2% over the medium term, giving the bank more scope for interest rate adjustments to stimulate the economy without the risk of immediately stoking significant inflation. The ECB cut the main interest rate to below 1% for the first time in July.

Meanwhile, the Bank of England has held its interest rate but increased the level of quantitative easing by £50 billion (€63 billion) to £375 billion amidst fears that the country’s double-dip recession may last into autumn.

Elsewhere, the People’s Bank of China cut its benchmark rate by 31 basis points to 6%. It was the second cut in less than a month and suggests the world’s second-largest economy may have slowed down more than previously thought.

Inflation fears persist

Given the unprecedented amount of money central banks have already pumped into the world economy, however, many investors remain concerned about the potential for inflation to emerge as this money gets spent.

Even small changes in inflation or interest rates can have significant impacts on pension funds because of the long-term nature of their liabilities. It is no surprise, then, if inflation is a key influencer of investment trends.

The latest European Asset Allocation Survey, by Mercer Investment Consulting, found that 15.1% of European pension schemes and 24.8% of UK pension schemes were planning to increase their allocations to inflation-linked assets over the next year. Mercer recently surveyed more than 1,200 European pension funds with assets of €650 billion.

Also seeing this trend is Peter Martin, head of manager research at JLT Benefit Solutions. “We have seen a wider and increased use of both index-linked gilts and swap-related products,” he says.

“Clearly, this depends on an individual fund’s circumstances and their attitude towards risk and their sensitivity to inflation. But, in general, we would expect this trend to continue and would encourage a particular focus on this area.”

However, there are challenges for investors who seek bonds for inflation protection.

De-risking of scheme liabilities has been a trend for some years. It has triggered a flight to bonds, which in turn has put pressure on bond yields, leading to widening pension deficits.

The Society of Pension Consultants calculates that if only 60% of UK pension liabilities used an inflation link, these liabilities would account for more than 400% of the long-dated inflation-linked bond market.

Factoring in deficit contributions, this shift could result in a demand for long-dated bonds of up to 12% of the overall market each year, up to 15% of the long-dated bond market and, conservatively, up to 35% of the long-dated inflation-protected bonds market.

Martin says there are other investments pension funds can potentially use as inflationary hedges, including treasury inflation-protected securities – commonly referred to as Tips – issued by the US Treasury. These have the added benefit of diversification because they are exposed to a different currency and a different type of inflation.

Particular types of property investments, infrastructure, commodities or inflation swaps are other possible solutions. Martin also points to equities and diversified growth strategies.

Dual challenge

There is also the challenge of managing market volatility. Mercer highlights that pension funds in Europe face the “dual challenge” of managing portfolio risk brought on by market volatility while identifying opportunities that will generate returns to support future liabilities.

Noel Collins, principal at the consultancy, says many pension funds are under pressure. They have become more focused on risk management and risk reduction as a result.

Noel Collins, principal at the consultancy, says many pension funds are under pressure. They have become more focused on risk management and risk reduction as a result.

“There is a lot of volatility in the market and volatility is difficult for pension funds to manage,” he says. “The regulatory environment is risk-averse, which influences asset allocation.”

Even before the crisis, pension funds have started to tighten the link between assets and liabilities.

Increasing life expectancy and funding gaps have put pension funds into difficult positions. Volatility and poor returns have created a situation where some pension schemes represent a material risk to the business.

Expensive choice

Gavin Orpin, partner at pensions consultancy Lane Clark & Peacock in the UK, says while there is demand for inflation-protection, the question is what price pension funds pay for this.

“There are significant supply and demand issues in the inflation-linked gilt market,” Orpin says, adding that pension funds need to address both interest rate movements and inflation.

Liabilities of most pension funds average at 30 years. Orpin says pension funds, therefore, need inflation-linked bonds with a maturity of 30, 40 or 50 years. But these look expensive now.

Orpin says pension funds buy them anyway because they need to match liabilities, even if this means potentially missing out on returns from more volatile asset classes.

Another problem, at least for UK pension funds, is that liabilities are linked to the consumer price index against which there are currently no linked government bonds.

Roger Gray, chief investment officer at the Universities Superannuation Scheme (USS), says his fund has incorporated a 4.5% strategic allocation to UK gilts in two steps – in early 2010 and in 2011 – funded by developed world equities.

“Real yields are now at historic lows, which discourages additional strategic allocations to inflation-linked gilts at this time,” Gray says. “In addition, given debt overhang and demographic trends, we are inclined to expect lower rather than high inflation.”

The Society of Pension Consultants warns that the mismatch of excessive demand to supply is likely to send the value of long-dated bond yields falling significantly over the next few years. This means pension fund deficits are likely to widen further.

Ultimately, pension funds will not be able to afford to fund the ever-increasing deficits exclusively through bonds so they will have to find alternative ways of de-risking their schemes.

Diversification

Ingrid Albisson, head of strategy at Swedish pension fund AP7, says inflation was more of a concern a couple of years ago. At AP7, the main focus has been on diversification.

“Modern financial theory suggests the best practice to reduce volatility is global diversification,” she says, adding that many Swedish pension funds have traditionally had a strong home bias.

The AP7, for example, once had 20% of its portfolio invested in Swedish equities. In recent years, however, this has been brought down to “just a couple of percent”, she says.

While the AP7 invests in equities, Albisson says other pension funds in Sweden have reduced their allocation from equities to fixed-income and alternatives.

Mercer’s survey found that schemes in traditionally equity-heavy markets – the main examples being the UK and Ireland – still have the largest equity weightings. Average allocations to domestic and non-domestic equities, however, have fallen over the past year.

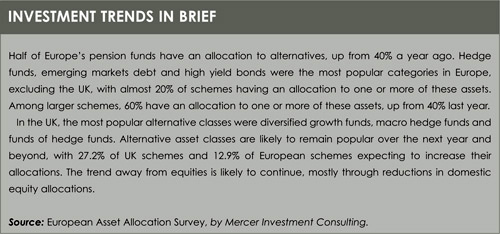

It also found that an increasingly broad range of alternative asset classes are being considered by pension plans, with 50% of schemes now holding an allocation to alternatives, up from 40% last year.

Silke Bernard, a member of the Association of the Luxembourg Fund Industry’s pension funds working group, confirms that pension funds are interestingly investing in alternatives.

Demand for alternatives is up because of poor returns and an economic – or even a legal obligation, as is the case in Germany – to generate a certain return to cope with pension obligations.

“As a consequence, [pension funds] have no choice but to go into alternative assets,” she says. “One could wonder whether the choice of alternative investments, such as real estate, might not also to some extend be driven by their resistance against inflation.”

Allocations

Gray says the USS’s medium-term allocation plans envisage substantial additional investments in infrastructure as a source of long-dated inflation-linked income streams.

The is primarily in real assets, including equities and property. Though ray says the response of such assets to inflation, particularly high inflation, is “far less assured”.

Earlier this year, the BT Pension Scheme, the largest in the UK, acquired a minority stake in Thames Water through a shareholding in Kemble Water Holdings.

The allocation increases its exposure to domestic infrastructure investments – a natural linkage to UK inflation. Frank Naylor, head of strategy for the pension scheme, says the investment “should provide predictable inflation-linked cash flows over the long term”.

Recent research from Towers Watson shows that pension fund assets already represent a third of the top 100 alternative managers’ assets globally. Pension funds’ allocations to alternatives now account for 20% of assets, up from 5% just 15 years ago.

©2012 funds europe