European equities traded close to par with the US earlier this year – unusually, as Europe should trade at a discount. Alec Harper of Axa Rosenberg believes investors bought in the hope of economic growth. He looks at what happened, and at the outlook for the asset class.

When visiting clients and investors across Europe in 2014, there appeared to be a consensus that US equities were expensive and European equities potentially offered better value, particularly for asset allocators. At the time we had to agree – taken on face value, traditional valuation metrics such as price/earnings (PE) had increased in aggregate, notably among smaller companies where the Russell 2000 Index traded at an average 30 times trailing earnings through 2014 (the S&P 500 was 17 times in comparison).

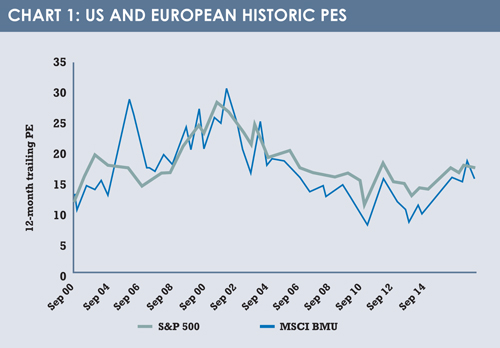

As 2015 has unfolded, the perceived ‘valuation gap’ between US and European equities was closed out altogether by May (see chart 1), which gave rise to another grave concern: European share prices were rallying without much fundamental support. At the time, we believed that investors were becoming overly optimistic about European earnings growth, with market valuations imputing an earnings growth rate of 14%. This seemed ambitious given the weak performance of the European economy since the global financial crisis.

As 2015 has unfolded, the perceived ‘valuation gap’ between US and European equities was closed out altogether by May (see chart 1), which gave rise to another grave concern: European share prices were rallying without much fundamental support. At the time, we believed that investors were becoming overly optimistic about European earnings growth, with market valuations imputing an earnings growth rate of 14%. This seemed ambitious given the weak performance of the European economy since the global financial crisis.

Prior to the recent correction, part of the strength in US equities was rooted in the performance of the economy, which ‘normalised’ quicker than other major world economies post the financial crisis. However, the result is that US equities in aggregate are more expensive now than they have been for many years. Indeed, the economist Robert Shiller (famous for his cyclically adjusted view of market valuations) recently told the media of his fears that US equities were in bubble territory.

From a European perspective, the run-up in equities seen prior to the recent correction was noteworthy. For the first time in nearly 13 years, and as chart 1 also shows, European equity markets were trading close to (and briefly above) par with the US. In our view this is important because, structurally, Europe should trade at a discount to the US. In part this is because of the ‘tech effect’; technology stocks make up some 20% of the US market, whereas in Europe they are just over 9%.

From a European perspective, the run-up in equities seen prior to the recent correction was noteworthy. For the first time in nearly 13 years, and as chart 1 also shows, European equity markets were trading close to (and briefly above) par with the US. In our view this is important because, structurally, Europe should trade at a discount to the US. In part this is because of the ‘tech effect’; technology stocks make up some 20% of the US market, whereas in Europe they are just over 9%.

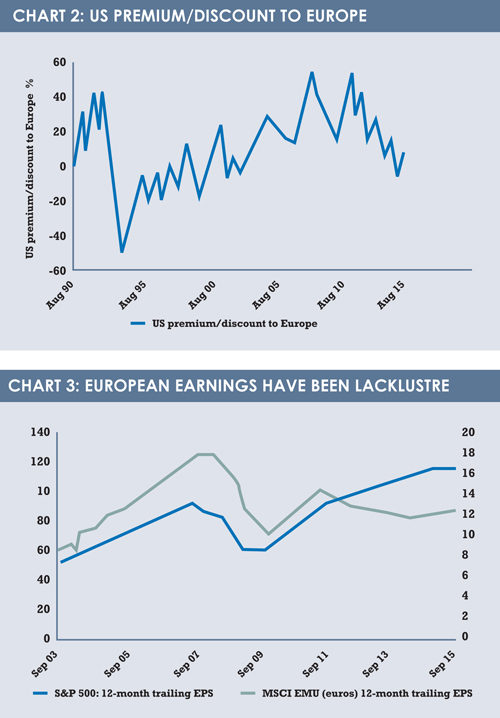

We observe that US stocks have commanded a 30-year historic average premium to Europe’s less technology-focused economy of some 10% (see chart 2).

EXCESS LIQUIDITY

What caused May’s valuation convergence, we believe, was investors buying European shares in the hope that Europe will grow, rather than because it has shown evidence of growth. In part, the European Central Bank was to blame with its asset purchase programme. Excess liquidity lifted asset prices, as it had in the US and Japan when they too undertook similar programmes, but fundamental problems persisted in Europe.

Our specific concern in May was that, prior to the volatility caused by the latest twists and turns of the Greek crisis (and the subsequent influence of China on global markets), the rate of price change in Europe was delivered in the context of flatlining earnings (chart 3). This is in stark contrast to the US, where earnings growth as a result of a strengthening economy has, to some extent, driven the valuation re-rating. Moreover, US companies on average have been more capable of converting revenues to income, with net income margins of around 6% (excluding financials and technology companies), compared with the 4% margin achieved by Eurozone companies; including the lucrative technology firms that push US margins over 8%.

Since May, two things have happened to alter the story. The first is that European equities (as measured by the MSCI EMU Index) have underperformed the US in local currency terms as the excessive exuberance shown by investors has waned, re-establishing the valuation discount relative to US equities normally ascribed to European equities. At the same time, we have started to see an improvement in aggregate European earnings, with 12-month forward growth of around 7.5% expected by consensus analyst estimates, as at the end of August. This is the first improvement in nearly five years, and the growth rate is currently higher than the US. The result is that, unlike in May, European equity valuations look more reasonable when compared to the US. It is still hard to argue that Europe is compellingly valued, but if the trend of rising earnings in Europe and slowing earnings in the US persists then this may change. Our focus is always on fundamentals, but the recent past highlights the tendency of investors to be overly optimistic or pessimistic in reaction to a changing market environment. While we are more positive on European equites, we believe that markets may be volatile in the short-term as investors over-extrapolate any positive data from Europe, as happened in May.

Alec Harper is client portfolio manager at Axa Rosenberg

©2015 funds europe