Despite the limited choice of stocks available for infrastructure managers in Latin America, the region offers some compelling investment opportunities. Stefanie Eschenbacher reports.

Infrastructure has emerged as one of the most compelling investment opportunities in Latin America, along with services, oil and gas.

Despite a global slowdown, the Economist Intelligence Unit (EIU), a research and advisory company, predicts the prospects for Latin America for 2011 and 2012 to remain solid. Argentina, Brazil and Peru are expected to grow more than 7%, and Chile, Colombia and Mexico at rates of between 4% and 5%.

As economic growth increases, so does the need for more and better infrastructure. The World Bank and participants at the recent World Economic Forum on Latin America in Rio de Janeiro, Brazil, this year, however, have warned that the region lags other emerging markets in improving its infrastructure. In the past, this has hampered economic growth and worsened poverty.

Unique, non-economic factors are creating additional infrastructure investment needs in Chile and Brazil.

Chile’s earthquake last year, the sixth largest ever recorded, destroyed large parts of the country’s infrastructure. Meanwhile, Brazil is preparing for the 2014 Fifa World Cup and the 2016 Olympic Games.

To meet the need for infrastructure, countries in Latin America have reformed their investment laws or have launched efforts to do so, says Vanesa Sanchez, a research manager at the EIU. While the regulatory framework for investing in infrastructure through public-private partnerships has already improved significantly, there is limited choice for those who want to invest in listed infrastructure companies.

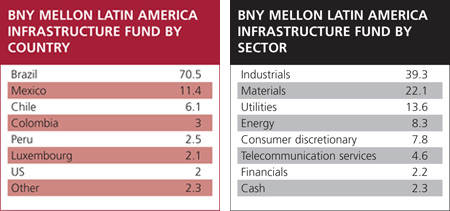

Alexander Gorra, senior strategist at BNY Arx and manager of the BNY Mellon Latin America Infrastructure fund, typically selects 30 stocks for his portfolio. With an investment universe of just 100 stocks, his choice is limited, at least compared with other sectors or regions.

A recent surge in initial public offerings, however, is likely to broaden his investment universe. In a research paper, entitled Latin America exchanges: IPO fever, the EIU lists infrastructure as one of sectors that is likely to see even more public listings.

A recent surge in initial public offerings, however, is likely to broaden his investment universe. In a research paper, entitled Latin America exchanges: IPO fever, the EIU lists infrastructure as one of sectors that is likely to see even more public listings.

Initial public offering activity in Brazil rebounded significantly in the years since the financial crisis. Foreign investors’ demand is strong and stock exchanges in the regions are making efforts to attract companies. Although Latin America’s biggest country is the leader in equity market transactions, Chile, Colombia and Mexico are catching up. One of the most important developments in recent months has been the integration of the Chilean, Colombian and Peruvian exchanges, known by its Spanish acronym Mila.

There is still a large number of family-owned firms that need to go public to maintain growth. Privatisation of government-owned companies has been another driver of expansion.

Brazil’s Petróleo Brasileiro, known as Petrobras, raised $67 billion (€50 billion) last year, making it the world’s largest initial public offering ever.

Colombia’s state-controlled Ecopetrol went public prior to the financial crisis. In Chile, the government is preparing the sale of its remaining stakes in water and sewage companies through the Corporación Fomento de la Producción de Chile. If it goes ahead, infrastructure investors will be able to buy into a sector they have traditionally found difficult to access.

Anecdotal evidence suggests the investment universe for infrastructure investment has already broadened. Prior to 2000, for example, there were no highway toll operators listed on Latin American stock exchanges. Now these are sought-after stocks.

OHL México, a toll operator in Mexico, is one of Gorra’s high conviction holdings. His second-biggest is Companhia de Concessões Rodoviárias, a Brazilian toll operator.

More than 80% of his portfolio is invested in Brazil. Not only do investors like the large, liquid stock market, they also say companies are more shareholder-friendly and their corporate governance is better.

Even though the choice of infrastructure stocks available in Latin America is limited, the region compares favourably with others. Data from Morningstar, a data provider, shows both emerging markets and global infrastructure investors have major allocations to infrastructure in Latin America.

The Macquarie Emerging Markets Infrastructure fund and the Swip (Society for Worldwide Interbank Financial Telecommunication) Emerging Markets Infrastructure fund had almost half of their portfolio invested in Latin America in 2010.

Swips infrastructure fund was liquidated last year, following the internal restructuring of its emerging markets team. But Joanna Terrett, an investment director on the international equities team, says the investment case for infrastructure in emerging markets remains attractive.

Some of the investments previously held in the Latin American part of the infrastructure fund can still be found in other Swip funds.

“There is a lot of bureaucracy and red tape in emerging markets but the Brics [Brazil, Russia, India and China] are still attracting infrastructure investors,” Terrett says. “There are a lot of opportunities.”

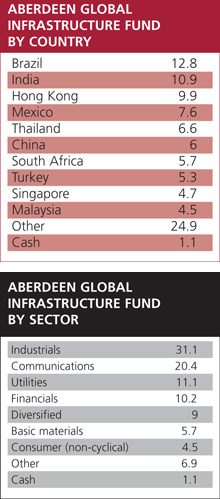

The JP Morgan Emerging Markets Infrastructure Equity fund, and the Aberdeen Global Infrastructure fund have nearly a third of their portfolios invested in Latin America.

Leon Eidelman, a co-manager of the JP Morgan fund, says within emerging markets there are more opportunities in Brazil and India, than in China and Russia. He says in a high inflation environment, such as in Brazil, companies tend to be more efficient as they have to generate returns greater than inflation.

In Brazil, inflation has soared to 7.3%, measured on a twelve-month basis, well above the Central Bank of Brazil’s target of 6.5%.

Despite mounting inflation worries, the bank has recently cut its benchmark interest rate by 50 basis points to 12%. Mexico has signalled it may follow suit. Fears over a global slowdown and a weaker growth outlook for Latin America’s largest economy had prompted the move.

The rate cut actually bolstered long-term investor sentiment towards Brazilian equities, even though the Bovespa (São Paulo stock exhange) fell in recent months.

Fund managers say they do consider macroeconomic factors, such as economic growth, inflation, and interest rates when making investment decisions. But stock characteristics tend to be the decisive factors.

Stephen Parr, an investment manager at the Aberdeen Global Infrastructure fund, says a shareholder-friendly attitude of companies is crucial. Parr, who can invest in infrastructure projects around the world, has nearly a quarter of his fund invested in Latin America.

High levels of corporate governance, talented management teams and innovative business models are some of the factors that draw Parr into Brazil and Mexico, rather than rapidly growing China.

Over the past ten years, China’s economy grew by a staggering 11.3%, compared with 3.7% in Brazil, according to the International Monetary Fund. Stock market returns, however, have been less impressive.

Over the past ten years, China’s economy grew by a staggering 11.3%, compared with 3.7% in Brazil, according to the International Monetary Fund. Stock market returns, however, have been less impressive.

Data from Morningstar suggests there is no positive correlation between economic growth and stock market returns. The MSCI Brazil Index returned 849.6% over the past ten years, but the MSCI China Index only 394.4%.

“Most importantly, we need companies that are run for shareholders, not for the management or the government,” Parr says. “We have limited or no exposure to Russian companies because the level of corporate governance is not high enough, but there is a lot of it in Brazil. Mexico also has high-quality companies.”

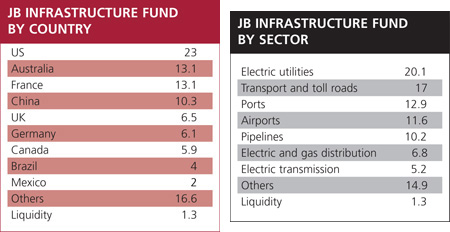

A decade ago, the Brazilian market created a new listing segment called Novo Mercado, which is reserved for companies with higher standards of corporate governance. According to a recent study of the Global Corporate Governance Forum and the International Finance Corporation, the companies listed on the Novo Mercado have generally outperformed their non-Novo Mercado peers. Other infrastructure fund managers see more compelling investment opportunities elsewhere. Justin Lannen, manager of the JB Infrastructure fund, says some of his largest holdings are Vinci, the French construction group, and the Spark Infrastructure Group in Australia.

Lannen says only 6% of the portfolio is invested in Latin America, while 10% is invested in China.

“We see strong growth in transportation infrastructure in China, with passenger numbers at airports and volumes on toll roads benefiting from solid GDP growth,” he says.

He adds, however, that there are numerous opportunities for infrastructure development in Latin America, which should be a strong driver of growth.

In Latin America, he holds Energias do Brasil, an energy infrastructure company operating in electricity generation and distribution. The company is increasing its exposure to the growing Brazilian electricity generation sector with low pricing risk.

LLX Logistica, another of his Latin American stocks, is an underdeveloped seaport in Rio de Janeiro. The port has seen significant support from local government and demand from customers as it plans to combine several stages of the value chain to build the largest port project in the region.

Elsewhere in Latin America, the fund owns two Mexican airports.

Elsewhere in Latin America, the fund owns two Mexican airports.

Latin America equity managers who can invest across sectors also find investment opportunities in infrastructure. Mark Livingston, a product manager in the emerging markets investment department at Fidelity Worldwide Investment, says his team has a positive view on infrastructure in Latin America, particularly as Brazil is preparing for the Fifa World Cup and the Olympic Games.

Yet many companies in Brazil have been struggling against foreign competition because of the strong currency, which makes their exports more expensive and less competitive.

Over the past three years, the value of the Brazilian real has risen by nearly 50% against the dollar, even though the government has taken measures to control the inflow of capital that is putting upward pressure on the currency. Brazil has introduced taxes on some foreign purchases of domestic assets while banks have been forced to hold higher reserves and pay higher taxes on short-term lending.

“Brazil and, in several cases, the rest of Latin America, continues to face large bottlenecks in transporting goods in and out of their region,” says Livingston. “However, the investable opportunities in this regard are not as clear cut.”

Because of the limited investment universe, many managers have loosened their sector definitions. The Fidelity team, for example, counts Cemento Argos, a cement business based in Colombia, as one of its infrastructure investments.

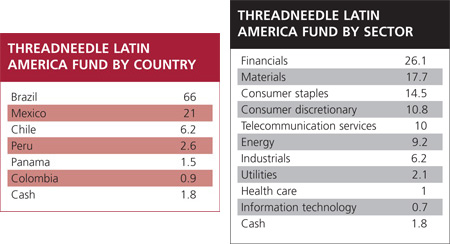

Daniel Isidori, the manager of Threadneedle Latin America fund, obtains only some of his infrastructure exposure directly. He holds commercial homebuilders, including MRV Engenharia and PDG Realty, and commercial properties, such as BR Properties. Other exposure is indirect, such as through a car rental company, Localiza, whose client base is mainly business oriented.

Although his portfolio is a result of individual stock decisions, he sees domestic consumption as a more interesting theme than infrastructure. Some of Isidori’s high conviction holdings are companies operating in retail, beverages, media and personal care.

Although his portfolio is a result of individual stock decisions, he sees domestic consumption as a more interesting theme than infrastructure. Some of Isidori’s high conviction holdings are companies operating in retail, beverages, media and personal care.

Struggle

Despite the recent surge in investment opportunities and managers’ abilities to broaden the mandate of their funds, they continue to struggle in some sectors. Telecommunications is a prime example. While the sector has shown strong growth, making it attractive to investors, it has been difficult for them to buy into because regulation is tight.

“We recongise the growth opportunities and the relevance of the telecommunications sector, but we are modestly underweight,” says Parr. “Regulation does have an impact on our investment decisions.”

América Móvil, Latin America’s biggest telecommunications company, has repeatedly come under pressure from regulators.

Share prices slumped to record lows earlier this year after the watchdog Comisión Federal de Telecomunicaciones decreed changes to the company’s fee structure, one of a growing number of steps to reduce its dominance.

Overall, stock exchanges and the regulatory framework surrounding infrastructure investments have been developing in line with economic growth. With Latin America’s market capitalisation as a percentage of its gross domestic product still low, there is significant potential for further expansion.

©2011 funds global