Emerging market ETFs have seen a short period of renewed inflows. Nick Fitzpatrick looks at measures needed to make their performance more transparent.

The ability to track an index closely is a major factor in exchange-traded fund (ETF) selection. Returns from ETFs can vary significantly even when based on the same index.

Emerging markets are more tricky for ETF providers to track owing to inefficiencies in the underlying markets, and the MSCI Emerging Markets equity index is the most common index used. The index has 21 countries and 822 names.

Emerging markets have underperformed since the summer of 2013. Before Easter, though, emerging market funds – including ETFs – saw an emerging market “bump” as flows to these regions increased.

Andrew Walsh, head of UK ETF sales at UBS, says the UBS emerging market ETF saw $284 million (€205 million) of inflows this year, taking total assets under management in it to £820 million (€996 million).

EPFR Global, which tracks fund flows, tracked positive inflows into various kinds of emerging market funds in early April and said investors were favouring the “diversified exposure and relative ease of exit” offered by global emerging markets ETFs.

At April 22, the MSCI Emerging Markets index had fallen back slightly from 1,132.67 on January 1 in sterling terms, to 1,121.83, but had still made a notable recovery from close to 1050 in February.

Flows have since slowed and the bump appears to be over – though opinions in the asset management industry that emerging markets valuations are now worth a fresh look are not hard to find.

Research from State Street, New Horizons for Official Institutions, points to pent-up demand for these markets across different asset classes.

It found that 80% of “official institutions” it surveyed, such as sovereign wealth funds, expect to increase their exposure to emerging markets.

TRACKING ERROR

Those who might extend an emerging market exposure, or begin one, using an ETF – at least as a stopgap until an active manager is found – will be encouraged to focus on tracking error significantly. It is a key part of ETF selection. Selecting the right ETF is not easy and more regulatory weight is being loaded on to the industry – including index manufacturers – with the aim of making ETFs more transparent.

Some industry players have responded and tracking error and costs are at the centre of the focus.

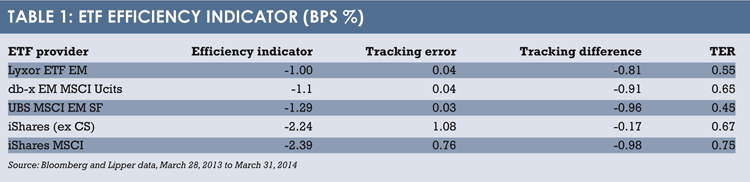

One example is Lyxor, Europe’s third largest ETF provider, which has ranked some of the top ETFs by assets according to its “efficiency indicator” (EI).

Fortunately for it, Lyxor ranks first in the emerging market category with a score of -1.00% (see table 1). It is followed by db-x trackers, which is the ETF arm of Deutsche Bank, UBS, and then two iShares ETFs.

Despite having the lowest EI, the iShares ETFs are also the most expensive, with the highest total expense ratios.

They also have the worst tracking error, defined as the volatility of the performance spread measures on a daily basis over one year.

However, the ex-CIS ETF has the best tracking difference.

Importantly, though, a key difference between the ETFs is that the iShares ETFs are physically replicated and the others are synthetic. Lyxor’s EI combines the three performance characteristics that Lyxor says matter most to investors: tracking difference, tracking error and liquidity spread.

The EI was proposed in 2013 by Thierry Roncalli, head of research & development at Lyxor and professor of finance at the Evry University, and Marlene Hassine, ETF research at Lyxor, in an academic publication entitled Measuring Performance of Exchange Traded Funds.

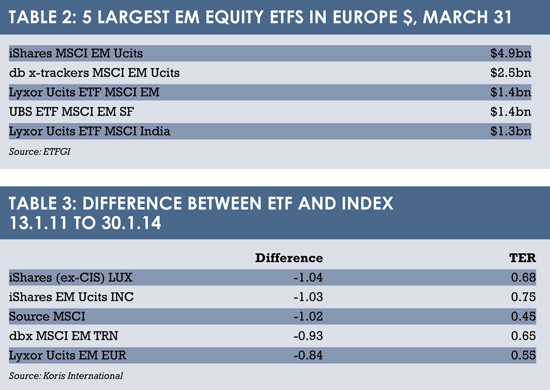

Despite the gap between the cost and tracking error, investors have made iShares emerging market ETFs the largest in Europe. At the end of March, ETFGI figures show the Europe-listed iShares MSCI Emerging Markets Ucits ETF had $4.9 billion of assets (see table 2).

Despite the gap between the cost and tracking error, investors have made iShares emerging market ETFs the largest in Europe. At the end of March, ETFGI figures show the Europe-listed iShares MSCI Emerging Markets Ucits ETF had $4.9 billion of assets (see table 2).

DELTA 1 EXPOSURE

Further scrutiny of ETFs as transparency marches onwards comes now from Koris International, an investment advisory firm.

Koris says it does not want to rank providers or postulate what is a good ETF for the level of fees paid for it, and points out that what investors intend to do with their ETF – such as short-term trading, or using an ETF for hedging – can influence the choice of ETF.

Funds Europe has listed ETFs from Koris’s research by the size of the difference between the ETF return and the index (see table 3). The focus of Koris’s first report is on tracking, but the firm’s next report will focus on market structure and liquidity.

“Tracking an index at controlled costs can be a clear challenge and this is what we want to put attention on,” says Jean-René Giraud, chief executive officer of Koris International in the ETF Inside Out report.

Delivering a delta-one exposure to an index – “a clever way to explaining the fund performance is matching that of the index” – is far from an easy task, says Giraud. Transaction costs, dividend treatment, tax assumptions, replication strategies, discrepancies between exchange trading times and other complexities inherent to the management of an ETF have resulted in those funds requiring fairly complex financial, regulatory and operational setups, Giraud says.

He adds there is no black-or-white conclusion that can be made as “all ETFs demonstrate excellence in some areas, weaknesses in others”.

This only emphasises the need for investors to put more attention to the selection of ETFs, Giraud says.

©2014 funds europe