François Millet, head of ETF and index product development at Lyxor Asset Management, looks at one of the major investment themes of the year and discusses why ETF assets under management have doubled in the past five years.

Recent flows into inflation-linked bonds point not just to a new inflation regime, but also to the inexorable rise of ETFs. Where do we go from here?

Central banks have been spending freely in support of their economies for years, largely without any of the expected effects on inflation rates. Now though, they are turning to fiscal policies – like increasing infrastructure spending or cutting taxation – to support loose monetary policy and that, allied to higher energy prices and near-full employment could drive inflation higher. When and where it might rise is hard to predict, but it’s better to be prepared.

GONE, BUT NOT FORGOTTEN

Having been dormant for years, inflation protection has emerged as a big theme for investors this year. Nobody wants to be caught off guard. Assets under management (AuM) in inflation-linked bonds have grown faster than almost any other bond market sector (see Fig 1). Fixed income flows are up 21% vs the same period last year, but the inflation-linked segment is ahead by 168%. And, with €8.7bn of assets under management, this segment now represents more than 6% of the total AuM for fixed income ETFs¹.

TAKING OFF TOGETHER

TAKING OFF TOGETHER

Although the US and European inflation-linked markets enjoyed inflows last year, the US was far more popular given more consistency in its economy.

Flows into Europe were more evident in the first and fourth quarters when prospects for an economic recovery appeared more concrete.

The pattern has been similar so far this year. The US has gathered most of the inflows due to improving economic conditions and a more stable oil price.

SUSTAINED DEMAND

Last year marked the apparent end of the very low inflation regime brought about by years of quantitative easing, especially in the US. That’s continued into 2016 as oil prices have rebounded and stabilised above $45 per barrel.

The outlook for oil looks positive over the next 12 months, so we believe inflation expectations in the US are actually lower than they should be. We still expect inflation to gradually move higher in the next few quarters, particularly in the eurozone where the effects of higher energy prices should finally be felt. This should help prompt further significant inflows.

UNDER THE PUMP

Although the ride won’t be smooth, we do expect much greater oil price stability as OPEC resumes its role as the regulator of supply. We also expect the bottoming out of headline inflation in the developed world. Taken together, this should support inflation expectations in the future.

Key numbers²:

- We see headline inflation in the eurozone reaching 1% by the end of the year, and 1.5% early next year

- In the US, a weaker dollar, higher energy prices and a tighter labour market should help lift headline inflation. The absence of any real wage growth could be an issue.

- We expect most developed world countries to get close to their 2% target for inflation, except in the UK, where sterling weakness could drive imported goods prices higher and push headline CPI figures above 2.5% by 2018.

STERLING PERFORMANCE

UK RPI has been rising throughout 2016, driven in part by sterling’s post-Brexit weakness. Sterling is already one of the world’s worst-performing currencies this year3 but it’s hard to see any immediate catalysts for a rebound. With many everyday goods produced overseas, a weak exchange rate could feed into price rises on the high street. Add to the mix the bounce in energy markets and recovering global economic growth and it’s not hard to see why RPI could go much higher.

Inflation-linked gilts are probably the most direct way to hedge against UK price rises. But this isn’t their only benefit – they can also be a driver of profit in a portfolio. The broad benchmark in this market is the FTSE Actuaries UK Gilts Inflation-Linked index, which covers more than 20 issues. The index returned 30% in the first nine months of this year4.

ADDITIONAL DIVERSIFICATION

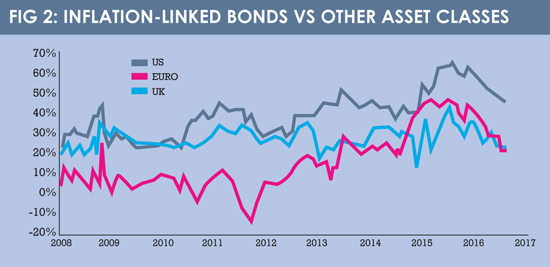

Although cross-asset correlations aren’t quite as high as they were, they are still above average (see Fig 2). Effective diversifiers are as important, and scarce, as ever. Inflation-linked bonds are now less correlated with other bonds, so they could help cushion portfolios at a time when most bond markets are looking expensive.

WHY ETFS WORK FOR INFLATION LINKERS

The acceleration of money flowing into inflation-linked products isn’t just limited to ETFs. €5.5bn flowed into the sector last year, while there’s already been €6bn of inflows this year.5 Where that money is going has, however, changed.

Active and passive products both enjoyed materially more inflows in 2015, but this year, ETF flows have grown by 32% (and done so in each quarter since January) while flows into active funds have declined by 1%5.

Reasons for this are several, but there does seem to be much greater awareness of the fact active managers aren’t always delivering what their investors need. On average, only 11% of active funds outperformed the FTSE MTS Eurozone Inflation-Linked bond index in 2015. Not one has outperformed the index over 10 years.5

Cost also comes into it – ETF fees are generally lower than those of actively managed funds, so investors get to keep more of their yield. This is important in markets in which real yields are low and every basis point counts.

It’s easy to see why ETF AuM has doubled over the last five years. And there’s no reason to think it won’t continue to grow with major markets like the US and Europe still dominated by active funds.

Footnotes:

1 – Source: Data in EURM, Lyxor, Bloomberg from 01/1/2014 to 31/8/2016

2 – Source: Societe Generale, Cross Asset Research. Data taken from the paper titled “The virtues of inflation-linked bonds”, released 14 October 2016

3 – Source: FT October, 2016.Past performance is no guide to future returns

4 – Source: Bloomberg, 1 October 2016.Past performance is no guide to future returns

5 – Source: Lyxor, using Morningstar data from 31/12/05 to 31/08/2016. The figures relating to past performances refer to past periods and are not a reliable indicator for future results. This also applies to historical market data.

THIS COMMUNICATION IS FOR ELIGIBLE COUNTERPARTIES OR PROFESSIONAL CLIENTS ONLY.

This document is for the exclusive use of investors acting on their own account and categorized either as “Eligible Counterparties” or “Professional Clients” within the meaning of Markets in Financial Instruments Directive 2004/39/EC. These products comply with the UCITS Directive (2009/65/EC). Lyxor International Asset Management (LIAM) recommends that investors read carefully the “investment risks” section of the product’s documentation (prospectus and KIID). The prospectus and KIID are available free of charge on www.lyxoretf.com, and upon request to [email protected]. Lyxor

International Asset Management (LIAM), société par actions simplifiée having its registered office at Tours Société Générale, 17 cours Valmy, 92800 Puteaux (France), 418 862 215 RCS Nanterre, is authorized and regulated by the Autorité des

Marchés Financiers (AMF) under the UCITS Directive and the AIFM Directive (2011/31/ EU). LIAM is represented in the UK by Lyxor Asset Management UK LLP, which is authorized and regulated by the Financial Conduct Authority in the UK under

Registration Number 435658.