Enhanced portfolio techniques are not sufficiently used in the investment management industry. Felix Goltz, of the Edhec-Risk Institute, explores the reasons behind this

In a ‘call for reactions’ carried out last year, the Edhec-Risk Institute canvassed the views of investment professionals on the conclusions of the Edhec European Investment Practices Survey, sponsored by Newedge. Fifty-seven investment management professionals sent us the completed questionnaire.

Our first objective was to establish whether there is any agreement with our conclusion that enhanced portfolio construction techniques are not sufficiently used in the industry today. Almost 95% of respondents agreed with this statement. One respondent plainly summarised the overall perception of respondents when he said that “many of the improvements found in the literature are not used by the industry”. The need to make progress is also acknowledged because the added value of portfolio construction tools is being recognised. “Decent and intelligent portfolio construction is an active source of performance and gives relief on forecast power, which is weak anyway,” says one respondent.

However, a small fraction of 5% of respondents disagrees with the conclusion of the Edhec European Investment Practices Survey concerning portfolio construction. One of the respondents in this group states that he “does not believe in modern portfolio theory based on optimisation using statistics”. This statement suggests that respondents disagreeing with our conclusions may do so because they see no value in portfolio construction techniques, not because they believe current practice in the industry fully integrates state-of-the-art concepts. Interestingly, there seems to be a common view among respondents that investment managers often use ad hoc decision making rather than quantitative portfolio construction processes. As one respondent puts it: “Very often portfolios are built in a qualitative way because people do not trust the optimiser or do not know quant tools.” Another respondent states that: “Many firms, even those that claim to have consistent asset allocation techniques, implement them arbitrarily or chaotically.”

Of course, there are many potential reasons for these practices. The objective of our call for reactions is, as it happens, to shed light on these reasons. With this awareness, the means of improving the situation, if any exist, may become clearer. We were interested in identifying the priority assigned by practitioners to techniques for improving portfolio construction.

Table 1 shows the results of our call for reactions. From these, we identified four groups of techniques that could be improved:

- Computation of VaR

- Covariance estimation

- Bayesian and resampling techniques

- Use of relative risk measures

Respondents to our call for reaction believe that improvements in all four groups are important. When asked to identify the need for improvements to these techniques on a scale of 1 (not important) to 4 (extremely important), respondents clearly state that improvements are important across the board.

For example, no more than 20% of respondents think that improvements to any one of the four groups are not important. Likewise, the average score is at least 2.5 for the four groups, showing that respondents tend to attach rather high importance to improvements in any one group. VaR computation and covariance estimation, however, are considered in greater need of improvement than are Bayesian and resampling techniques or relative risk measures, as shown by their average scores (2.87 and 2.79 versus 2.50 and 2.51), as well as by the percentage of respondents who believe that improvements are extremely important (36% and 30% versus 22% and 23%). Overall, exhibit 1 shows that practitioners actually do see progress on the conceptual front as important; that the four groups highlighted by the Edhec-Risk survey are of relevance to them is also confirmed.

Although improvements to all four groups are considered important, it may be interesting to find out why practitioners do not use of state-of-the-art techniques in the first place. After all, the results of research in financial economics that apply to investment management are available free of charge to anyone, including practitioners in the industry.

In principle, then, there could be a number of reasons for the failure to take advantage of these results, despite their ready availability. It may be that research advances simply do not add significant value in a practical context. Another possibility is that clients express no interest in state-of-the-art techniques and investment managers make no effort to make them an integral part of their day-to-day activity. Or it may be that investment managers themselves lack knowledge of existing techniques, so they are not used, even though they may add value and clients may raise no objections. Finally, the use of portfolio construction concepts may simply be too difficult or costly, even if the concepts themselves do not pose a problem.

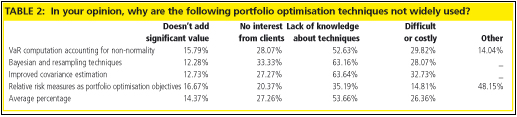

We asked the respondents to state why they believe new portfolio construction concepts are not widely used. The results are shown in table 2. The percentages do not add up to 100% across every line of the table, as multiple answers were possible. The average percentage of respondents for every explanation across the four groups is indicated in the bottom line of the table.

Across the four groups, 14% of respondents raise the issue of limited value-added. As one respondent writes: “When focusing on these techniques, you lose focus and miss good investment opportunities.”

However, while there are differences across the various areas of portfolio construction techniques, overall, only a minority of respondents claim that the advanced techniques in our four groups do not add significant value. On the other hand, 27% of respondents find that clients may be to blame for the limited use of advanced portfolio construction techniques. One respondent arguing in favour of this explanation states that: “If the client isn’t comfortable with a technique, his fund manager isn’t going to get informed consent for a mandate including such a technique.” However, some respondents argue that the duty of drawing on existing financial knowledge lies with the asset manager, not with his client: “It is neither necessary nor useful to try to explain sophisticated techniques systematically to clients.” For this respondent, it is also up to the investment manager “to be able to explain complex techniques in a simple way to clients”.

Of the respondents, 26% believe that the difficulty or cost of implementation is responsible for the relative neglect of sophisticated techniques. Indeed, it may be that academic studies present portfolio construction techniques in highly stylised environments, making it difficult to draw on the insights directly. “Going from academic concept to implementation requires many iterations of playing with real data,” says one respondent, “there is little research on which technique adds value under which circumstances.” It should be stressed that none of these reasons – lack of value, lack of client interest, and implementation difficulties – are subscribed to by much more than a quarter of respondents. The majority of respondents (54%) hold the lack of knowledge among investment managers in the industry responsible for the failure to use these portfolio optimisation techniques.

As one respondent says: “The advantages and potential pitfalls of portfolio optimisation techniques are understood properly by only a handful of industry participants.” Another practitioner has harsher words for his colleagues: “There are too many people in our industry who have no interest in constant learning and improving their methodologies. Therefore, the funds suffer from several layers of vintage knowledge.”

There may be other explanations for the industry’s failure to use some of the mentioned improvements. Relative risk considerations may, in fact, be used as a constraint rather than as the objective function in portfolio optimisation. For 48% of respondents, it is for this reason that relative risk objectives are not more frequently taken into account in portfolio optimisation. In addition, only 35% of respondents attribute the low use of relative risk objectives to a lack of knowledge among industry professionals; for the three other groups of techniques, this number comes to more than 50%.

In VaR computation, 14% of respondents indicate that considerations of non-normality may not enter the decision process more often because, in the presence of scarce data, low frequency or short history, it may be difficult to estimate parameters for models incorporating non-normality. It is interesting that Bayesian and resampling techniques and improved covariance estimation are considered of little value-added by the lowest percentage of respondents and victims of practitioner ignorance, as it were, by the highest percentage of respondents. This combination of relatively positive views of the techniques themselves and relatively pessimistic views of practitioner knowledge of said techniques suggests that practitioners refrain from implementing techniques when they lack in-house competence, even though they are convinced of the value of these techniques.

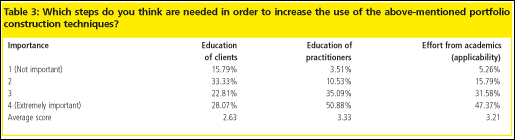

Obviously, the means of fostering the adoption of advanced portfolio construction techniques depend on the cause of the current failure to use these techniques at acceptable rates. We asked the practitioners who respond to our call for reaction for their views on how to improve matters. If, as one respondent suggested, “vintage knowledge” is to blame for the reluctance to adopt advanced techniques, education, either of investment managers or of clients, may be an appropriate response. At the same time, it may be that research must better respond to practitioners’ needs by addressing issues of practical relevance and by giving clear directions on practical applications. For a view on practitioners’ thoughts on potential remedies, we asked them to state the importance they attribute to better education of clients, of investment managers and to greater efforts by academics to render their research applicable. The results are shown in table3. Again, respondents were asked to rate importance on a scale from 1 (not important) to 4 (extremely important). The bottom line of the table shows the average score for each potential remedy for the failure to adopt advanced portfolio construction techniques.

Table 3 shows that the education of investment management professionals is regarded as the most important step to take to increase industry uptake of advanced portfolio construction techniques. Indeed, half the respondents think that the education of practitioners is “extremely important”. The education of clients is considered of less overall importance, although 28% of respondents still believe it is “extremely important”.

Respondents clearly think that academic research also has a part to play in improving things. Of the respondents, 47% say an effort on the part of academics to render their results more applicable is “extremely important”. One respondent says: “Academic research often seems to ignore the real practical constraints of the business. The difference between a single study and a robust system with good data capture over time and robust implementation is enormous.” At the same time, the value-added of concrete research advances is clearly acknowledged. For example, table 2 shows that none of the advanced techniques mentioned is perceived to suffer from a lack of value-added.

Indeed, one respondent states that even though “research material is not always practical for the industry, professionals should try anyway to exploit these new techniques to gain a competitive advantage”. Other respondents, on the contrary, do expect more effort from academics, with one saying: “It would be very helpful for the industry to get some practical guidelines from the academics on how to apply the results in the real world.”

• Felix Goltz is head of applied research at the Edhec-Risk Institute

©2010 funds europe