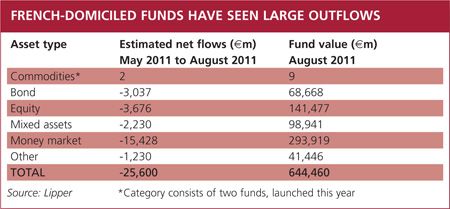

French funds are outflowing across many asset classes and the country’s closed market means distribution is locked down by the big players. No wonder top CEOs are looking abroad. George Mitton reports.

When Funds Europe visited Paris last year there was optimism about big deals and the dynamism of the boutique firms but this year, the talk is downbeat. Because of Basel III requirements (a new global regulatory standard on bank capital adequacy and liquidity agreed by the members of the Basel Committee on Banking Supervision), the banks want to get more money on their balance sheets, and billions have flowed from French funds into bank deposits. “France has seen high outflows in any given asset class,” says Pierre Servant, chief executive officer of Natixis Global Asset Management.

Then there are worries about exposure to Greek debt, which prompted the ratings agency Moody’s to downgrade two French banks, Société Générale and Credit Agricole. The stock market has tumbled in recent months, causing losses across hundreds of funds.

There is still room for growth, just not in France. Senior executives in some of the top French firms say the battle is for overseas markets, while competitive pressure at home will squeeze profits across the board.

It is not that the dynamic boutiques have gone. The number of asset managers in France continues to grow, thanks to supportive government policies and seed capital for such firms. But the darling of the French boutiques, Carmignac Gestion, has had a difficult year (see box) and there are fresh claims that these firms will only survive if they stay small. As Christian Dargnat, chief executive officer at BNP Paribas Asset Management, part of BNP Paribas Investment Partners, puts it, “in this business you need to be very big or very thin”.

The thinking is that the French market only has space for two types of asset manager. There are the behemoths such as Amundi, Natixis Global Asset Management, BNP Paribas Investment Partners and Axa Investment Managers, which have their own distribution networks reaching millions of retail customers. And the small, nimble boutiques that serve a handful of affluent investors and some institutions.

Many in France characterise it as distinction between factories and artisans. On the one hand, big firms – backed by banks or insurance companies – that roll out cheap, beta-generating products such as money market funds and fixed income products. On the other, specialists that supply mainly equity funds designed to capture elusive alpha returns.

According to Dominique Carrel-Billiard, chief executive officer at Axa Investment Managers, this landscape is not likely to change soon, because the big players want to protect their distribution networks. “Accessibility is the key issue,” he says. “France is still a country where the architectures are closed. They open up for the very high-net-worth individuals and in some circumstances for corporate plans. But it is still mostly a closed country.”

Independent financial advisers (IFAs) account for just 15% of the market, which is higher than ten years ago but still much less than in the UK, where 90% of the market goes through IFAs. The rest of the retail market buys funds through a bank or an insurance wrapper. Industry groups are quick to paint this as a cultural quality of the French, rather than protectionism.

Going global

The institutional market is freer than retail but much less significant than in other European countries because France has fewer pension funds and the main institution-like money comes from insurance companies.

Carrel-Billiard ponders the matter from his office in La Defense, the business district of Paris, which has a view out to the Eiffel Tower. “Internationally is where the stakes are. Most of my colleagues see that France has reached saturation, so their growth potential is abroad.”

The question of where to invest foreign resources is an important one. Axa is one of only two French firms with a meaningful presence in the United States, thanks to its subsidiary AllianceBernstein. The other is Natixis (see box). The rest of the French firms have had difficulty breaking into a market that accounts for half the world’s assets under management.

Some are looking to Asia and the Middle East, but not all. Yves Perrier, Amundi chief executive officer, says: “The first objective is to make Europe our domestic market.”

Amundi, which is the biggest French manager by assets under management, has hopes to expand in Germany and elsewhere, pushing its low-cost products at a time when low interest rates are hurting asset management firms.

Perrier says that in the financial year 2010, Amundi was the only firm of the big four to have positive net inflows, as demand for equity, bonds and absolute return products compensated for money flowing out of money market funds. “You have to choose the field where you have the best chance to win,” he says. “As you know, I have played sport a lot. You are more successful when you play at home than when you play away. The US is a very tough market for foreigners, especially for Europeans.”

He says the merger between Société Générale and Credit Agricole that created Amundi in January 2010 is now complete, and the last of the employees laid off in the merger left the company at the end of March this year.

In its expansion efforts, Amundi may be assisted by the Ucits IV regulations which should make distribution of cross-European funds simpler. The French government transposed Ucits IV into law this summer, just in time for the deadline. France is an important market for the legislation as it hosts the second biggest number of EU-domiciled funds, after Luxembourg but before Ireland.

The regulation requires some adjustments, notably the creation of Key Investor Information Documents. One industry observer admits this will be “a nightmare for their lawyers and IT guys”. However, Ucits IV may offer economies of scale thanks to the master-feeder structures. Combined with the management company passport, it will allow firms to launch funds outside the country without having to set up or keep local subsidiaries. Some players intend to repeal existing foreign subsidiaries but keep funds there as feeders, cutting costs.

There may be some adverse consequences, though. The regulations will make European distribution easier for all companies, including non-European ones, potentially ratcheting up competition. And some say there will be a tax incentive to domicile master funds in Luxembourg instead of France.

Though he has no plans to do so, Patrick Rivière, chief executive officer at La Française AM, formerly UFG-LFP, accepts this could occur. “The tax effect won’t be from a client perspective because there is no difference for a client if it’s Luxembourg or Dublin or France,” he says. “But if you have to choose where your money has to be taxed, as a fund manager you may prefer it to be taxed in Luxembourg.”

The French funds industry group L’Association Française de la Gestion Financière denies this, however, and says survey data says firms still want to be based in France. “There was no significant intent to locate masters in Luxembourg,” says Stéphane Janin, head of its international affairs division.

“There was a clear expression of will to domicile largely their master funds in France, which makes sense. It is preferable to have the master fund where the manager is, where the track record is.”

©2011 funds europe